|

|

|

*Advertisement* |

|

|

|

|

|

26 Jul, 2017 (Wednesday) |

IRC(1029)

Analysis:

The K&S project of IRC Limited (1029) achieved satisfactory operating results during the second quarter of 2017. The total production and sales of iron ore concentrate amounted to 380661 tonnes and 376821 tonnes respectively, representing a quarter-to-quarter increase of 20% and 17% respectively. In the first half of 2017, 700000 tonnes of iron ore concentrate were sold, 219% up compared to the Group`s sales in the first half of 2016. The K&S project continues to generate positive cash flow. K&S is currently operating at a steady production capacity of over 50%. The Group aims at operating K&S at close to full capacity on or about the end of 2017. (I do not hold the above stock)

Strategy:

Buy-in Price: $0.325, Target Price: $0.38, Cut Loss Price: $0.30

|

|

CANVEST ENV(1381)

Analysis:

Canvest Environmental Protection, as the largest non-State-owned WTE provider in Guangdong Province, has expanded its business rapidly since going public. Now the Company holds 13 WTE projects which are mainly distributed in Guangdong, Guangxi and Guizhou, and its capacity in operation and total design capacity have reached 8,600 tons/day and 19,240 tons/day, respectively. At present, the Company has enjoyed a 30% market share in Guangdong Province and the percentage is expected to rise to 69% in 2020. In accordance with the Plan for the Construction of Urban Household Waste Harmless Treatment Facilities in the 13th Five-Year Plan Period, the daily MSW treatment capability in Guangdong Province will be improved from 18,400 tons in 2015 to 73,000 tons in 2020, which is one of the WTE markets with highest growth potentials. Meanwhile, the urban household WTE ratio across the country will be increased from 31% in 2015 to 54%. It is predictable that there is vast room for capacity growth of the Company in the future. Canvest Environmental Protection, dedicating to its major industry of WTE, is outstanding in project acquisition capability as well as outstanding operation efficiency. Benefiting from favorable government policies and the expansion of WTE market in Guangdong Province as well as across the country, the Company, with great certainty, enjoys a relatively stable momentum for performance growth in the next three years. We predict that from 2017 to 2018, the Company's revenues will reach HKD2.27 billion and HKD 2.94billion, respectively; net profit HKD 0.54 billion and HKD 0.72 billion, respectively; EPS 0.22 and 0.29, respectively and we set HKD5.0 as its target price, rated as "Buy".

Strategy:

Buy-in Price: $4.17, Target Price: $5.00, Cut Loss Price: $3.80

|

| |

|

Minth Group (425.HK) - Keep the rapidly growing revenue, with stably GP

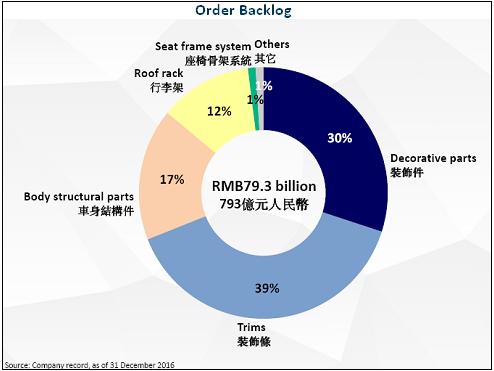

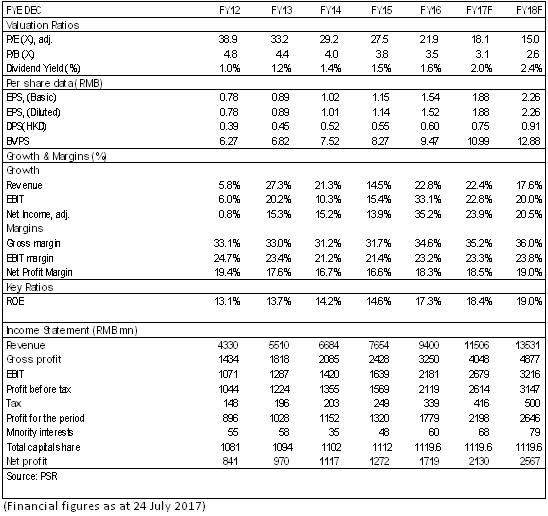

Investment ThesisMinth's operating income keeps increasing rapidly since 2017. It is expected that the increasing trend of the gross profit margin is to continued. We maintain the opinion that Minth's existing businesses indicate a robust growth momentum, while great potential boom lies before the new ones. We believe that it is reasonable to give the company a valuation of 19.9x/16.5x P/E in 2017/2018, equivalent to target price of HK$ 41.45 and Accumulate rating. Keep the rapidly growing revenue, maintain existing orders and undertake new businessWith the explosion of demand for aluminium products, the operating income of the Company keeps increasing rapidly since 2017, and the growth rate of the first five months maintains at approximately 20 percent. In particular, the domestic growth rate is greater than that of the overseas business, with the former greater than 20 percent, while the latter slightly lower than 20 percent. In 2016, the aluminium products of the Company report revenues of two billion, which account for 21% of the total revenues. In 2017, the revenues from aluminium products are expected to increase to about three billion, up 50% year-on-year. In 2019 or 2020, the revenues from aluminium products are expected to be five to six billion. Due to the lead time of part orders, 95% of sales volume in 2017 has been fixed in advance. Since there were 4.4 billion new orders in 2016, the new orders in 2017 are expected to increase to 4.5 billion. Currently, the existing orders of the Company amount to 79.3 billion yuan, 8.4 times the total revenues in 2016. Therefore, the visibility of the future performance is relatively high. The total receivables for 2020 are planned to be over 20 billion by the Company, and the average supporting amount for each car increases from 330 at present to 400 to 500 yuan/car.

Solid financial performance and attractive dividend policyThe Company has a solid financial condition, with only 28% asset- liability ratio and 2.9 billion cash in hand. Besides, its operating net cash flow has increased year by year, and the capital expenditure in 2017 is expected to reach 1.3 - 1.6 billion. With respect to the early personal changes, the Company has made some arrangements. The founder of the Company, Mr. Qin will take in charge for about 1.5 years before the new CEO is chosen and appointed. In addition, the new financial director has been appointed. With the end of the crisis, recently the management has demonstrated their confidence in the Company by increasing their stake. It is believed that the 40% dividend payout ratio will maintain and even increase. The operating capability of overseas business is improved and the trend of stably growing gross profit margin is expected to maintainAfter accumulation for many years, the factories set up at abroad by the Company, such as those in Mexico and America, have been operated gradually smoothly with increasing operating benefits, and the drag of overseas business on the overall gross profit margin is decreasing little by little. In recent years, the Company has successfully expanded the new business orders from ABB, a luxury car brand.(The company is equipped with 30% to 50% of BMW models, including the whole life cycle models of the three and five series.) In the future, the European market will increasingly take the role of the growth engine for the overseas business.

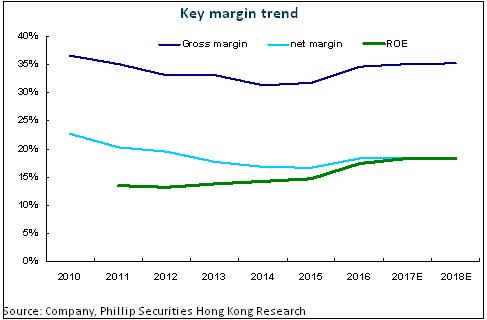

The gross profit margin of the Company provided by it for 2017 is from 34% to 36%. It is thought that the increasing trend of the gross profit margin is expected to maintain, with the aid of increasing demand for aluminium products and decreasing drag from overseas market.

Financials

Click Here for PDF format...

| Recommendation on 26-7-2017 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 37.550 | | Suggested purchase price | N/A | | Target Price | $ 41.450 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong 輝立研究部 – 香港及中國 |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | Goldpac Group | 3315 | 27/03/2017 | Buy | 3 | 2.4 | | O-Net Technologies | 877 | 27/09/2016 | No Rating | | 4.02 | | | Minth Group | 425 | 26/07/2017 | Accumulate | 41.45 | 0.000 | | Inovance Technology | 300124 | 19/07/2017 | Buy | 32.4 | 23.71 | | | | Wisdom Sports Group | 1661 | 11/07/2016 | Buy | 3.3 | 2.18 | | NetDragon | 777 | 16/06/2016 | Buy | 28.4 | 22.9 | | | Kanion Pharmaceutical | 600557 | 25/07/2017 | BUY | 20.2 | 16.17 | | Kanion Pharmaceutical | 600557 | 24/07/2017 | BUY | 20.2 | 16.17 | | | TK Group | 2283 | 20/03/2017 | Accumulate | 2.8 | 2.38 | | TK Group | 2283 | 10/01/2017 | Buy | 2.8 | 2.18 | | | HEC Pharm | 1558 | 02/06/2017 | Buy | 22.24 | 17.08 | | Luye Pharma | 2186 | 22/03/2017 | Buy | 6.3 | 4.95 | | | HN RENEWABLES | 958 | 27/02/2017 | Buy | 3.5 | 2.72 | | CONCORD NE | 182 | 24/10/2016 | Buy | 0.6 | 0.39 | | | L`OCCITANE | 973 | 22/05/2017 | Accumulate | 17 | 15.3 | | L`OCCITANE | 973 | 19/05/2017 | Accumulate | 17 | 15.3 | | | JNBY | 3306 | 13/04/2017 | Accumulate | 6.6 | 5.95 | | CECEP COSTIN New Materials Group | 2228 | 18/10/2013 | Buy | 5.6 | 4.23 | | | Chinasoft International Ltd | 354 | 10/04/2017 | Buy | 5.8 | 4.61 | | Chinasoft International | 354 | 26/10/2016 | Buy | 4.86 | 3.72 | | | Longfor Properties | 960 | 21/07/2017 | Accumulate | 20.35 | 19 | | China Overseas Land & Inv | 688 | 22/06/2017 | Accumulate | 25.1 | 22.85 | | | Yip's Chemical | 408 | 15/06/2017 | No Rating | | 3.29 | | ND Paper | 2689 | 05/04/2017 | Accumulate | 9.5 | 8.35 | | | CANVEST ENV | 1381 | 20/07/2017 | Buy | 5 | 4.16 | | Beijing Enterprises Water Group Limited (BEWG) | 371 | 13/07/2017 | Buy | 7.68 | 6.07 | | | Kerry Properties | 683 | 14/07/2017 | Buy | 33.6 | 26.4 | | Far East Consortium | 35 | 29/06/2017 | Buy | 5.3 | 4.33 | | | IGG | 8002 | 21/11/2014 | Accumulate | 3.95 | 3.44 | | HC INTERNATIONAL | 2280 | 06/11/2014 | Buy | 14.92 | 8.8 | | | Jinjiang Hotels | 2006 | 08/07/2016 | Accumulate | 2.98 | 2.49 | | CUTC | 600358 | 08/03/2016 | N/A | | 10.41 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2017 Phillip Securities (HK) Ltd. All Rights Reserved.

|