|

|

|

*Advertisement* |

|

|

|

|

|

31 Jul, 2017 (Monday) |

|

|

Longma Environm(603686)

Analysis:

Longma Environmental Sanitation Equipment Co., Ltd is a professional supplier of sanitation equipment and service. The company has maintained compound annual growth rates of 20-25% for the last few years. In 2016 it recorded a revenue of RMB2.218 billion, increasing by 44.8% year-on-year. Its net profit attributable to shareholders of parent company amounted to RMB211 million, up by 40.2% year-on-year, and the basic EPS was RMB79 (+31.67%), with the performance expected to grow.(1) Regarding the business of sanitation equipment, Longma has an edge over its competitors, and the company is expected to grow steadily due to the overall improvement of sanitation equipment.(2) There is a blue ocean market for sanitation service, where Longma holds great first-mover advantages, and its future growth is highly resilient. Therefore, it is expected that the company will record a revenue of RMB 3,139 million and RMB 4,206 million, net profit of RMB 281 million and RMB 390 million, EPS of RMB1.03 and RMB1.44 in 2017 and 2018, respectively. Based on the information, the target price of RMB 41.2 is given, and the company is rated Accumulate.

Strategy:

Buy-in Price: CNY31.82, Target Price: CNY41.20, Cut Loss Price: CNY29.00

|

| |

|

Report Review of July. 2017

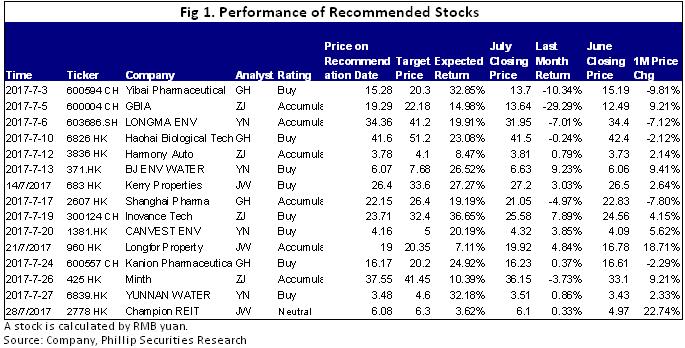

Sectors: Mainland Pharmaceuticals &Telecom (Fanguohe), Air, Automobiles (ZhangJing), Environmental protection (Wang Yannan), Property Development & Investment (John Wong) Mainland Pharmaceuticals &Telecom (Fan guohe)In July I released five equity reports including Yibai Pharmaceutical (600594.CH) , Haohai Biological Technology (6826.HK), Shanghai Pharma (6826.HK), Kanion Pharmaceutical (600557.CH) and Livzon Pharmaceutical (1513.HK). Over the past three years, oseltamivir phosphate (Kewei) has recorded a growth of ten times. It is expected to maintain high growth in the future with factors such as the inclusion of granules into the national drug reimbursement list(NDRL) 2017 version and the market expansion of pediatric drugs. With the R&D support from the group and the affluent product reserves of HEC Pharm, insulin and hepatitis C drugs are expected to have subsequent growth. In addition, the reorganization of the company and the group A-share subsidiary Dongyang Guangke is also expected to receive support from A-share market funds. We give the company an estimation of 18x EPS in 2017 and a target price of HKD22.24, with the "Buy" rating maintained. Automobile & Air (ZhangJing)This month I released 4 equity reports including GBIA (600004 CH), Harmony Auto (3836 HK), Inovance Technology (300124 CH) and Minth (425 HK). For the long run, we prefer the Inovance Technology first. The company realized an income of RMB0.782 billion in 2017Q1, a year-on-year increase of 37.7%; net profit attribution stood at RMB0.172billion, a year-on-year increase of 23.54%. Gross profit margin fell by 1.55 percentage points to 46.6%, mainly due to China's new energy vehicle market influenced by policy interference in the first quarter. As China's new energy vehicle market rebounded, we believe that from the second half of 2017, factors of perturbing gross profit margin to decline brought by new business will gradually vanish. The company's performance will return to high growth. Environmental protection (Wang Yannan)In July I released 4 equity reports, including Longma ENV(603686.SH), BJ ENV WATER(371.HK ),CANVEST ENV (1381.HK),YUNNAN WATER(6839.HK). Beijing Enterprises Water Group affiliates to the state-owned enterprise Beijing Enterprises Group Company Limited. The Company's main business included water treatment services (sewage treatment + water supply), water environment governance and construction (comprehensive governance + BOT water services) and technical services. As at the end of 2016, the Company had 452 water plants, covering 25 provinces/autonomous regions/ municipalities directly under the Central Government in China and parts of overseas regions. Its total design capacity reaches 27,168,000 tons/day and the water handling capacity reaches 16.48 million tons/day. The scale ranks the top in China stably. The Company will maintain rapid development with the benefit from the release of PPP performance and the promotion of industry concentration. Furthermore, the widespread use of the light asset model of the PPP+ industry fund is expected to be a catalyst for boosting the Company's share price. We estimate that, from 2017 to 2018, the revenues of the Company will reach RMB24,545 million and RMB31,909 million, respectively; the net profits RMB 4,165 mbillion and RMB 5,264 million, respectively; EPS RMB 0.48 and RMB 0.60, respectively. We give a target price of HKD7.68 and the rating "Buy". Property Development & Investment (John Wong)In July, I have issued 3 research reports on Kerry Properties (683.HK), Longfor Property (960.HK) and Champion REIT (2778.HK). In particular, Kerry Properties has sizable room for growth especially they have several major properties being completed in FY2017, including Martin Heights in Ho Man Tin and The Bloomsway in So Kwun Wat. Kerry Properties has started the pre-sales for these properties in FY2017 and they have achieved good results so far. As at 31/12/2016, Kerry Properties sold 39% and 79% of the units in Martin Heights and The Bloomsway respectively. According to the information released by the company, Kerry Properties achieved HK$12.2Bn accumulated contracted sales in Hong Kong while it achieved HK$14.2Bn accumulated contracted sales in China. This will provide assurance to the company's future result especially the one in FY2017. Besides, the company has a large investment property segment, brining sizable recurring revenue and cash flow to the company. Moreover, there will be several large investment properties being added in the next few years, such as Shenyang Kerry Centre and the Shenzhen Qianhai projects, providing 5.7Mn square foot and 2.5Mn square foot of GFA respectively, thereby continuing to provide growth prospect to the company in the future. Therefore, we have assigned Kerry Properties a target price of HK$33.60, equivalent to a `Buy` rating.

Click Here for PDF format...

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong 輝立研究部 – 香港及中國 |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | Goldpac Group | 3315 | 27/03/2017 | Buy | 3 | 2.4 | | O-Net Technologies | 877 | 27/09/2016 | No Rating | | 4.02 | | | Minth Group | 425 | 26/07/2017 | Accumulate | 41.45 | 37.55 | | Inovance Technology | 300124 | 19/07/2017 | Buy | 32.4 | 23.71 | | | | Wisdom Sports Group | 1661 | 11/07/2016 | Buy | 3.3 | 2.18 | | NetDragon | 777 | 16/06/2016 | Buy | 28.4 | 22.9 | | | Report Review of July. 2017 | | 31/07/2017 | | | 0.000 | | Kanion Pharmaceutical | 600557 | 25/07/2017 | BUY | 20.2 | 16.17 | | | TK Group | 2283 | 20/03/2017 | Accumulate | 2.8 | 2.38 | | TK Group | 2283 | 10/01/2017 | Buy | 2.8 | 2.18 | | | HEC Pharm | 1558 | 02/06/2017 | Buy | 22.24 | 17.08 | | Luye Pharma | 2186 | 22/03/2017 | Buy | 6.3 | 4.95 | | | HN RENEWABLES | 958 | 27/02/2017 | Buy | 3.5 | 2.72 | | CONCORD NE | 182 | 24/10/2016 | Buy | 0.6 | 0.39 | | | L`OCCITANE | 973 | 22/05/2017 | Accumulate | 17 | 15.3 | | L`OCCITANE | 973 | 19/05/2017 | Accumulate | 17 | 15.3 | | | JNBY | 3306 | 13/04/2017 | Accumulate | 6.6 | 5.95 | | CECEP COSTIN New Materials Group | 2228 | 18/10/2013 | Buy | 5.6 | 4.23 | | | Chinasoft International Ltd | 354 | 10/04/2017 | Buy | 5.8 | 4.61 | | Chinasoft International | 354 | 26/10/2016 | Buy | 4.86 | 3.72 | | | Longfor Properties | 960 | 21/07/2017 | Accumulate | 20.35 | 19 | | China Overseas Land & Inv | 688 | 22/06/2017 | Accumulate | 25.1 | 22.85 | | | Yip's Chemical | 408 | 15/06/2017 | No Rating | | 3.29 | | ND Paper | 2689 | 05/04/2017 | Accumulate | 9.5 | 8.35 | | | YUNNAN WATER | 6839 | 27/07/2017 | Buy | 4.6 | 3.47 | | CANVEST ENV | 1381 | 20/07/2017 | Buy | 5 | 4.16 | | | Champion REIT | 2778 | 28/07/2017 | Neutral | 6.3 | 6.08 | | Kerry Properties | 683 | 14/07/2017 | Buy | 33.6 | 26.4 | | | IGG | 8002 | 21/11/2014 | Accumulate | 3.95 | 3.44 | | HC INTERNATIONAL | 2280 | 06/11/2014 | Buy | 14.92 | 8.8 | | | Jinjiang Hotels | 2006 | 08/07/2016 | Accumulate | 2.98 | 2.49 | | CUTC | 600358 | 08/03/2016 | N/A | | 10.41 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2017 Phillip Securities (HK) Ltd. All Rights Reserved.

|