Investment Summary

- 2 new hotels in Washington and Shanghai are expected to open in FY2017

- Hotels are located at prime locations

Business Overview

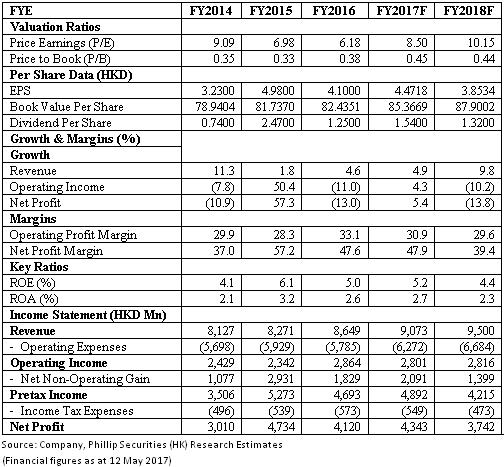

2016 result in line with our expectation: Great Eagle reported the FY2016 result, with revenue increasing 4.7% to HK$8,648.5Mn while net profit decreasing 13.0% to HK$4119.7Mn. The increase in revenue is mainly contributed by the increase in hotel income and rental income from the investment properties. Besides, the large drop in profit is caused by the decrease in the income stemming from the increase in fair value of investment properties owned by Great Eagle. Moreover, in FY2015, Great Eagle had a reversal of impairment on a hotel asset, which is a one off item and does not exist in FY2016. In FY2016, Great Eagle reported an EPS of HK$4.09, a 17.9% drop in comparison with FY2015, and has declared a dividend of HK$0.48 and a special dividend of H$0.50 per share.

Growth in the hotel segment is fueled by the income growth of hotels in North America and Pacific region: The revenue generated by the hotels in North America and Pacific region rose 6.3% and 4.5% respectively. The 6.3% rise in revenue generated by the hotels in North America is caused by the good performance of hotels in Pasadena, Chicago and Toronto. On the other hand, the hotels in New York and Boston have a slight drop in their performance because of the relatively weak performance in the retail and group hospitality segment and the competition brought by AirBnB and various online travel agents reducing information asymmetry.

The Langham Hotels in North America are located in prime locations and therefore will face strong demand and a stable stream of revenue despite the intense competition. For example, The Langham New York is located at The Fifth Avenue and is just a few blocks away from the Empire State Building. The Langham, Chicago is next to DuStable Bridge and Chicago Riverwalk and is within walking distance to the Navy Pier.

Hotel in Europe, i.e. The Langham London, has a weak performance financially because of the part closure, which 109 hotel rooms were being renovated in phases. The average available room in The Langham, London has decreased from 341 rooms to 297 rooms in FY2016. In addition, due to Brexit, GBP has depreciated about 10%, amplifying the downward trend of revenue, which is reported in HKD, even further.

The renovation project was started in November 2015 and was originally scheduled to be completed in 3Q FY2016. However, the renovation project was delayed and was not completed until January 2017. With the renovated hotel rooms coming back to operation, The Langham, London is expected to perform better in FY2017 especially UK tourism has outperformed after Brexit due to the low GBP valuation. The hotel will also be benefit from the renovated rooms, which will allow the hotel to charge higher room rates per night and attract high end retail and corporate clients to the hotel. Moreover, the hotel is at prime location and is located at Regent Street and a few steps away from Oxford Circus, which are highly attractive to tourists. The following is the result of tourism in February 2017 prepared by UK Office for National Statistics:

Stay tuned to the upcoming new hotel development and renovation projects: Great Eagle has obtained a land in Seattle with a consideration of USD18Mn and a size of 19,400 square foot. The site is entitled for a 17-storey hotel but the group is also seeking available options to enhance the prospect from the development of the site. Besides, the group has several hotel renovation projects expected to be commenced in FY2017 and also several hotels to start operating in FY2017. We believe that these new hotel projects will provide solid recurring income to the group.

Several hotels will undergo renovation in FY2017. The renovation work will lead to part closure in these hotels and will adversely affect the revenue of these hotels in short term. However, the renovation will allow the hotels to stay competitive and thus allow the company to charge high room rate in the market despite the highly competitive market.

Hotels owned by Great Eagle and expected to undergo renovation are as follow:

The following is the operating statistics of all the hotels owned by Great Eagle:

Investment property segment achieved good growth: Including the interest Great Eagle has in other entities, Great Eagle achieved a 9.5% growth to HK$2,749Mn in property rental income. The growth in rental income is primarily contributed by the increase in rental income generated by Three Garden Road, which is owned by Champion REIT, which Great Eagle has an equity interest of 67.9%, and whose rental income increased 19.7%. Other investment properties, such as Langham Place Office Tower and Langham Place Mall, also owned by Champion REIT, achieved a growth in rental income of about 6.1% and 3.4% respectively. The following is the operating statistics of the main investment properties of the group:

The revenue from the investment property segment is expected to have mild growth in the coming future since the occupancy rate of the properties are close to 100% except Eaton Serviced Apartments. Unless the rent per square foot can rise sharply or there is new addition to the investment property portfolio, we expect the revenue generated from this segment to be stable with small growth only.

Some property development projects are ongoing: Great Eagle has property development projects in Dalian and Hong Kong. The Dalian project has achieved a loss due to disproportionate of land appreciation tax despite a development profit. The Dalian project will comprise 1,200 high-end residential apartments and 220 of them were delivered in FY2016. Besides, Great Eagle has development project in Pak Shek Kok, Tai Po. The land Great Eagle obtained was the cheapest out of the available land. Pak Shek Kok is one of the luxurious residential district with unobstructed spectacular view of Tolo Harbour. The residential apartment is therefore expected to face high demand and will be sold at solid price. The foundation work has been completed in January 2016 and the superstructure work is expected to start in Mid-2017.

Investment Thesis, Valuation & Risks

Our valuation model suggests a target price of HK$39.30: Great Eagle's hotels are popular around the world and is one of the most popular 5 star hotels in Europe and North America. The investment properties, including those held by Champion REIT, will also provide sizable and stable cash flow and revenue to the company. We are also optimistic towards the Pak Shek Kok development project and expect a good and strong sales. Therefore, a target price of HK$39.30, corresponding to a P/E and P/B of 8.50x and 0.45x, has been assigned, with a `Neutral` rating assigned. (Closing price as at 12 May 2017)

Financials

Click Here for PDF format...