Investment Summary

- Expanding portfolio of investment properties at the heart of Wan Chai, bringing stable cash flow to the companies

- Stable cash flow from Hopewell Highway Infrastructure, which has an 100% dividend payout ratio

- Stable and high dividend yield

Business Overview

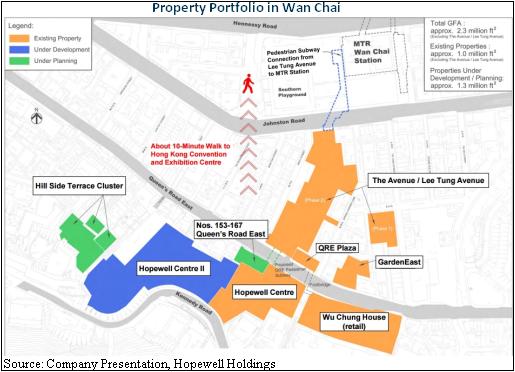

Decades of experience in property sector in Hong Kong: Hopewell Holdings primarily engages in the property investment and development business in both Hong Kong and China. Main property construction projects in the past include Telford Gardens and Healthy Gardens in Hong Kong. Hopewell Holdings is also a large landlord in Wan Chai and the majority of its investment properties, such as Hopewell Centre, and Wu Chung House are located in Wan Chai. In fact, the properties developed by Hopewell Holdings, either for leasing purposes or for selling purposes, are concentrated at the heart of Wan Chai, creating an integrated complex of residential, retail, commercial and hotels. This creates an ecosystem and synergy among the properties via a diversified portfolio of shops, restaurants, commercial and residential properties.

The following map shows the location of properties of the company in Wan Chai:

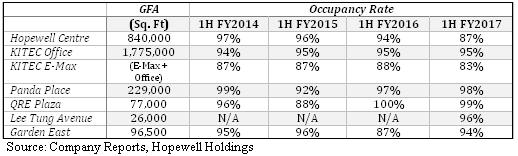

Growth potential from its investment properties: The revenue generated by investment property segment has increased 3% despite there is a drop in the occupancy rate in both Hopewell Centre and KITEC E-Max. The increase is mainly caused by the additional revenue brought by Lee Tung Avenue, which Hopewell Holdings holds 60% via a joint venture with Sino Land.

The following is the summary of occupancy rate:

The decrease in occupancy rate for Hopewell Centre and KITEC E-Max is caused by the tenant reshuffling. In particular, KITEC E-Max has introduced popular brands into the shopping mall gradually in 2016 and by 2018, the fashion outlet will have an additional GFA of 100,000 square foot, subject to government approval. Moreover, according to the interim report, the tenancy agreement with a tenant in the auto mall has been renewed and the rent has more than doubled. We expect KITEC E-Max's occupancy rate to go back up in short term and larger revenue to be obtained from the mall in the future.

The company currently has several investment properties project located at prime locations under development, with some of the land acquired decades ago. Summaries are as follow:

After the completion of the above properties, the total GFA of the investment properties will increase from the current 3.5 million square foot to 4.8 million square foot, an increase of 37.1%. We expect that there will be substantial increase in rental income, because the properties are located at prime location, and will be the main driver of growth in the future.

Prosperous Redevelopment Project in Wan Chai

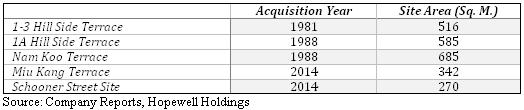

Hill Side Terrace Cluster: Hill Side Terrace Cluster is one of the most valuable projects held by Hopewell Holdings. The company has started acquiring the properties in this project since 1980s and the latest acquisition was performed in 2014. The company currently plans to restore Nam Koo Terrace, a Grade I Historic Building, on the site, and construct a residential building. The development plan has been submitted to Town Planning Board.

The book value of the cluster, as at 31/12/2016, is approximately HK$600Mn. Since some of the properties were acquired in 1980s, we expect the future residential building to provide sizable revenue and cash flow, relative to acquisition cost, to the company.

Hopewell Centre II: A conference hotel with 1,024 rooms will be built with large exhibition and conference facilities. Along with the hotel, offices and retail spaces will be built and the aggregate GFA will be 101,600 square metres. Moreover, the company is experienced in hotel operations, as evident by the consistent high occupancy rate achieved by the Panda Hotel and the recorded high occupancy rate of 97% first achieved in FY2016. The following is the average occupancy rate achieved by the Panda Hotel across years:

The target customer of the Hopewell Centre II conference hotel will be more diversified than that of the Panda Hotel and the target customer will not just the tourists from China, but the business travelers and corporate customers using the conference facilities from all around the world. The target hotel rating for the conference hotel is also expected to be comparable to the top tier hotels located at Central and Admiralty. Hence, the hotel will be able to charge higher room rate because of its location and the built in facilities, bringing stable and sizable cash flow and revenue to the company.

Development in China

Hopewell New Town: This development project is located at Huadu District in Guangzhou and is a composite development project consisting of houses, apartments, and commercial area, with a plot ratio GFA of 1.1 million square metres and 0.45 miillion square metres for the carpark. As at 31/12/2016, about 453,200 square metres of the GFA have been sold and recognised.

In 1H FY2017, the company has already achieved the sales target of Hopewell New Town of CNY600Mn. Currently, the company expects to recognize CNY700Mn of sales in FY2017 because of the good sales achieved in 2016. Starting from 2Q2017, the company will start the pre-sales for FY2018. The following is the company's sales targets:

Besides, the company is investigating the option to develop a commercial area of 150,000 square metres of GFA in Hopewell New Town. With the new MTR Route 9 expected to be opened in 2017 and an exit being constructed near Hopewell New Town, both the potential commercial district and the residential district of Hopewell New Town will benefit from the more convenient transportation infrastructure and we expect that Hopewell will have more pricing power in its sales in the future.

High Dividend Payout Infrastructure Segment

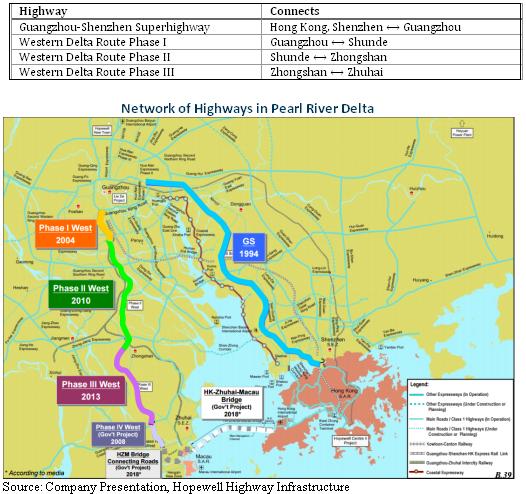

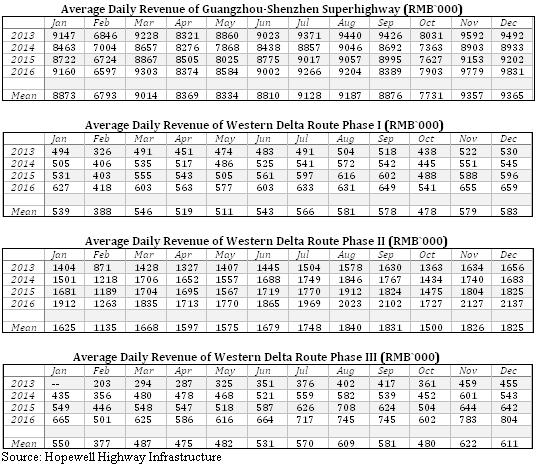

Pearl River Delta highway builder and manager: Hopewell Holdings has a 66.7% owned highway infrastructure construction and management business and is also listed in the Hong Kong Stock Exchange. The highways are located at the coast of Pearl River Delta and connect major cities such as Shenzhen and Guangzhou. The highways are as follow:

Large and steady cash flow business: From the above tables, Hopewell Highway Infrastructure generates large, steady streams of cash flow. Since the company adheres to a 100% dividend payout policy, Hopewell Holdings will be able to directly benefit from the cash flow generated by this highway infrastructure business.

Moreover, according to China Association of Automobile Manufacturers, China sold 28 million vehicles in 2016. Statistics Bureau of Guangdong also releases data that Guangdong's registered car population rose from 13.3 million in 2014 to 14.7 million in 2015, a 10% increase. With the car population increasing in Guangdong region, we expect the trend of large, steady cash flow stream to continue and Hopewell Holdings will continue to benefit from the high dividend payout policy by this highway business.

Financial Overview

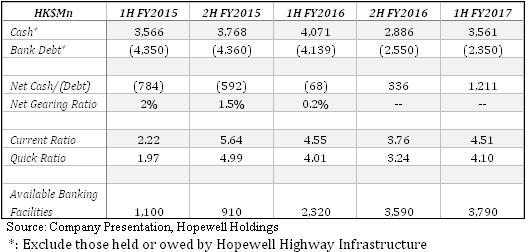

Strong liquidity position: The company has a very strong and gradually increasing liquidity position since FY2015, giving the company a net cash position in rent years. Moreover, the current ratio and quick ratio have been above 3x ever since 2H FY2015, indicating the company has large reserve of cash and liquidity. The company's liquidity position can be further strengthened by the fact that it has a large available banking facilities that can be utilized when needed. The large cash position and the available banking facilities will allow the company to finance its capital expenditure once investment opportunities appear.

The following is the changes in cash and debt of the company over time:

Large amount of revenue from highly liquid business: Property leasing and highway operation are highly liquid business in the sense that rental income are collected monthly and the highway tolls are collected in cash. In particular, the average toll collected in all of the highways between 2013 and 2016, as shown on page 4, is CNY11,370 thousand per day.

The profit attributable to Hopewell Highway Infrastructure is as follow:

The toll collection period are long and the one with earliest expiry date is still more than 10 years away. With Hopewell Highway Infrastructure adhering to a 100% dividend payout policy, we believe the company, which owns 66.7% of Hopewell Highway Infrastructure, can directly benefit from the large stream of cash flow from the highway business.

Valuation

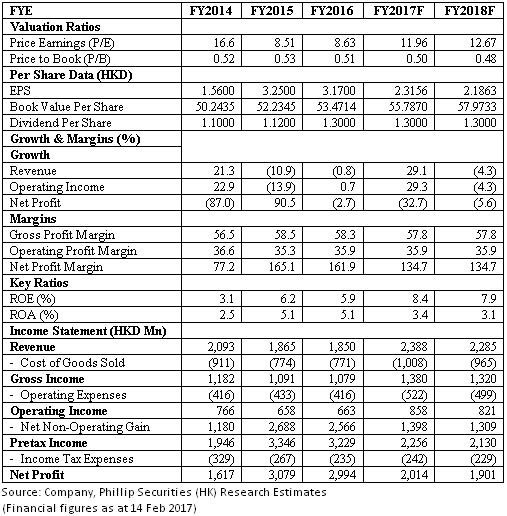

Valuation model suggests a HK$27.70 target price: Because of the diversity of the business of Hopewell Holdings, which comprise property investment and development, highway infrastructure, power generation and hotel operations, Hopewell Holdings is more appropriately considered to be a conglomerate enterprise.

Our sum of parts model suggests a target price of HK$27.70, corresponding to a P/E and P/B of 8.09x and 0.66x respectively, with Neutral rating assigned. (Closing price as at 14 Feb 2017)

Risks

Possible tightening regulations of highway infrastructure: The Chinese government implemented Holiday Toll-Free policy since 2012 National Holiday. The toll-free policy will adversely affect the revenue of the company especially the traffic just prior to, during and just after the holiday period is usually high. If further toll-free policies are implemented, the revenue and profit will be adversely affected.

Competition from other transport means: The Guangzhou-Shenzhen Superhighway currently generates the highest revenue among the highways. However, it may face competition from the new Coastal Expressway and the Guangzhou-Shenzhen-Hong Kong Express Rail Link, which could divert some of the users of the Guangzhou-Shenzhen Superhighway, adversely affecting the revenue and the profit of the company.

Uncertainties in Hopewell Centre II demand: Hopewell Centre II is located at Wan Chai, which has a number of conference and exhibition facilities nearby, such as the Hong Kong Convention and Exhibition Centre. Moreover, the nearby region has many 5 stars hotels and the company may not be able to achieve a very high occupancy rate, like the one achieved by Panda Hotel, especially there will be 1,024 rooms in Hopewell Centre II conference hotel.

Financials

Click Here for PDF format...