Introduction to O-Net Technologies

O-Net is a wholly foreign-owned company in the technology sector, and has been named `Shenzhen Top Brand` and received `The Top 100 enterprises of China's Communication Industry in 2015`. O-Net principally engages in the design and manufacturing of optical networking components, industrial application and automation. In particular, optical networking business contributes to about 86% of the company's revenue in 2015 and has been the main driver of the company's growth in recent years, contributing to 63% and 75% of revenue growth in 2015 and 2014 respectively. The reason for the rapid growth is the firm's strategies of vertical integration as well as business diversification into sectors such as machine vision and fiber sensor.

Continued Rapid Growth in 1H2016

In the first half of 2016, O-Net generated HK$746.2Mn of revenue, a YoY growth of 43.3%, of which 59.5% are generated in China and Asia. O-Net also generated HK$44.3Mn of profit throughout the period, a YoY growth of 71.2%. The growth are mainly contributed by the rapid growth in the optical networking business. Gross profit has increased 35.4% to HK$237.5Mn. The gross margin however has dropped from 33.7% to 31.8%. Despite research and development cost has increased 22.7% for the same period, operating margin has managed an increase from 5.5% to 8.3% for the same period of the year, due to higher revenue outweighing the relatively smaller increase in administrative cost. Earnings per share has increased from HK$0.04 per share to HK$0.06 per share for the same period of the year.

Strong Growth in Optical Networking Continues

Optical Networking continues to be the primary revenue source and has been the company's main driver of growth in revenue. Optical networking business grew 49.8% against the same period last year, and outperformed the optical networking market, whose growth for the same period was only 16.1%. The high growth achieved by O-Net is caused by strong growth and demand in telecommunication market and data center in North America and Europe, as well as the continuous extension of mobile and optical access network in China.

Expanding Business Portfolio

O-Net actively seeks for new products and technologies. Currently, the company is in talk with two auto manufacturers on possible cooperation of O-Net's LiDAR product on self-driving cars. The construction of manufacturing plant has been completed and therefore no significant capital expenditure is expected in the foreseeable future.

(Closing price as at 23 Sep 2016)

Risk

Increase in raw material price and labour cost

Reduction in profit margin

Slowing economic growth

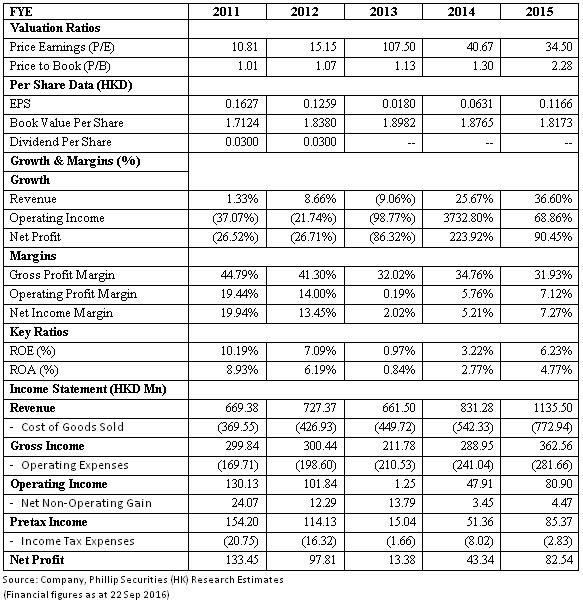

Financials

Click Here for PDF format...