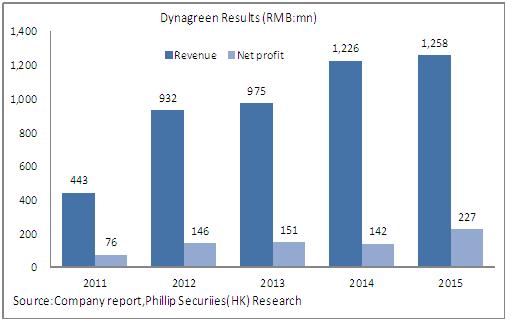

Mid-term Profitability: Annual Growth Rate at 50%

In 1H16, the company recorded a revenue of RMB832 million, representing a year-on-year increase of 28%; net profit was RMB166 million, increased by 50.02% Y-o-Y mainly due to the dropping tax rates. The EPS increased to HKD0.16 from HKD0.11 during the same period of the previous year, representing an increase of 45.5%.

In respect of profitability, the gross profit margin fell by 4.1% to 31.56% mainly affected by the fast revenue growth of waste generator construction business having comparatively low gross profit margin. In terms of expenses, due to the new operating projects, the administrative expenses reached RMB4.435 million, representing a year-on-year increase of 33.3% while the expense ratio fell by 0.2% from 5.3% compared to that of the business projects in the previous year. The financial expenses amounted to RMB5.251 million, representing a year-on-year decrease of 16% while the expense ratio fell by 3.1% to 6.31% compared to that of the previous year, mainly affected by the year-on-year decrease of borrowing rate due to the interest reduction policy issued by the Central Bank. Therefore, the net profit margin reached 19.9%, representing a year-on-year increase of 3%.

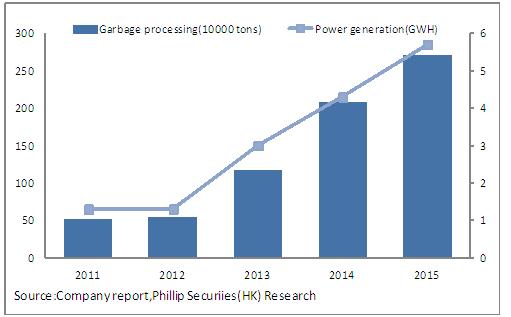

New Processing Capacity Was 1,400 Tons

During the first half of 2016, the waste treatment capacity reached 1.52 million tons, increased by 17% year-on-year with the processing capacity of approximately 8,500 tons/day. The power generation was 345 million kWh, representing a year-on-year increase of 32%. During the reporting period, a new operating project--the Jiangxi Yichun Project, was developed with the designed processing capacity of 1,400 tons/day and the investment amount of approximately RMB630 million. At present, the company has 27 projects at hand, including 10 operating projects. There are another 6 projects under construction including Huizhou, Ji County, Jurong, Ning River, Bangbu and Tongzhou Projects. The operating projects and those under construction aggregate a processing capacity of 13,560 tons/day. Because some of the projects under construction will be put into operation within the year, the annual treatment capacity of household waste is expected to increase approximately by 30%.

Steady Progress of Projects under Construction

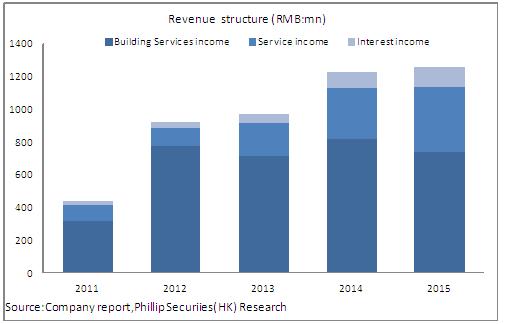

During the first half of 2016, the Company's waste-to-electricity business realized an operating revenue of RMB211 million, representing a year-on-year increase of 13.3%. The Huizhou Project and the Ji County Project were put into operation in May 2016. The Jurong Project is expected to be put into operation in the second half of the year. If everything goes well, the company is expected to achieve substantial growth in annual operating revenue of the waste-to-electricity business.

The waste generator construction business generated a revenue of RMB551 million, representing a year-on-year increase of 38.1% mainly due to delay of some projects, of which the revenue was recognized within the reporting period. The Ninghe, Bangbu and Tongzhou Projects are under construction. The total contracted processing capacity of the three projects is 3,750 tons/day and the investment amount reaches RMB2.034 billion, providing guarantee for the revenue growth of construction business in the coming two years.

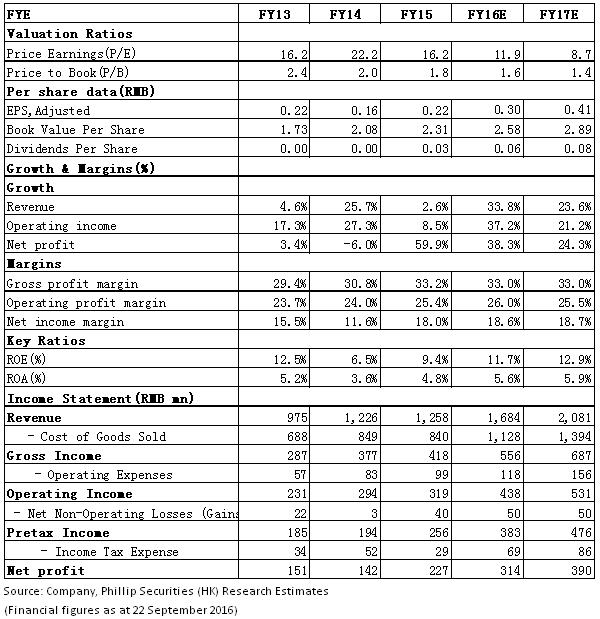

Valuation

The company focuses on expanding the processing capacity and raising the market share. So if the company is successfully listed on A-shares market, it is expected to significantly improve the cash flow status, strengthen the company's capital power and project acquisition power. In addition, with each project capacity increasing independently and the Shenzhen-Hong Kong Stock Connect program available, the company's valuation is expected to recover. We adopted the SOTP approach on the construction business and the operating business valuation, and give the target prices of HKD 5.52 and the Buy rating is granted. (Closing price as at 22 Sep 2016)

Risk Warnings

The acquisition of new projects falls short of expectations;

The progress of project construction is slower than expectations;

Capital and policy risks occur.

Financials

Click Here for PDF format...