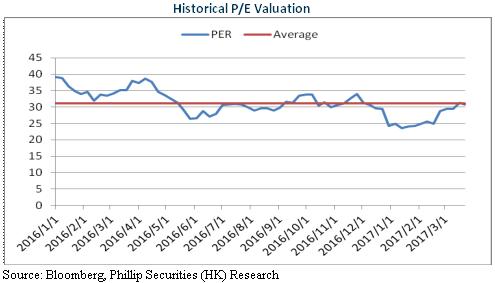

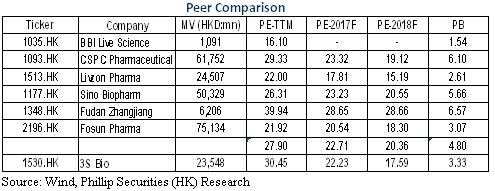

Investment Summary

The company's 2016 performance was in line with expectations. Yisaipu and TPIAO have been included in the National Drug Reimbursement List and are expected to release the potential of rapid growth from the fourth quarter of 2017. Expanding the field of diabetes through externally acquired products shall create growth drivers. And abundant drugs in research will also support the company's mid- and long-term development. As one of the few leading biopharmaceutical companies in China, it is expected to achieve an annualized growth rate of over 20%. We give an estimation of 22x EPS in 2018 with a target price of RMB11.6. And the "Buy" rating is maintained. (Closing price as at 27 Mar 2017)

2016 Performance in Line with Expectations

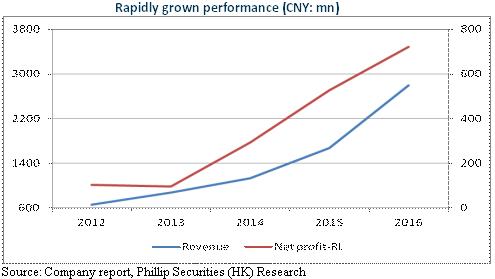

In 2016, 3SBio Inc. reported a revenue of RMB2.8 billion, representing an increase of 62.7% YoY; the net profit attributable to parent company amounted to RMB0.713 billion, surging by 35.4% YoY, with an EPS of RMB0.28 which was in line with market expectation.

TPIAO is one of the core growth points. And its yearly sales increased by 26.4% to RMB0.765 billion, accounting for 27% of total revenue. Besides, Yisaipu was included in the consolidated statement, with a revenue growth of RMB0.786 billion. And the Company's gross profit margin saw a year-on-year increase of 0.1% to 85.6%, with the operating profit margin surging from 29.7% in 2015 to 34.9% in 2016. However, new acquisition loans have led to a surge in financial expenses, with the net interest gain of RMB7 million in 2015 up to the net interest expense of RMB0.124 billion and the core net profit margin seeing a YoY decrease of 2.4% to 25.2%.

Including Core Products in 2017 National Drug Reimbursement List (NDRL) Supporting Development

In H2 2016, the sales growth of TPIAO decreased from 37.4% in the first half to 14.7%. And Yisaipu's sales growth also saw a decrease from the first half's 16.5% to the second half's 4.4%. However, the aforesaid two drugs was included in 2017 NDRL, expanding its potential market tenfold in size than before. And it's expected to support the company's rapid growth.

Compared with Recombinant Human Interleukin-11, the traditional medicine, TPIAO has a better curative effect in treating thrombocytopenia caused by chemotherapy, also with less side effects. But according to the data issued by IMS, TPIAO's market share of treating thrombocytopenia caused by chemotherapy is only 11%. TPIAO is expected to accelerate its replacement of traditional therapies after being included in NDRL. Meanwhile, as an exclusive product, TPIAO shall see a limited decrease in its price and a compound growth rate of 25-30% in its sales.

Besides, currently the penetration rate of monoclonal antibodies in China is lower than that of the world. Yisaipu is the first listed monoclonal antibody, and is also the first domestic biosimilar of Etanercept accepted by the market, and has formed a relatively stable market pattern. After being included in NDRL, given the reimbursement for Yisaipu, its medication course is expected to be prolonged on the basis of present 3-month course and then bring about the increase in its sales. And given its price advantage over imported products, we believe that its sales shall experience a double-digit growth continuously.

Abundant Product Reserve

The company increases its varieties through external acquisition and independent Research & Development. And the company has reached an agreement with AstraZeneca to acquire the exclusive right to commercialize Byetta, Bydureon single dose tray, Bydureon dual chamber pen and Bydureon auto-injector in China to enter the field of diabetes. Byetta has been included in the reimbursement list of nine provinces. Bydureon is projected to make its first contribution to the revenue in the second half of 2017 and become the first GLP sustained release preparation listed in China. These will become the company's new growth drivers. Make an analogy with the international market and we find that Bydureon is expected to grow into a premier variety worth RMB1 billion.

Besides, the company has abundant products in research. It boasts 24 varieties in search, 15 of which are in Research & Development as the National Class New Drugs. In 2016, the company's 5 new drugs have obtained clinical approval. In January 2017, the company appointed Dr. Zhenping Zhu as President of Research & Development and Chief Scientific Officer. Dr. Zhu has extensive research and development experience within the biotechnology industry, especially in the field of antibody therapeutics. It is predicted that the company shall focus on speeding up the clinical trials of products in research and actively expands its product layout.

Risks

Price drop of products exceeds expectations;

Risks of R&D of new drugs.

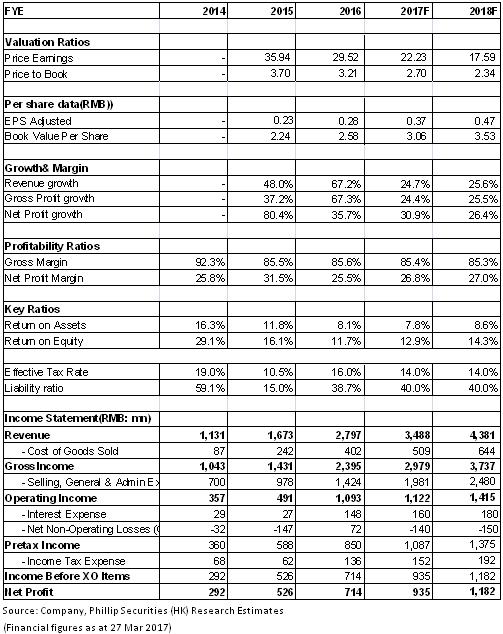

Financials

Click Here for PDF format...