Investment Summary

-The 2016 result was lower than expected, however the valuation is appealing.

-Solid national power consumption figures in first two months, and coal-fired power capacity cut could be beneficial to the group.

-Expected that China coal price correction will continue, beneficial to the coal-power generation costs control.

Company Overview

Huaneng Power International Inc. and its subsidiaries mainly engaged in developing, constructing, operating and managing large-scale power plants throughout China. As of 31 December 2016, the Company is one of China's largest listed power producers with controlling generation capacity of 83,878 MW and an equity-based generation capacity of 76,618 MW. Besides, the Company has commenced operation of certain photovoltaic units and coal-fired generating units recently. According to the company, as of 21 March 2017, the controlled and equity-based generation capacity was 101,116 MW and 89,545 MW, respectively.

According to the firm's 2016 results, total power generated by the Company's domestic operating power plants for the year of 2016 on consolidated basis amounted to 313.69 billion kWh, representing a YoY decrease of 2.13%. The electricity sold amounted to 295.80 billion kWh, representing a YoY decrease of 2.05%. The company realized operating revenue of RMB113.814 billion, representing a decrease of 11.71% YoY, and net profit attributable to equity holders of the Company amounted to RMB8.520 billion, representing a decrease of 37.59% YoY. Earnings per share amounted to RMB0.56. Net assets per share attributable to the equity holders of the Company amounted to RMB5.66, representing an increase of 2.21% YoY, which indicated that the stock is trading at about 18% discount to its book value. The Board claimed that it is satisfied with the Company's results last year. However, the net profit was lower than our expectation.

As expected, along with overall unfavorable business environment of the power generation industry, the firm experienced a tough time in last year. The most obvious problem is that, the price surge of the thermal coal resulted a significant impact on the cost of power generation. Moreover, the Excess Capacity of the power generation industry is another crucial problem. China's industrial power use growth has slowed in resulting the decrease in the power generation. However, the stock is trading at approximate 8.29x FY2016 PE and 0.82x PB Ratio, and providing a fat dividend yield of 6.21%. We believe most unfavorable information possibly has priced in on the stock price. In last 12 months, the stock had underperformed by around 40%, compared with the Hang Seng Index, which the valuation might already become appealing. The national power consumption figures in first two months was solid, the coal-fired power capacity cut could be beneficial to the group, and we expected that China coal price correction continue. Overall, although we agree that 2017 will be a tough year for the group, we are still prudently optimistic about the firm's long-term prospects.

The Valuation is attractive

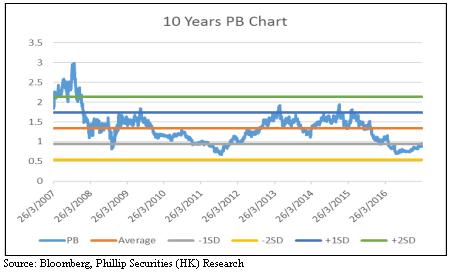

The Chart in below shows 10 years of PB ratio of Huaneng Power, the statistic started on 26/3/2017, with 2 standard deviation banh.

From the chart above, we can see that the PB valuation is significantly lower than the 10 years average. The average 10 years PB ratio is approximately 1.34x, one standard deviation below is 0.94x, and the stock trades significantly below the 10 years average but slightly lower than 1 standard deviation. From the 10 years PB chart, we can see that the valuation of the stock is extremely fluctuate, but since it is trading at significant below the 10 years average, the downside risk possibly limited. At least, in term of the PB ratio, the valuation is attractive.

These were two periods that the firm's Price to Book Ratio similar to now, the first period is during the 2008 financial crisis and the 2011 European debt crisis.

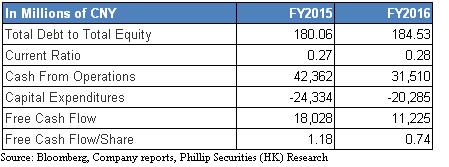

Although the valuation looks appealing by just looking at the PB ratio, the recent profitability, liquidity and operation efficiency are also the important factors. We have collected some key figures in the table below:

According to the 2016 result, although the Total debt to total equity ratios rose very slightly to 184.53, the current ratio stayed the almost same, which indicated the liquidity risk is still low. The group still has an abundant operating cash inflow of RMB 31,510 million, which decreased by 25.62% compared with 2015. Since the Capital expenditure decreased 16.64% to RMB 20,285 million, the group still has free cash flow per share of RMB0.74, which is higher than the earning per share of RMB 0.56. This indicated that the free cash flow of the group is still abundant.

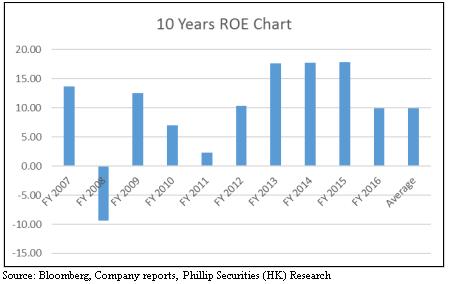

The Return on Equity ratio is also crucial, which can provide more information regarding the profitability of the group.

According to the data we collected, the ROE of FY 2016 is 9.89% wchi is close to its 10 years average of 9.93%, indicating that the profitability is acceptable for the period. The stock only trades at around 0.82x PB ratio currently. The firm's profitability was extremely unfavorable in two periods. The first period was 2008 during the Financial Crisis, the firm's ROE was -9.4%, and the stock traded at lowest PB of 0.82. The second period was 2011 during the European debt crisis, the firm's ROE was only 2.26%, and the stock traded at the lowest PB of 0.67. This could indicated that most of the unfavorable information possibly has already reflected in the stock price, and the group possibly undervalued in recent times due to market overreaction.

Moreover, to find out whether Huaneng Power is undervalued, we used a simple Discounted Dividend Model for evaluating the intrinsic value. The annual market return of HSI that we use for the calculation is 7.16%, which is the data collected from 31th Dec 1995 to 31th DEC 2016. We used the 10 years China government bond yield of 3.27% as the risk free rate, and the historical Beta of the stock is 0.729. From that, we calculated that the required return of the stock is 6.11%. Our forecasted dividend per share for next year is 0.20 RMB per share. Basic on the 10 years average ROE figure, we prudently predict that the ROE will be 50% lower than its 10 years average. And we assumed the dividend payout ratio will stays the same as 50%. As a result, we speculated the dividend growth rate is 2.48%. As a result, we calculated the intrinsic value of RMB 5.51 per share and it is significant higher than its current share price. Therefore, it is reasonable to believe that the stock is undervalued.

Bottomed power consumption, coal-fired power capacity cut

According to the China electricity council, the national total electricity consumption 5.92 trillion KWH, represents an increase of 5.0% YoY. The Power consumption rose 11 percent in the service sector and 10 percent among urban households. Meanwhile, the manufacturing and general business sector posted a 2.9 percent increase to 4.2 trillion kilowatt-hours, making it by far China's largest power consumer. Although China's economy growth slowed, and China possibly switch to less energy-intensive industries in order to be more resource-efficient, but the growth rate of the national total electricity consumption is still 5%, perhaps if the electricity consumption continue to grow steadily, the firm's long-term earning power is still favorable. In February 2017, China's overall social power consumption reached 448.8 billion kilowatt-hours (kWh), a jump of 17.2% from the same month last year. From January to February 2017, China's accumulative social power consumption reached 935.6 billion kWh, an increase of 6.3% from the same period last year, which was 4.3 percentage points higher than the previous year, according to China's National Energy Administration (NEA). This could indicated that the power consumption possibly bottomed in first two months, and expected the power consumption will growth steadily in the future.

Moreover, according to the annual meeting of parliament, the National Development and Reform Commission (NDRC) said it would shut or stop construction of coal-fired power plants with capacity of more than 50 million kilowatts. China moves to a greener growth model and toward use of more renewable energy resources to generate electricity, the burden for capacity cuts in coal-fired power plants will lessen. The capacity cut policy could resulted many smaller power generators become obsoleted and further consolidate the monopoly power of the group. After the capacity cut, the on-grid coal power tariffs is expected to be increase, and the coal power average utilization hours of generating units is expected to rise as well. Overall, we believe that the coal-fired power capacity cut will beneficial to the firm's future earning power.

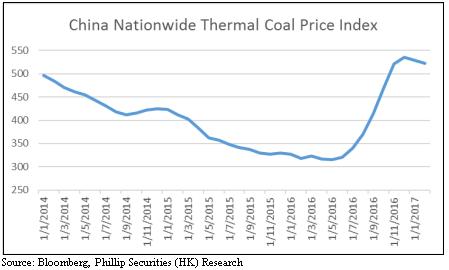

Current China Coal Price is possibly not sustainable

Since the China government has been implemented a successful coal supply-side structural reform, including the strictly production limitation and reduction policy in major coal producing areas, as well as intensified the inspection on illegal coal mines and closure and suspension of mines. The China Nationwide Thermal Coal Price Index, the coal price continue to drop to 522.49 per tonne in Feb 2017. In 2016, the coal price increased roughly more than 60%, according to the data from Bloomberg. The surged coal price had a significant impact on the power of earning of the coal-fired power generation companies, no exception for China Resources Power.

However, the significant price increases disrupted the coal industry's capacity reduction and hurt the business of downstream industries, could cause the serious excess capacity problem reappeared in the coal industry. On the demand side, the end of the winter heating season will also reduce the demand for Coal. As a result, the coal price correction would possibly continue in recent time, it is beneficial to the firm's fuel cost reduction. According to the company result announcement, on the other hand, with the issuance of Notice on Distributing the Memorandum of Stabilizing the Abnormal Fluctuations of Coal Price, Chinese government has established early warning mechanism monitoring price abnormal fluctuation, and make clear that the green range of coal price is between RMB500 to RMB570 per ton. These measures are expected to significantly reduce the possibility of excessive fluctuation of coal price. In 2017, the coal supply and price situations will gradually return to normal. As a result, along with the correction of the coal price, we believe the group's earning power will improve in the future.

Valuation

Taking all the points mentioned above into consideration, Huaneng Power International Inc's target price is therefore $5.91, with Accumulate rating assigned, represents 0.91x FY16 P/B and 0.87x FY17 P/B. (Closing price as at 28 MAR 2017)

Risks

Risks relating to the power demand in China, the overall power demand could keep declining if the economic growth slows down.

Risks relating to coal market, the fluctuation on the coal price will bring certain degree of risks to the fuel cost control

Risks relating to electricity tariff, it could cause uncertainty on the electricity pricing.

Risks relating to environmental protection policies, the national standards for energy saving environmental protection could pushed higher and the environmental protection restrictions for energy development is possibly more tightened.

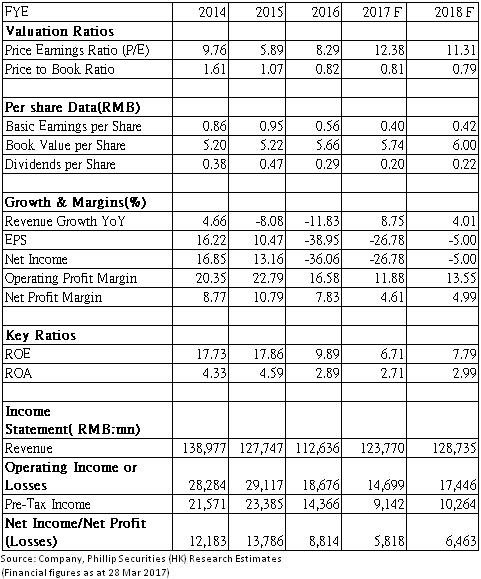

Financials

Click Here for PDF format...