Last Year's Operating Results Fell Short of Expectations

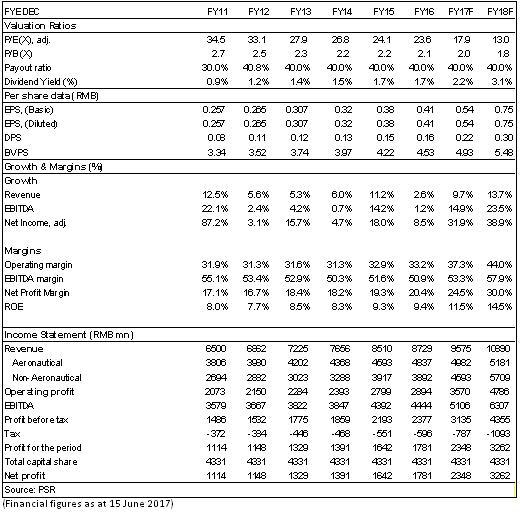

BCIA reported a revenue of RMB8.729 billion in 2016, a slight increase of 2.6% yoy, and a net profit of RMB1.781 billion, an annual growth of 8.5%. The result growth ratio is not only lower than 2015, but also lower than our expectations. EPS was RMB0.41. The figure was RMB0.38 in last year. The final dividend was RMB0.1018, and the annual dividend was RMB0.1645, with the dividend payout ratio remaining 40%. The debt structure was continuously optimized, and the total asset-liability ratio fell from 44% to 42.8%.

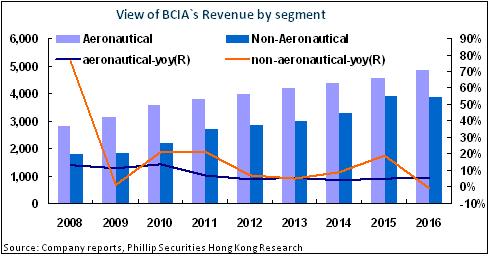

Growth of Airline Business Increased Slightly with Non-aviation Business Falling Unexpectedly

In 2016, the annual aircraft movements reached 610,000 flights, representing an increase of 2.7% yoy; the passenger throughput reached 94.39 million, representing a YOY increase of 5%; the cargo and mail throughput reached 1.94 million tonnes, representing a YOY increase of 2.8%. A slight increase yoy was seen in the growth ratio of aeronautical business over the previous year, and the revenue from aeronautical business rose by 5.3% to RMB4.84 billion.

The main reason for the operating results falling short of expectation was that part of non-aviation business (advertisement, parking revenue, etc.) were restrained under the influence of the current economic environment and industrial competition, and this part of revenue decreased by 0.6% yoy to RMB3.89 billion. Meanwhile, in terms of costs, the operating expense increased by 3.3% YOY to RMB5.79 billion influenced by the new passenger service purchase agreement as well as the increase of security personnel and equipment investment caused by the promotion of aviation security level.

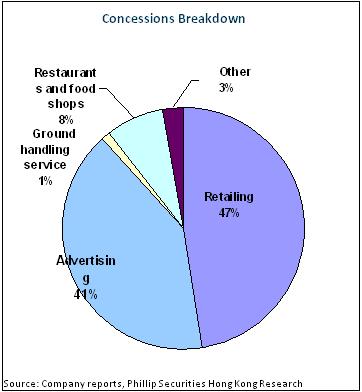

Specifically, the revenue of retail, catering and VIP service in non-aviation business increased by 11% to RMB1.21 billion, 6% to RMB0.2 billion and 70% to RMB97 million YOY, respectively, and the main reasons were the increased consumption of international airline passengers and upgrading of consumption, while advertisement, ground service, other concession service and parking revenue fell by 5% to RMB1.04 billion, 76% to RMB30 million, 30% to RMB70million and 12% to RMB0.16 billion, respectively. The sluggish economy and the impact of internet advertisement on traditional advertisement model resulted in the poor performance of advertisement revenue of the company. The emergence of internet tailored taxi service also imposed negative effects on the parking business of the company. As for the sharp decrease of ground service and other concession service, the reason was that an agreement hasn`t been reached with airlines, causing the delay of the confirming time of the revenue.

The Bidding for Duty-Free Contract Again Will Make the Surge of Non-Aviation Revenue Possible

In the bidding of duty-free retail stores at the Terminal T2 and T3 of Beijing Capital International Airport Company Limited on April 6, 2017, the two highest bidders China Duty Free (Group) Co., Ltd. and Zhuhai Duty Free Enterprises Group Co., Ltd are quite sure to gain the franchise rights in next 8 years, and the company's royalty rate of free-duty business is expected to rise from the current 25% to 47%, better than market expectations. If the above two companies win successfully, it will bring another 30% of profit to the company.

The Beijing Second Airport, which will be put into use in 2019 or after, is possible to influence the company's turnover at the first year largely. However, since Beijing Capital International airport has suffered pressures in capacity growth, it is not a total bad news. Perhaps 20% of the traffic volumes will be transferred when the second airport in first opened, but in three or four years, the conditions will be recovered. Besides, the management of the company plans to make use to this opportunity to further adjust and optimize the structure of traffic volumes and raise the ratio of international tourists.

Valuation and investment thesis

We revised our target price at HK$11.36, equivalent to the 8.6/7x estimated P/EBITDA of 2017/2018. We think recent hike of stock had partly priced in the expectation and therefore we shall give the rating of "Neutral". (Closing price as at 15 June 2017)

Financials

Click Here for PDF format...