Investment Summary

- Renovation of The Peninsula Beijing will provide substantial growth in RevPAR and is expected to more than offset the effect on revenue caused by the decrease in number of rooms

- New hotel construction projects are on good track

Business Overview

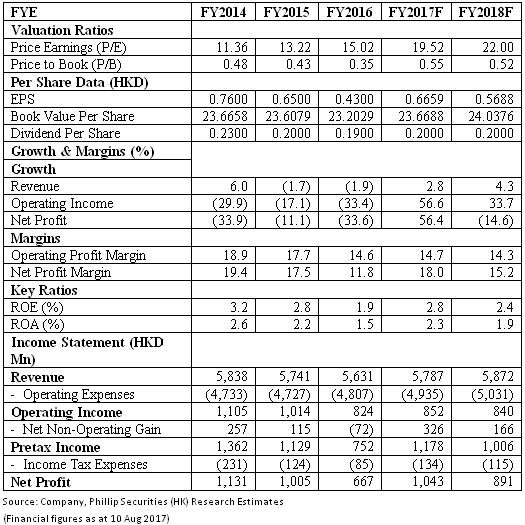

1H2017 result was better than our expectation: Hongkong & Shanghai Hotels had a tiny drop in revenue of about 0.4% to HK$2,596Mn in 1H2017. However, EBITDA increased 7% to HK$561Mn, primarily because of the general recovery in the hotel segment. Profit attributable to the shareholders increased 162% in 1H2017 to HK$519Mn. The reason for the rapid increase in profit attributable to the shareholders is throughout 1H2017, the increase in fair value of investment properties increased 565% to HK$359Mn, which contributes to a substantial proportion of the increase in the profit. Out of the HK$359 revaluation gain, a large majority of the increase in fair value was contributed by The Repulse Bay Complex. Excluding the fair value changes of investment properties and other non-recurring items attributable to shareholders, the underlying profit increased 19%, representing a HK$0.12 underlying earnings per share.

The Peninsula Beijing renovation are being completed in phases: In FY2015, the company started the renovation of The Peninsula Beijing. The first phase was completed in September 2016 and the second phase is expected to be completed in August 2017. Originally, there were 525 rooms in The Peninsula Beijing but after the renovation, the rooms has been combined and the number of room has decreased to 230. However, the size of the room has increased and is the largest in Beijing, allowing the hotel to become the market leader in terms of room rates in 1H2017. The dining outlets have been renovated and the shopping arcade has successfully retained most of the tenants. In particular, the company has implemented a strategy to focus on diplomatic and group booking so that The Peninsula Beijing could take advantage of the increasing number of conferences taking place in Beijing.

Benefitting from the renovation of The Peninsula Beijing and the expansion of the rooms, The Peninsula Beijing had a sizable growth in 1H2017, with RevPAR increasing by almost 300%. Therefore, when all the rooms become available, the company is expected to experience even higher room rate growth because the room rates in 1H2017 was temporarily suppressed by the partial closure and disruption in the hotel due to the renovation of the second phases of rooms.

New hotel construction projects are on track: The Peninsula London project is currently on track and the last office tenant moved out in April 2017. The hotel will have 189 rooms and 24-28 luxury residential apartments, which we expect the profit from the luxury apartments to cover the majority of the construction cost of the project, currently budgeting at around GBP600Mn. Demolition of the current site has begun and the expected completion date of The Peninsula London is FY2021.

For The Peninsula Istanbul, the company has started the demolition for the site. The Peninsula Istanbul will be a 180-room hotel by the waterfront and is part of the larger Galataport project consisting of museums, galleries, restaurants and parks. Moreover, the recent improvement in relationship between Russia and Turkey will attract more Russian tourists to travel to Istanbul, thus allowing The Peninsula Istanbul to expand its target customer group not only to Gulf nations but also to Russia. The expected completion date for the hotel is FY2019.

Investment property business continues to be stable: The Repulse Bay Complex remained to be the largest revenue contributor of the investment property business in 1H2017, contributing HK$310Mn or 66.5% of the total revenue of the investment property segment. The Peak Tower was the second largest revenue contributor and was fully leased throughout the reporting period. Additional revenue was received from Sky Terrace 428, which at the same time had a combination ticket arrangement with The Peak Tram. The company was granted a further 10-year operating rights for The Peak Tram subject to improvement project being satisfactory to the government. We view this as an encouraging opportunity as The Peak Tower, along with The Peak Tram and Sky Terrace 428, will provide synergy, thus generating stable recurring revenue to the company.

1-5 Grosvenor Place, the site for The Peninsula London, has been vacated in the reporting period. The revenue contributed by this investment property was HK$14Mn throughout the reporting period. Since demolition has started, the property will no longer be classified as investment property and will not provide any rental revenue. Therefore, we expect the revenue from the investment property segment to remain at current level.

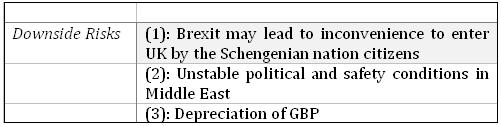

Investment Thesis, Valuation and Risk

Our valuation model suggests a target price of HK$12.50: Hongkong & Shanghai Hotels has several new hotel construction projects and they are on track. Further to that, The Peninsula Istanbul will be completed in FY2019 and will definitely be benefit from the recovery in the relationship between Russia and Turkey, thereby allowing the hotel to expand its customer group to Russian visitors apart from the Arabian visitors. Moreover, The Peninsula Beijing has almost completed its renovation and the RevPAR has been better than our original expectation. Therefore, we have altered our expectation on the financial performance and raised the target price to HK$12.50, corresponding to a P/E and P/B of 19.52x and 0.55x, with a `Neutral` rating assigned. (Closing price as at 10 Aug 2017)

Financials

Click Here for PDF format...