Nearly 40% Increase in Result in the First Three Quarters

China Southern Airlines reported total revenue of RMB86.628 billion in the first three quarters, slightly up by 1.5% YoY, and its net profit attributable to the parent company amounted to RMB6.441 billion, soared by 38% YoY, growing fastest among the Big three Carriers in China. EPS in the first three quarters was RMB0.66, and EPS in Q1, Q2 and Q3 was RMB0.27, RMB0.04 and RMB0.34, respectively, rocketed by 41%, -73% and 180% YoY, respectively, from last year's RMB0.19, RMB0.16 and RMB0.12, respectively.

Declined Fuel Costs: Biggest Contributor

Thanks to the extremely low oil prices in Q1, the average jet fuel price in the first three quarters declined by almost 30% YoY. China Southern Airlines had the largest fleet and the lowest cost of jet fuel among the three airline giants in China, strongly promoting the company's growth in main business performance, with the gross profit margin in the first three quarters reaching the record high.

Less Financial Expenses, Continuously Optimized Debt Structure

China Southern Airlines was the toughest reformer adjusting debt structure among China's three airline giants. Over the period, by issuing RMB bonds and short-term financing bills, as well as repaying short-term and long-term US dollar loans, the company swapped its US-dollar-denominated obligations for RMB-denominated obligations, optimizing the debt structure. The US-dollar-obligations reduced from 93% in late 2014 to 61% in late 2015 and around 49% in 2016. According to current rate, it is estimated that every 1% RMB depreciation will contribute to a mere reduction of RMB310 million in the company's net profit, representing a further decrease in risk exposure. Moreover, the company's debt-to-asset ratio fell from 73.4% in late last year to 70.8% in this year through debt payment. Under the influence, the company's financial expenses in the first three quarters of 2016 plummeted by 33.9% YoY.

Bigger Market Brought by Expanded China-Australia Traffic Rights

Recently Chinese government and its Australian counterpart signed an agreement on traffic right expansion, fully opening the China-Australia third and fourth traffic rights (the aircraft to unload and carry passengers, mails or goods within the territory of each country) and expanding the fifth traffic right to fly via the third country. After many years of development on China-Australia routes, China Southern Airlines, taking the lion share of the market with 36%, will benefit from opening skies to the greatest extent. Meanwhile, its Guangzhou-centered hub network strategy will once again gain momentum.

Investment thesis

The swing of oil prices and exchange rates will cause the fluctuation of airline companies` results in the short run. But we are convinced that, with the counter-cyclical feature, the booming outbound tourism and domestic long-distance tourism will embrace great potential for development in China.

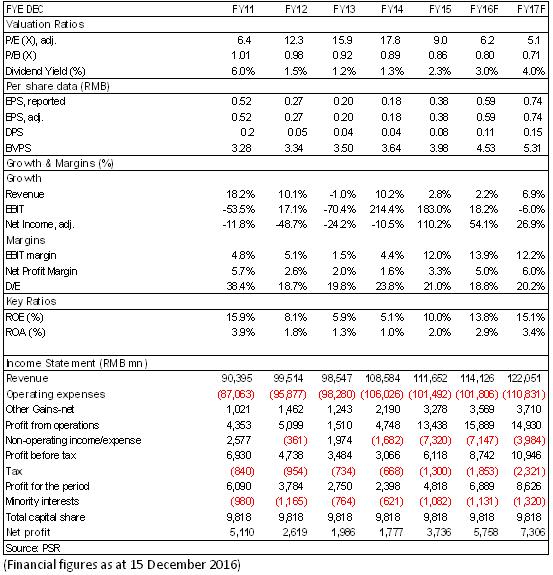

In accordance with the latest data, we adjust the estimate of the Company's EPS to RMB0.59/0.74 in 2016 and 2017. The "Buy" rating is maintained. The target price is HK$5.24, equivalent to 8/6.5x and 1/0.9x estimated P/E ratio and P/B ratio, respectively, in 2016 and 2017.

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast.

War, terrorist attacks, SARS and other emergencies;

Irrational inter-industrial price war;

Financials

Click Here for PDF format...