Quarter 1 of 2017 turned losses into gains

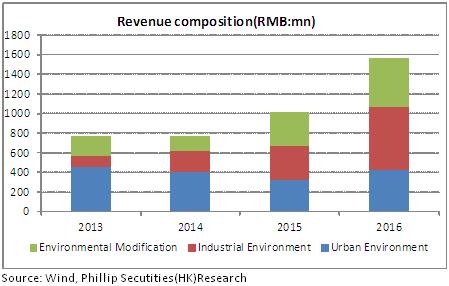

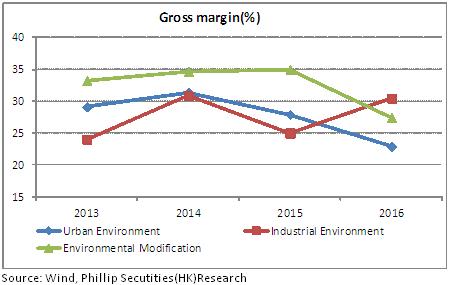

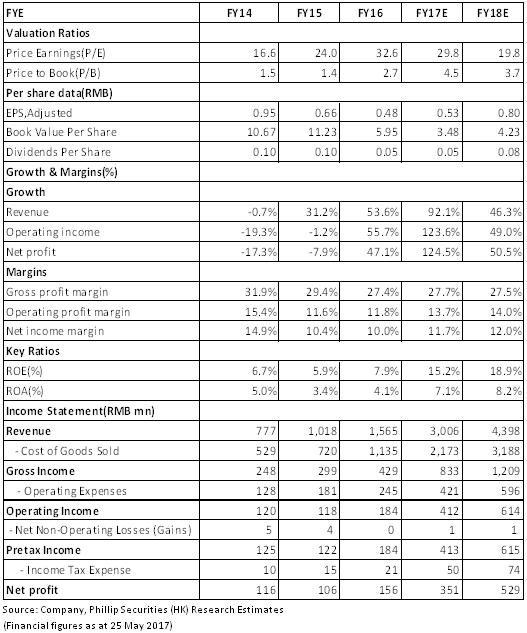

In 2016, Beijing GeoEnviron Engineering & Technology recorded a revenue of RMB1.565 billion, representing a YoY increase of 53.6%. Net profit attributable to shareholders stood at RMB156 million, with a YoY increase of 47.1%. Profits are in line with expectation. Specifically, from the perspective of business type, the revenue from environment modification, industry environment, and urban environment increased by 43.4%, 87.5% and 28.9%, respectively, and with revenue share of 31.8%, 41.2%, and 27%, respectively. Among them, the gross margin of environment modification and urban environment were 27.4% (-7.6%) and 22.9% (-5%), with some degree of decrease. And the total gross margin slipped by 1.9 percent point to 27.43%. From the perspective of business scale, engineering contract generated the dominant revenue, with the proportion of 94.4%, owing to the significant increase of new orders, with a YoY increase of 49.05%. Meanwhile, the gross margin declined by 2.6 percent point because of the fierce competition.

In the first quarter of 2017, the company recorded a revenue of RMB280 million, up140% YoY; the net profit attributable to parent company after deduction of non-recurring profit or loss was RMB3,554,800, turning from loss in the same period of the previous year to profits, a YoY increase of 128.7%. Usually the first quarter is supposed to be slack season with small proportion of annual income. However, this year it is a good start with strong growth. It is predicted that the annual performance would obtain an impressive growth.

Modification and waste business contribute to main growth momentum

Modification and waste business are the core business that the company focuses on. The increase was 2.2 times for modification business orders of 2016, with total amount of RMB1.3 billion. Most of them will contribute to revenue and probably reach the income goal of RMB 1 billion this year. In the following years, the market of soil remediation will be large and hyper-competitive. The company boasts prominent technology and experience and as a result is expected to maintain a stronger contracting ability than others. We predict that the modification orders will improve significantly to RMB2.1-3.0 billion in 2017.

In 2016, the company recorded a revenue of RMB595 million, up 77.5% year-on-year; actual revenue was RMB640 million, a YoY increase of 87.5%. To be specific, several waste projects including Ningdong Nanhu Water Plant are already in the implementation stage. The expansion of waste projects is speeding up, too, covering Xinde Environmental Protection Project, Ningbo Land Project, Keling Environment Protection Project, Jingyuan Hongda Project, Yangxin Pengfu Project and so on. We have obtained the license of dealing with 400,000 tons of waste till the first quarter. With the help of extended acquisition, the growth of waste business in the future is expected to accelerate.

The amount of orders in Quarter 1 of 2017 is RMB533 million, including RMB202 million of environment modification, RMB322 million of industry environment and RMB9 million of urban environment. At present, the amount of order in hand is RMB8.768 billion, of which RMB1.305 billion has been executed and RMB7.463 billion have not. The sufficient contracts are sure to drive business growth of the company.

Heavy financial stress in short term

Low market concentration in the company's business scope, fierce industry competition and downside risks of gross interest rate in short term. At the same time, orders in hand have come to the intensive construction stage and have strong demand of capital. Meanwhile the extension degree is about to increase so the short-term financial stress is big. For specific performance, the asset-liability ratio in recent five years was on the upward trend and rose to 52.3% in 2016. The current ratio and quick ratio declined year by year to 1.04 and 0.39 in 2016, respectively. Although the debt paying stress is increasing, the risk indicators are still under control. Besides, with the gradual accomplishment and operation of projects, the company will receive stable earnings and cash flow. The expected cash flow would take a favourable turn and the financial stress would ease as well.

Valuation and rating

We think that in short time, the enough orders waiting execution and accomplishments of projects would safeguard a high growth of performance. In long term, projects entering into stable operation would drive the continuous development of performance and improvement of cash flow. Based on the estimate, from 2017 to 2018, the company's net profit attributable to the parent company will reach RMB351/529 million, respectively, equivalent to an EPS of 0.53/0.8, respectively, and a PE of 29.8/19.8, respectively. We give a target price of RMB19.4 and the Buy rating. (Closing price as at 25 May 2017)

Risk warnings

Increasing industry competition;

Risk of fund shortage;

Project progress below expectations;

Financials

Click Here for PDF format...