Investment Rating

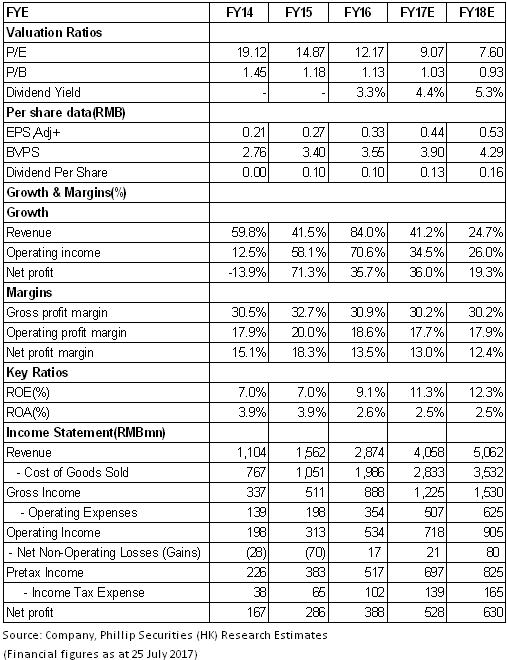

After being listed, Yunnan Water has shown a relatively strong project acquisition capacity, gaining an abundant reserve of PPP projects, and it is predicted that the company will keep strong growth momentum in water treatment industry in the future; meanwhile, there are continuous acquisitions in solid waste treatment field, and with the regular performance contributed by the newly acquired projects, it is hopeful to help the company to achieve significant growth in its performance comprehensively. It is predicted that from 2017 to 2018, the company's revenues will reach RMB 4.06 billion and RMB 5.06 billion, respectively; net profit RMB 528 million and RMB 630 million, respectively; EPS RMB 0.44 and RMB 0.53 , respectively and we set HKD4.6 as its target price, rated as "Buy".

Water and Solid Waste Grow Together

After being listed, Yunnan Water has developed from a single water service supplier into a comprehensive supplier of city environment, mainly engaged in sewage treatment, water supply, solid waste treatment, construction, equipment sales and so on. In recent years, the company has accelerated its expansion to achieve high performance growth. From 2012 to 2016, its compound growth rate reached 63.7%, and the compound growth rate of the net profit attributable to parent company reached 34.1%.

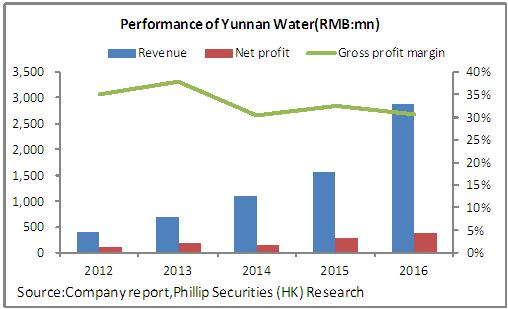

The company achieved an income of RMB2,866 million in 2016, a year-on-year increase of 83.9%; the profit reached RMB414 million, a year-on-year increase of 30.5%. Specifically, all the business items achieved great growth. The sewage treatment segment reached an income of RMB628 million (+49.6%), the water supply segment reached an income of RMB639 million (+40.7%), and the solid waste segment reached an income of RMB425 million compared with only RMB8.2 million during the same period in 2015, whose large increase was mainly driven by the investment and operation of the newly purchased solid waste projects; the construction and equipment sales reached an income of RMB1.11 billion (+85.9%) and other business items reached an income of RMB63 million (-19.6%).

In respect of profitability, the gross profit margin fell by nearly 2% to 30.7%, mainly affected by the relatively low revenue rate of the newly purchased solid waste business and the relatively low unit price of the preliminary service of water supply project. The period expense ratio increased to 20.4% (that was 17% in 2015), mainly due to the multi-channel financing which nearly quadrupled the financial expense to RMB0.22 billion. Affected by the decrease of the gross profit margin and the significant increase of financial expense, the net profit margin fell by 5.9% to 14.5%.

Accelerating the Expansion on Domestic and Overseas Water Market

The company owns 151 water projects in total (including O&M Project), and the treatment amount of water projects reached 4,005,000 tons per day (with 2,025,000 tons per day increased). Specifically, the number of sewage projects under construction and operation is 84 (with 28 increased), the sewage treatment amount is 2,434,000 tons per day (with 1.32 million tons per day increased, +118.5%) and the average sewage treatment fees increased by 10.4% to RMB1.17 per ton; the number of water supply projects under construction and operation is 40 (with 11 increased), and the water supply scale is 1,571,000 tons per day (with 705 thousand tons per day increased, +81.4%); the number of O&M Projects is 27 (with 1 increased) and the daily treatment amount increased 14 thousand tons. The company adheres to a two-wheel driven model of putting technology first and fund second and focuses on the introduction and development of core technologies. OriginWater, the second largest controlling shareholder of the company is a leader in the all-series membrane technology field. Based on the advancing MRB water treatment technology, the company has occupied the water market in Yunnan and accelerated its pace in entering domestic, South Asian and Southeast Asian market.

From 2016 to now, the company has acquired many PPP projects inside and outside the province with a total investment amount of RMB7.03 billion. These projects include the PPP project named "One Water, Two Wastes" (i.e. equipment construction for water supply, sewage and domestic waste treatment in towns) in Jianshui County, Yunnan Province (the investment amount was RMB1,409 million), the black and odorous water body governance PPP project in Jinshuihe, Yuxi City (the investment amount was RMB887 million), the comprehensive governance PPP project in stream entering lake in Erhai, Dali City (the investment amount was RMB800 million) in 2016, the water resources comprehensive utilization and urban and rural sanitation integration PPP project in Luoyuan County, Fujian Province (the investment amount was RMB1,335 million) in 2017 and environment governance and ecological restoration PPP project in Yanjin Lake on Chishui River Basin in Guizhou City (the investment amount was RMB2.6 billion). The abundant project reserve is predicted to bring new driving force for the performance growth of the company in the future.

Solid Waste Treatment Business Grows Rapidly

As of the end of 2016, the company has owned 7 solid waste treatment projects, covering such domestic markets as Yunnan, Fujian and Shandong as well as overseas markets, such as Thailand and Indonesia. The annual solid wastes treatment amount reached 985 thousand tons (with 209 thousand tons increased), with an increase rate of 26.9%. Among them, 6 projects have been put into operation, with an annual treatment scale of 729 thousand tons, and the actual solid waste treatment use ratio is 89.1% (+3.4%). During this period, the company put greater efforts in the technology R&D in waste solid treatment fields like sludge carbonization and waste oxidation to enhance core technologies and equipment manufacture so as to expand source of income. Meanwhile, the company adopts photovoltaic power generation and accurate aeration technologies to reduce energy consumption and operation cost so as to improve profitability. In the future, the company will seize the opportunity brought by "One Belt & One Road" Strategy to expand emerging markets like Southeast Asia and South Asia continuously so as to expand market penetration.

Diversified Financing Channels Help External Acquisition

The company is committed to external acquisition to improve market penetration domestically as well as in Southeast Countries. The total investment and acquisition amount of the company in 2016 reached over RMB4 billion, and the fund of the fast expansion mainly came from the extensive financing channels of the company. During this period, the company issued the first ABS with the sewage treatment and water supply charge right as the basic asset in China and issued financing tools like non-directional debt financing national PPN and corporate bond. Thanks to the diversified financing tools, the average financing cost of the company fell from 6.36% in 2015 to 4.7% and the company's long-term credit rating rose from AA to AA+.

Risk Warnings

Slow implementation of PPP projects;

The profit contribution of acquired projects below expectations;

Related risks brought by cross-border acquisition.

Financials

Click Here for PDF format...