Investment Summary

Due to the integration of M&A business, the company's result in 2016 is below expectation, but that in 2017 is beyond expectation. Although the new business of M&A is still in the integration period, the company is expected to upgrade itself from supplier of individual components to system integrator of products integrating software and hardware, creating a distinctive service model of supply chain and becoming the leader in the segment industry. We reaffirm a target price of RMB 40.5 equivalent to 30 of 2017's estimated P/E ratio and 26 of 2018's, respectively, and assign BUY ratings. (Closing price as at 15 Aug 2017)

Integrating Cost to Achieve Higher Result than Last Year

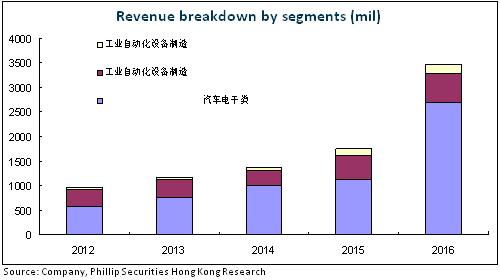

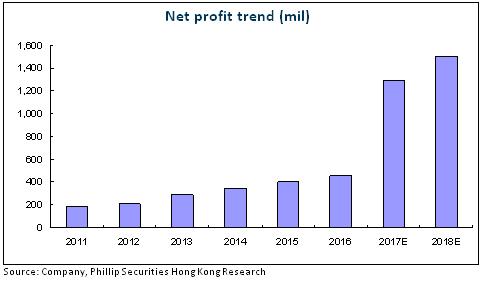

In 2016, the company recorded a revenue of RMB18.55 billion, representing a year-on-year growth of 129.5%. Original business revenue grew by 13%, while KSS and PCC created a consolidated income of RMB9.54 billion, accounting for half of the revenue. Net profits attributable to the parent company was RMB0.45 billion, only up 13.5% year-on-year. The EPS was RMB0.66, below our original estimate and market consensus, with the direct result that in the first five months of 2017, the company's share price was weak and plunged sharply, over ten percent less than the whole stock market.

The main reason is that during the reporting period, the acquisition of KSS and PCC (originally called TS) required a non-recurring expense of approximately RMB0.31 billion which includes interests from bank loans for acquisition and expenses of intermediary services and due diligence investigation, as well as the purchase price allocation (PPA) for KSS and PCC of nearly RMB62 million. In addition, KSS was affected by the devaluation of Mexican Peso, which reduced the profits and made the company unable to achieve the earnings forecast.

Integration Accumulated Strength to Ensure Substantial Growth in H1 2017 Results

At the beginning of 2017, the positive results of integration started to appear. In the first quarter of 2017, the company's revenue and net profits increased by 202% to RMB6.53 billion and 72% to RMB0.21 billion, respectively. In May, the company announced satisfying results. It is estimated that net profits attributable to the parent company will reach RMB0.61 billion to RMB0.68 billion, up 150% to 180% year-on-year. Following are the main reasons of the dramatic growth in results:

1) The investment income created by the share transfer of Preh Auto, estimated between RMB0.19 billion-RMB0.22 billion, was included in the revenue of the reporting period.

2) The consolidation of two subsidiaries, KSS and TS, promoted the sustainable and steady growth of the company's main business, which is estimated to create net profits attributable to the parent company from RMB0.42 billion to RMB0.46 billion, up 70% to 88% year-on-year.

Continuously Promoting Integration to Pursue Coordinated Development

The automobile consumption is becoming increasingly high-end. Thanks to the increasing rate of automobile electronization and the development of new energy vehicle market brought by the upgraded automobile consumption, automobile intelligence, safety, electronization and other fields, will continue to develop rapidly in the foreseeable five to ten years. The company will follow closely the development trend of automobile industry. Through asset acquisition and equity investment, we will improve the business layout of intelligent manufacturing, such as auto safety and automatic driving. Thus, the future result has the potential to rocket up. This year, the company will continue to promote the integration of KSS and PCC, control financial expenses and strive to achieve steady growth in result. The revenue in 2017 is expected to surpass USD4 billion and that in 2021 to reach USD10 billion. As for the cost control, the company will upgrade and integrate the supply chain and continue to promote global purchasing to reduce the cost of raw materials. What's more, it will continue to invest or expand production line in low-cost areas, such as China, Mexico and Macedonia, to reduce the cost of production. We believe that in terms of cost control, the company should have a larger space to dig.

Financials

Click Here for PDF format...