Wasion Group is a pioneering supplier of smart meters and power distribution as well as an integrated energy management solution provider in China. It owns outstanding core competitiveness. Since 2012, the company has consistently increased its investment in research & development (R&D), boosting the R&D expense ratio from 2% to 4% to strengthen its technological edge. Besides, the company also has built up brand recognition among its downstream customers. Leveraging on its all-rounded competitiveness in technology, quality, scale and management, the company maintains its competitive advantage in the smart meter tenders of the State Grid and China Southern Power Grid, enabling it to be the top three players of the industry.

At present, smart meter business accounts for around 1/3 of the company's revenue. There will be close to 120 million households installing smart meters in the coming several years. Besides, the replacement cycle of smart meters will be around 5-8 years according to the state regulation. As a result, the domestic demand for smart meters is expected to remain steady at a double-digit annual growth rate. Wasion Group is one the few successful bidders in almost all tenders of the State Grid and China Southern Power Grid, so we believe its smart meter business will at least achieve Synchronous growth.

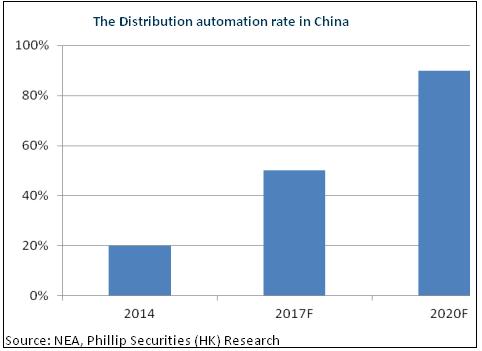

During the 13th 5-Year Plan, the domestic smart grid will enter into the investment phase of the 2nd-generation AMI, which may create more business opportunities for the company. Meanwhile, the water, gas and heat business will also be the key to the company's growth momentum. What's more, there may also be better growth opportunities for its ADO business. Currently, the automation rate of the nation's power distribution is just at around 20%, which is far below the 50% level achieved by developed countries. The target of the Energy Bureau is to raise the level to 90% by 2020. Wasion Group is now speeding up its development in this business. We believe that the ADO business has entered into a fast-growing stage and will maintain a high growth rate of 50% or above in the medium term.

Main beneficiary of smart power grid

China's power reform will drive the development of smart grid, which will also significantly stimulate the demand for automated power distribution equipment. Wasion Group will be one of the major beneficiary. The reform of water pricing will also lead to further growth of the company. At the same time, profitability can be sustained at a high level with the improvement in product mix. The gross margin is expected to stay at 31% or above.

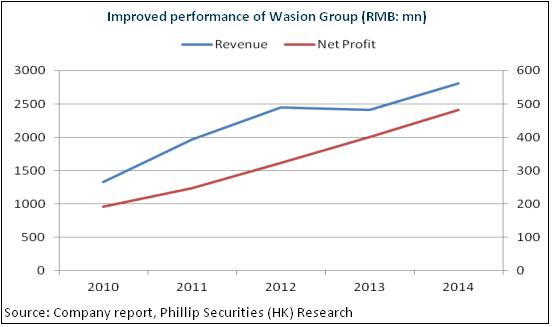

CAGR of the company's revenue and net profit was 20.6% and 26% respectively from 2010 to 2014. It is expected to deliver a rapid growth at 20% or above during the 13th Five-Year Plan. We forecast that the revenue of the company will reach RMB3.4 billion and RMB4.12 billion in 2015-16, representing an annual growth of 21% and 21.1%. Net profit is expected to reach RMB610 million and RMB740 million, representing an annual growth of 27.3% and 21.1%. Corresponding EPS will be RMB0.62 and RMB0.72.

Outstanding core competitiveness

Wasion Group is a pioneering supplier of smart meters and power distribution as well as an integrated energy management solution provider in China. The company was established in 2000, initially just as an electricity meter manufacturer. It has actively developed into the upstream of the supply chain, by offering solutions to advanced metering infrastructure (AMI) and advanced distribution operations (ADO). These two segments have already contributed to 70% of revenue and enjoyed higher profit margins. In terms of business arena, the company has expanded into water, gas and heat meters.

The company has built up technological competitive advantage. Since 2012, the company has consistently increased its investment in research & development (R&D), boosting the R&D expense ratio from 2% to 4% to strengthen its technological edge. In 2015H1, the company received 44 patents for its new products and energy saving services and 21 patents for its software. The number of effective patents for new products and energy saving services are 605 and 392 respectively. At the same time, it has successfully gained market recognition by developing and launching a number of AMI systems and solutions. Among which, the “Power, Water, Gas and Heat All-in-one Data Collection System” has received pilot orders in Beijing, Shanghai and Shangdong.

Besides, the company also has built up brand recognition among its downstream customers. Leveraging on its all-rounded competitiveness in technology, quality, scale and management, the company maintains its competitive advantage in the smart meter tenders of the State Grid and China Southern Power Grid, enabling it to be the top three players of the industry.

Continued steady growth in its smart meter business

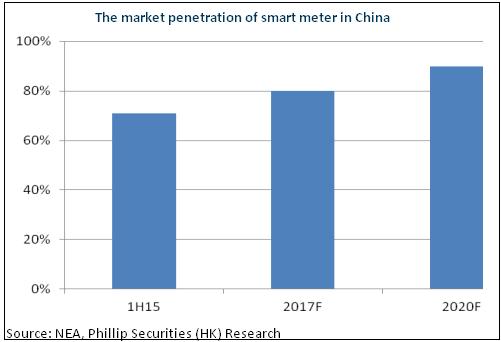

At present, smart meter business accounts for around 1/3 of the company's revenue. Overall speaking, the demand for this segment continues to be strong. By the end of 2015H1, the national coverage of smart meters has already reached 71% and there will be close to 120 million households installing smart meters in the coming several years. Besides, the replacement cycle of smart meters will be around 5-8 years according to the state regulation. As a result, the domestic demand for smart meters is expected to remain steady at a double-digit annual growth rate. Moreover, Wasion Group is one the few successful bidders in almost all tenders of the State Grid and China Southern Power Grid. In the four tenders of State Grid in 2014, contracts won by the company reached RMB1.2 billion, representing an increase of 69% yoy. Recently, the company maintained its top position by winning a contract value of RMB330 million again in the third round of tender of the State Grid. The cumulative contracts won for the full year reached RMB1.08 billion, further strengthening the company's leading position in the industry.

Upstream businesses will keep high growth

AMI is an integrated service platform that consists of smart meter, data collection terminal, information system and smart metering system integration that contributes to 60% of the company's revenue. At present, the company grabbed over 20% of market share in China's AMI electricity market. Not only does it occupy a pioneering position, it is also the only supplier in the market that can offer advanced meters in power, water, gas and heat as well as integrated energy efficiency solutions.

It is anticipated that AMI system can save around 5% of electricity bills and hold the key to smart grid's next stage of development. During the 13th 5-Year Plan, the domestic smart grid will enter into the investment phase of the 2nd-generation AMI, which may create more business opportunities for the company. Moreover, the water, gas and heat business will also be the key to the company's growth momentum. Benefiting from the strong promotion of “step-up” water tariffs and ten water policies, the revenue of Wasion's water, gas and heat business increased by 47% yoy to RMB85 million in 2015H1. It was successfully short-listed in the tenders of 34 water companies. Its full-year target is to sign contracts for 60 projects and the company is likely to outperform its target, securing growth opportunities for its water AMI business.

Besides, there may also be better growth opportunities for its ADO business. Currently, the automation rate of the nation's power distribution is just at around 20%, which is far below the 50% level achieved by developed countries. The target of the Energy Bureau is to raise the level to 90% by 2020. Wasion Group is now speeding up its development in this business and will use more than half of the new fund raised through the share placement to develop the ADO business. This includes the setting up of an investment platform to acquire and consolidate resources and the construction of the Wasion Power Industrial Park to serve as the manufacturing and R&D base of its ADO business. On the other hand, the company will strengthen the strategic partnerships with international electricity players such as Siemens, ABB and Schneider Electric. In H1, this business segment grew by more than 70%. We believe that the ADO business has entered into a fast-growing stage and will maintain a high growth rate of 50% or above in the medium term.

Catalysts

The State Grid to announce its investment plan for 2016-2020;

More detailed announcements of the power reform.

Risks

Slower than expected development of the smart grid;

Risks in the overseas market;

Further decrease in gross margin.

Financials

Click Here for PDF format...