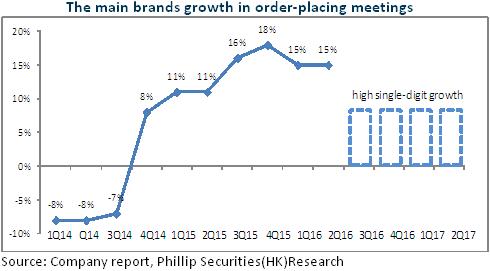

Sustained Spectacular Results in Order-Placing Meetings

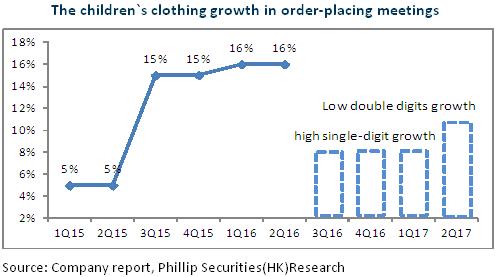

361 Degrees sustained spectacular results in order-placing meetings in autumn and winter of 2016 and spring and summer of 2017. The main brands of 361 Degrees achieved a high single-digit growth in each quarter, while the children's clothing achieved a high single-digit + low double-digit growth. And the company's growth rate of orders continued to take the lead among its counterparts listed on the Hong Kong Stock Exchange. Over the same period, ANTA Sports achieved a high single-digit + mid single-digit growth, while Xtep International achieved a high single-digit + low-to-mid single-digit growth. The company is expected to achieve great results in H2 this year and H1 next year, according to the excellent order results.

Rapid Growth in 361 Degrees Children's Clothing Business

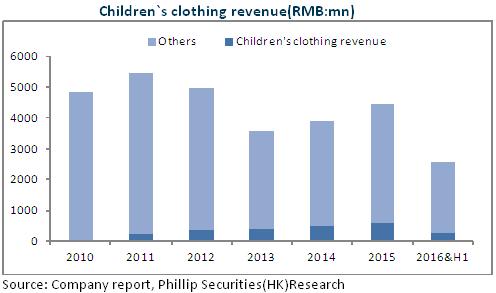

361 Degrees children's clothing has experienced a rapid growth since its launch in 2010. In H1 2016, the revenue soared by 16.5% YoY to RMB272 million, and its proportion as a percentage of the total revenue increased to 10.7%. The department's gross profit margin was partly benefited by the products of high gross profit margin ordered, whose proportion rocketed to 43.1%. Management said the gross profit margin of its department of children's clothing would remain stable at roughly 41%, and its future revenue contribution would be further increased to 11% to 15%, thanks to the full implementation of the two-child policy and the upgrading of consumer spending.

361 Degrees Well-Poised for Overseas Business

361 Degrees overseas business mainly focuses on high-end, differentiation-based functional products. Not only is product performance comparable to world-renowned brands, but the prices are impressive as well. Many series of products, such as Sensation, STRATA, KgM2 and SPIRE, have won good feedback international for their excellent performance. The company will continue to improve the R&D and features of products. In H1 2016 the revenue from overseas business rocketed by 120% YoY to RMB45.2 million, accounting for 1.7% of the total revenue. Thanks to the successful sponsorship of Rio 2016 Olympic Games and Paralympic Games, a significant increase in brand awareness and the rapid expansion of overseas sales outlets are expected to bring considerable revenue to the company, contributing to 2% of the total revenue of the year and around 4% of the year after and beginning to contribute to the company's profits.

Stepping Up Efforts to Boost Operation Efficiency and E-Commerce Growth

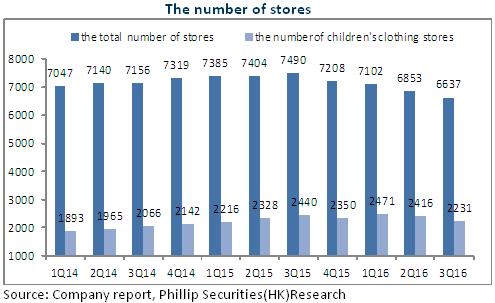

In terms of offline stores, the company will continue to optimize the number of stores, and improve their operation efficiency. As of Q3 2016, the number of offline stores of 361 Degrees has been reduced to 6,637, of which around 67% locate in third-tier or below cities, and the company will maintain an ideal size of around 6,500. Its number of children's clothing stores, is 2,231. In Q3 2016, the sales growth rate of main-brand offline stores and children's clothing stores remained at a high level of 7.3% and 7.3% YoY, respectively, reflecting the strong competitiveness of corresponding products. At present, the average sales volume reached around RMB1.5 to 2.5 million per store, and it is expected to be increased to RMB2.5-3 million.

In terms of online e-commerce, the company will increase the proportion of special products and speed up the development of its channels. In H1 2016 the sales volume of online special products reached RMB166 million, accounting for 6.5% of the total revenue. Currently, the online special product only makes up around 50% of the total sales, and the rest comes from offline store inventory. With the decreased inventory in offline stores, the proportion of online special products will soar to roughly 80%, which is expected to boost the revenue contribution from e-commerce to around 10% to 15%.

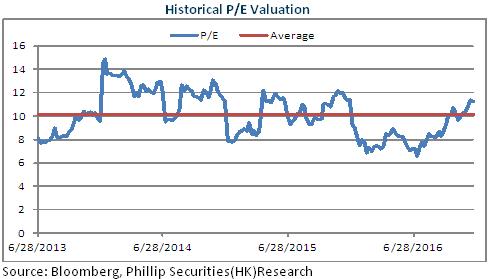

Valuation and Rating

Benefited from the favorable policies and increased sports consumer demand, the company's industry outlook is relatively optimistic. Considering the company's improved operation efficiency and potential growth in overseas business, and the rapid growth in children's clothing business and e-commerce, we give an estimation of 11x EPS in 2017 and the target price is HKD3.82. Also, the "Buy" rating is maintained. (Closing price as at 19 Dec 2016)

Risk Warnings

Macroeconomic downturn and inventory backlog;

Market demand release below expectations;

Results of overseas business expansion below expectations;

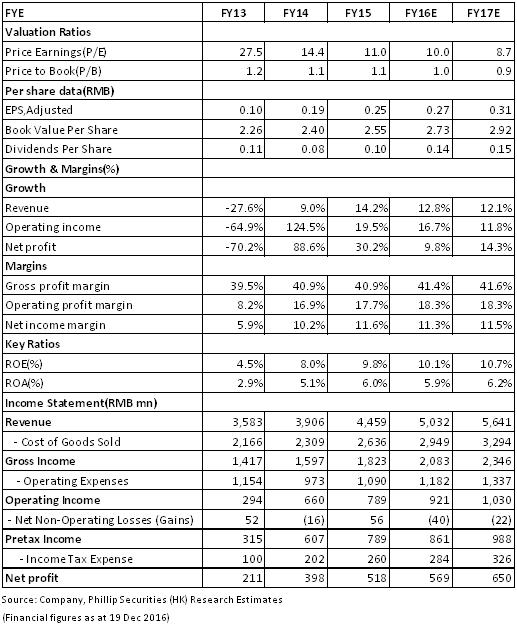

Financials

Click Here for PDF format...