|

|

|

*Advertisement* |

|

|

|

|

|

28 Jul, 2017 (Friday) |

|

|

YUNNAN WATER(6839)

Analysis:

After being listed, Yunnan Water has developed from a single water service supplier into a comprehensive supplier of city environment, mainly engaged in sewage treatment, water supply, solid waste treatment, construction, equipment sales and so on. In recent years, the company has accelerated its expansion to achieve high performance growth. From 2012 to 2016, its compound growth rate reached 63.7%, and the compound growth rate of the net profit attributable to parent company reached 34.1%.The company achieved an income of RMB2,866 million in 2016, a year-on-year increase of 83.9%; the profit reached RMB414 million, a year-on-year increase of 30.5%. Specifically, all the business items achieved great growth. The sewage treatment segment reached an income of RMB628 million (+49.6%), the water supply segment reached an income of RMB639 million (+40.7%), and the solid waste segment reached an income of RMB425 million compared with only RMB8.2 million during the same period in 2015, whose large increase was mainly driven by the investment and operation of the newly purchased solid waste projects; the construction and equipment sales reached an income of RMB1.11 billion (+85.9%) and other business items reached an income of RMB63 million (-19.6%).After being listed, Yunnan Water has shown a relatively strong project acquisition capacity, gaining an abundant reserve of PPP projects, and it is predicted that the company will keep strong growth momentum in water treatment industry in the future; meanwhile, there are continuous acquisitions in solid waste treatment field, and with the regular performance contributed by the newly acquired projects, it is hopeful to help the company to achieve significant growth in its performance comprehensively. It is predicted that from 2017 to 2018, the company`s revenues will reach RMB 4.06 billion and RMB 5.06 billion, respectively; net profit RMB 528 million and RMB 630 million, respectively; EPS RMB 0.44 and RMB 0.53 , respectively and we set HKD4.6 as its target price, rated as "Buy".

Strategy:

Buy-in Price: $3.51, Target Price: $4.60, Cut Loss Price: $3.00

|

| |

|

Champion REIT (2778.HK) - Disposal of Asset Releases the Value of the Trust

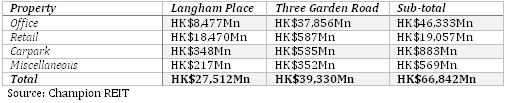

Investment Summary- Attempting to sell Langham Place Office Tower. If the disposal is successful, the Trust is expected to receive large stream of cash flow - With Murray Road Carpark land sold at a price per square foot of about HK$50,000 by the Government, the Trust's property, Three Garden Road, is expected to benefit from that valuation, if the Trust is looking to sell Three Garden Road in the future Business OverviewProperties at prime locations: Champion REIT owns three properties, namely Three Garden Road, Langham Place Mall, and Langham Place Office Tower, which are located either at Central or Mong Kok. Although the Trust only has three investment properties, these properties are valuable and produce large stream of cash flow and rental income to the Trust. The details of the three properties are as follow:

The Trust announced the disposal of Langham Place Office Tower: In July 2017, Champion REIT announces the potential disposal of Langham Place Office Tower. In FY2016, Langham Place Office Tower contributed HK$325Mn of rental income to Champion REIT, representing about 14.1% of the total rental income Champion REIT generated during the year. In terms of net property income, Langham Place Office Tower has a higher contribution, providing HK$295Mn of and representing 14.6% of the total net property income. According to the FY2016 annual report, the fair value of Langham Place Office Tower was HK$8,477Mn. In fact, Langham Place Office Tower only represents a small portion of the investment property portfolio of the trust, with its valuation contributing only 12.7% of the fair value of the entire investment property portfolio of the trust.

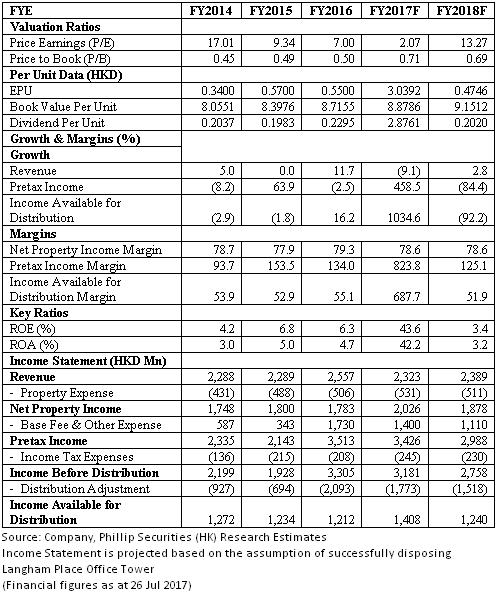

The potential disposal of Langham Place Office Tower may imply a payment of special dividend by the Trust: On 18/7/2017, Savills was appointed as the principal agent for the global tender sale of Langham Place Office Tower, with the indicative price range of the tower between HK$24.5Bn and HK$25.0Bn, about 190% higher than the fair value of the property on the financial statement. As at 31/12/2016, the Trust had HK$14,841Mn debt outstanding. If Langham Place Office Tower is sold successfully at the indicative price and the proceeds are used to repay all of the outstanding debt, the Trust will still have approximately HK$10Bn on hand. Therefore, the disposal may mean the Trust can distribute the excess cash in the form of special dividend. The ordinary dividend however may decrease due to the lower profit, a result of the disposal of the Langham Place Office Tower. The tender for Murray Road Carpark is potentially beneficial: In May 2017, the Murray Road Carpark land, which has a GFA of 465,005 square foot, was sold at a recorded price of HK$23.28Bn, equivalent to a price per square foot of HK$50,063. This is potentially beneficial to the valuation of the Three Garden Road, which is located close to the Murray Road Carpark land. Moreover, Three Garden Road's GFA is 1,638,000 square foot, about 250% larger than that of the Murray Road Carpark land. If Champion REIT considers to sell Three Garden Road, which is currently valued at about HK$24,000 per square foot on the financial statement, the value of the property, coupled with the positive effect brought by the tender of Murray Road Carpark land, will be released, thereby bringing sizable cash flow to the Trust. Investment Thesis, Valuation and RiskOur valuation model suggests a target price of HK$6.30: Our valuation model is based on the NAV per unit. Given by the fact that Champion REIT's investment properties are all high quality and located at prime locations and the potential disposal of Langham Place Office Tower will release the value of the property by bringing sizable cash flow and gain to the company, we expect the Trust will have a large increase in distributable income in FY2017. Moreover, the sales proceed, if Langham Place Office Tower is successfully sold, will be more than enough to repay all of the debt of the Trust. Therefore, a target price of HK$6.30, corresponding to a 29% discount to NAV and a `Neutral` rating, has been assigned. (Closing price as at 26 Jul 2017)

Financials

Click Here for PDF format...

| Recommendation on 28-7-2017 | | Recommendation | Neutral | | Price on Recommendation Date | $ 6.080 | | Suggested purchase price | N/A | | Target Price | $ 6.300 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong 輝立研究部 – 香港及中國 |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | Goldpac Group | 3315 | 27/03/2017 | Buy | 3 | 2.4 | | O-Net Technologies | 877 | 27/09/2016 | No Rating | | 4.02 | | | Minth Group | 425 | 26/07/2017 | Accumulate | 41.45 | 37.55 | | Inovance Technology | 300124 | 19/07/2017 | Buy | 32.4 | 23.71 | | | | Wisdom Sports Group | 1661 | 11/07/2016 | Buy | 3.3 | 2.18 | | NetDragon | 777 | 16/06/2016 | Buy | 28.4 | 22.9 | | | Kanion Pharmaceutical | 600557 | 25/07/2017 | BUY | 20.2 | 16.17 | | Kanion Pharmaceutical | 600557 | 24/07/2017 | BUY | 20.2 | 16.17 | | | TK Group | 2283 | 20/03/2017 | Accumulate | 2.8 | 2.38 | | TK Group | 2283 | 10/01/2017 | Buy | 2.8 | 2.18 | | | HEC Pharm | 1558 | 02/06/2017 | Buy | 22.24 | 17.08 | | Luye Pharma | 2186 | 22/03/2017 | Buy | 6.3 | 4.95 | | | HN RENEWABLES | 958 | 27/02/2017 | Buy | 3.5 | 2.72 | | CONCORD NE | 182 | 24/10/2016 | Buy | 0.6 | 0.39 | | | L`OCCITANE | 973 | 22/05/2017 | Accumulate | 17 | 15.3 | | L`OCCITANE | 973 | 19/05/2017 | Accumulate | 17 | 15.3 | | | JNBY | 3306 | 13/04/2017 | Accumulate | 6.6 | 5.95 | | CECEP COSTIN New Materials Group | 2228 | 18/10/2013 | Buy | 5.6 | 4.23 | | | Chinasoft International Ltd | 354 | 10/04/2017 | Buy | 5.8 | 4.61 | | Chinasoft International | 354 | 26/10/2016 | Buy | 4.86 | 3.72 | | | Longfor Properties | 960 | 21/07/2017 | Accumulate | 20.35 | 19 | | China Overseas Land & Inv | 688 | 22/06/2017 | Accumulate | 25.1 | 22.85 | | | Yip's Chemical | 408 | 15/06/2017 | No Rating | | 3.29 | | ND Paper | 2689 | 05/04/2017 | Accumulate | 9.5 | 8.35 | | | YUNNAN WATER | 6839 | 27/07/2017 | Buy | 4.6 | 3.47 | | CANVEST ENV | 1381 | 20/07/2017 | Buy | 5 | 4.16 | | | Champion REIT | 2778 | 28/07/2017 | Neutral | 6.30 | 0.000 | | Kerry Properties | 683 | 14/07/2017 | Buy | 33.6 | 26.4 | | | IGG | 8002 | 21/11/2014 | Accumulate | 3.95 | 3.44 | | HC INTERNATIONAL | 2280 | 06/11/2014 | Buy | 14.92 | 8.8 | | | Jinjiang Hotels | 2006 | 08/07/2016 | Accumulate | 2.98 | 2.49 | | CUTC | 600358 | 08/03/2016 | N/A | | 10.41 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2017 Phillip Securities (HK) Ltd. All Rights Reserved.

|