Investment Summary

- Several key property development projects will be completed in FY2017, bringing substantial revenue to the company

- Large proportion of stable recurring revenue contributed by the investment property and hotel segments

Business Overview

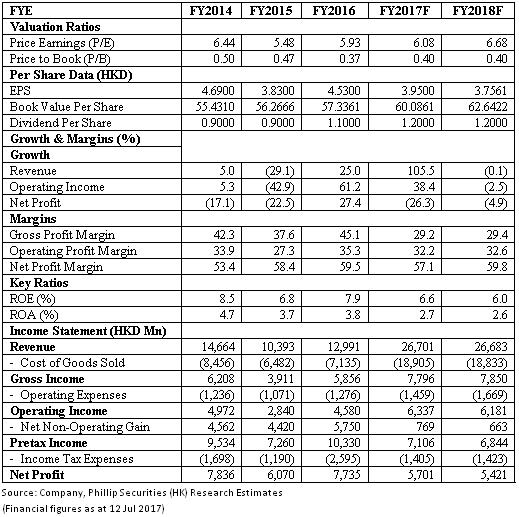

Better than expected FY2016 result: Kerry Properties achieved sizable growth in FY2016. Revenue grew 25.0% to HK$12,991Mn. Gross profit margin increased from 37.6% in FY2015 to 45.1% in FY2016, leading gross profit in FY2016 to increase 49.7% to HK$5,856Mn. The increase in gross profit is mainly caused by the increase in the gross profit margin of the property development segment. In FY2016, Kerry Properties achieved very strong sales. Contracted sales in Hong Kong rose from HK$5.8Bn in FY2015 to HK$12.2Bn in FY2016. Contracted sales in China rose from HK$6.8Bn in FY2015 to HK$14.2Bn in FY2016. Net profit attributable to the shareholders increased 18.2% to HK$6,537Mn. In FY2016, Earnings per Share increased 18% to HK$4.53 and the company declared a final dividend of HK$0.80, 33% higher than last year.

Several major properties will be completed in FY2017: Several major property development projects in both Hong Kong and China will be completed in FY2017. In particular, the HK$12.2Bn contracted sales of Hong Kong segment in FY2016 were primarily the result of the sales of the two key properties in Hong Kong, namely Martin Heights and The Bloomsway. For the HK$14.2Bn contracted sales of China segment, it was mainly contributed by Nanjing Jinling Arcadia Court, Hangzhou Zhijiang Castalia Court and Chengdu Metropolis-Arcadia Court etc. A substantial portion of the contracted sales is expected to be recognised in FY2017 because some projects are expected to be completed in FY2017. The key Hong Kong projects expected to be completed in FY2017 are as follow:

The key projects in China to be completed in FY2017 are as follow:

For the remaining unsold units, particularly those in Hong Kong, Kerry Properties plans to sell the remaining units after the whole projects are completed. In fact, using the data of recent transaction, we expect the remaining units of Martin Heights and The Bloomsway to worth about HK$16Bn, having the potential to add sizable revenue to the company.

Besides, the company has a strong development pipeline and the projects and land reserve are enough for the company's development for the next 4 years. There are several property development projects set to be completed in FY2018 and FY2019. They are located in Beacon Hills, Sai Ying Poon and Ho Man Tin, all of which are expected to aim at high end home seekers and investors and are expected to have strong demand and sales.

Investment properties segment is growing steadily: The investment property segment is expected to have a considerable growth, caused by the completion of a new property originally planned for sales, Shan Kwong Road project. The project has a GFA of 81,217 square foot and provides 106 units. Rent per square foot is expected to be HK$50-HK$70 per month and the annual rental income, assuming a 100% occupancy rate, from the property is expected to be approximately HK$60Mn. The project is expected to be completed in FY2017.

Besides, Kerry Properties also has several large investment properties construction projects ongoing in China, such as the Shenzhen Qianhai projects and Hangzhou Kerry Centre, with completion date ranging from FY2017 to FY2020. The type of properties ranges from residential and office to retail and hotel. Key investment properties under development are as follow:

Investment Thesis, Valuation and Risk

Our valuation model suggests a target price of HK$33.60: Kerry Properties has achieved strong sales in its Hong Kong projects, namely The Bloomsway and Martin Heights, and at the same time has a large and stable stream of recurring revenue from the investment property segment. Moreover, it still has large number of unsold units with high market value in the Martin Heights and The Bloomsway projects, potentially adding large stream of revenue to the company. Therefore, a target price of HK$33.60, corresponding to a P/E and P/B of 6.08x and 0.40x respecitvely, has been assigned, with a `Buy` rating assigned. (Closing price as at 12 Jul 2017)

Financials

Click Here for PDF format...