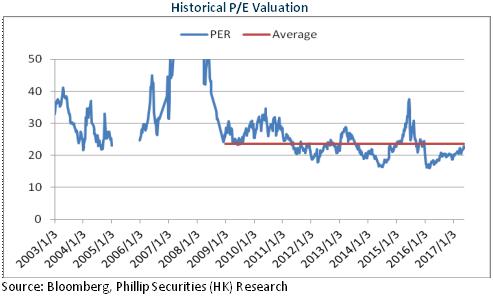

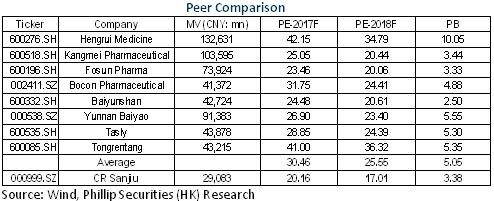

Investment Summary

China Resources Sanjiu (CR Sanjiu) is a leader in domestic OTC field with certain brand bargaining power. In the future, the company intends to provide more plentiful products to raise prices moderately and enhance brand positioning. Meanwhile, the company has successfully finished the adjustment of product structure. The proportion of prescription drugs has continued to increase, and TCM formula granules and Xuesaitong soft capsule will have sound development prospect. With strong channels and terminal resources, the cooperation with Sanofi is expected to bring new growth point for the company, and the future M&A expansion in the field of big health is also worth the wait. We give the company an estimation of 24x EPS in 2017, with a target price of MRB35.38 and "Accumulate" rating initially. (Closing price as at 15 May 2017)

First Quarter Results Benefited from Outward M&A

The revenue and net profit attributable to shareholders of the company in the first quarter of 2017 were RMB24.6 and RMB370 million, respectively, up 15.2 and 20% yoy, equivalent to earnings per share of MRB0.38, which is in line with expectations.

The results of the first quarter significantly outperformed the negative growth in 2016, mainly attributable to Shenghuo Pharmaceutical's inclusion into the consolidated statements in September 2016. In addition, the company has achieved steady growth in original business such as TCM granules and OTC business. Moreover, the cost control of the company was effective. The marketing expense and administrative expense ratio were 35.9% and 6.9%, respectively, down 0.6 percentage point and 2.9 percentage points compared to those in 2016. On the whole, the company's profitability remained stable, with the gross margin and the net profit margin maintaining at approximately 62% and 15%, respectively.

Outward Expansion Will Drive New Growth Points

In 2016, the company completed 100% stake acquisition of Kunming Shenghuo Pharmaceutical which specializes in cardiovascular and cerebrovascular drugs. The main products of Shenghuo Pharmaceuticals include Xuesaitong soft capsules and Huangtengsu soft capsules, forming a complementation with Shenfu injection of the company. It is worth noting that its main product "Lixuwang" Xuesaitong soft capsules was included into 2017 NDRL, so the sales expansion in the future is expected to be accelerated.

The company also signed the Framework Agreement of Cooperation in China to Carry out Consumer Healthcare Business with Sanofi to jointly develop the health consumer goods market in China and set up a joint venture specializing in pediatric and gynecological non-prescription products in China. In addition, the company is selling Sanofi products as a sales agent. Since the beginning of January, the company has become an omni-channel agent of Sanofi's liver product Yishanfu that ranks the forefront in the world, and will gradually introduce its global OTC varieties in the near future. It is believed that Sanofi's pediatric drug brand "Goodbaby", gynecological drug brand "Kangfute" and liver medicine "Yishanfu" will form a good complementation with the company's OTC products and channels, and bring new growth point for the company.

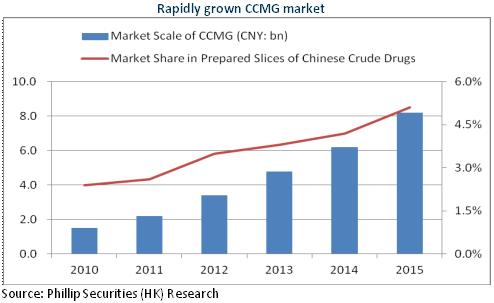

TCM Formula Granules Business Will Grow Rapidly

At present, the domestic business of TCM formula granules only accounts for 5.1% of Chinese herbal pieces business, far behind the rest of the Asia-Pacific region. In addition, TCM granules will extend to secondary hospitals and grassroots hospitals, therefore the prospects for development is broad. At present, CR Sanjiu is approximately occupying a market share of 14%, ranking second in the market. The company is capable of producing about 640 kinds of single-flavor dispensing granules, possessing a certain competitive advantage. The company will also utilize the Chinese intelligent pharmacy and actively promote the sale of TCM formula granules. This business is expected to maintain a growth rate of more than 20%, being one of the main driving forces for prescription drugs.

Risks

The pace of M&A integration was not optimistic as expected;

The business of traditional Chinese medicine injection has continued to decline.

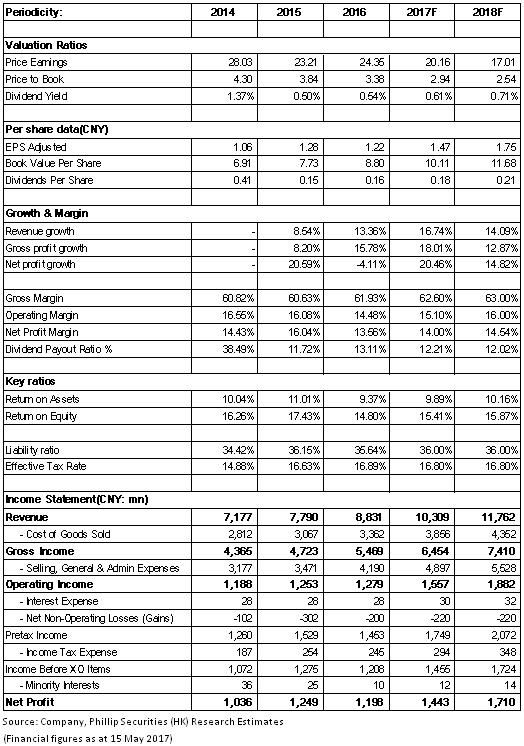

Financials

Click Here for PDF format...