Investment Summary

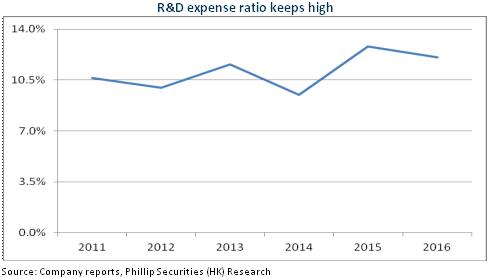

Kanion Pharmaceutical boasts a leading R&D strength in domestic enterprises of Traditional Chinese Medicine, with the R&D expenses maintained over 10% of the company's revenue for years. Although products of TCM injections caused pressure over its previous performance, the company has abundant product lines, among which, the Diterpene Ginkgolides Meglumine Injection has been included in the National Reimbursement Drug List by negotiation and will see a rapid growth of sales volume. With continuous marketing efforts made, the company is expected to reverse the declining growth rates of revenue and performance. The controlling shareholder plans to increase up to 2%'s shares in half a year since June 15, showing its confidence in the new development phase. We give the company an estimation of 28x EPS in 2017 and the target price is RMB20.2, with the "Buy" rating maintained.

Expense ratio increase affects business performance

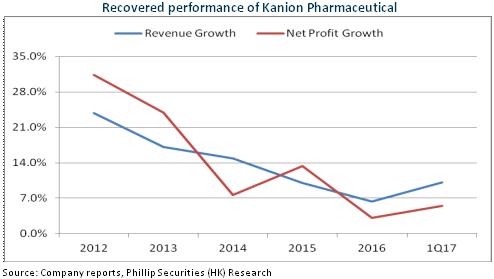

In the first quarter of 2017, the revenue, net profit attributable to the parent company and net profit excluding non-recurring items of Kanion Pharmaceutical were RMB770 million, RMB87 million and RMB82 million, growing YoY 10.2%, 5.4% and 3.5%, respectively. Injections, oral liquid products and tablets and pills grew by 16%, 27.8% and 34.3%, respectively, accounting for 70% of the overall revenue. In terms of injections, Reduning Injection and Diterpene Ginkgolides Meglumine Injection are expected to have grown 10% and 100%.The growth rate of Reduning Injection was less than 2% in 2016, but the potential influenza outbreak in spring drove the sales. Meanwhile, the company has positively promoted its use in hospital departments for adults. Xinnaoxin Pills contributed for most growth in tablets and pills sales. As for oral liquid products, as mainly influenced by the price rise of Jinzhen Mixture, the sales is predicted to reach RMB45 to 50 million, hopefully close to RMB200 million for the whole year.

In addition, the company's gross margin saw moderate but stable growth of nearly 2% in the first quarter. Especially the injections business grew by 2.3%, due to the increasingly obvious advantages brought by the company's scale expansion. However, the increase of expense ratios resulted in a slower performance growth than the revenue growth. Since the company has strengthened its promotion, the sales expense ratio and administrative expense ratio were 43.8% and 14.4%, grew 2.7% and 0.2% YoY, respectively.

Continuous efforts made for marketing reform

Since May 2016, the company had started a marketing reform to transform the formal vertical sales mode divided by product lines into a matrix management mode with product-line sales and regional sales integrated, and to apply a mixed-line sales with anti-infection line and gynaecology line driving the sales of other varieties so that less competitive ones could penetrate deeply into market segments. In the fourth quarter of 2016, the company implemented a responsibility system of hospital administrators to achieve horizontal and vertical coordination between hospital administrators and sales representatives so as to form a three-dimensional sales network in regional markets covering all the terminals and triggering the vitality of sales force.

In the second quarter of 2017, the company announced that it plans to grant 17 million shares of equities, equivalent to 2.76% of its total share capital, to 82 executives and core members, 63 of which are in the marketing system. The exercise price is RMB15.6, to be carried out when the performance targets of 2017 to 2019 are satisfied, with assessment standards set at 13%, 15% and 18.46% for YoY revenue growth rates. The proportion of individual exercise is linked to one's performance assessment results, with exercise proportions for excellent, good, qualified and unqualified staffs set at 100%, 95%, 80% and 60%, respectively. We believe that the equity motivation plan can further motivate the sales persons to reverse the declining growth rates of revenue and performance.

Diterpene Ginkgolides Meglumine Injection can grow rapidly

The company's Diterpene Ginkgolides Meglumine Injection, with effective constituent ginkgolide ABK reaching up to 97%, has a huge edge in material purity and definitive curative effect over its competitors, and is expected to promote the updating and upgrading of Ginkgo preparations and replace its similar low-end varieties. Its daily drug expenditure keeps at a high level, affecting patients` willingness of drug use. But this product has been selected into the new NRDL by negotiation, we think the sales volume will see a rapid growth with the price declining 49%, and it is expected to become another heavy variety like Reduning.

Risks

Progress of marketing reform below expectations;

The price decline of drugs exceeds expectations.

Financials

Click Here for PDF format...