Summary of Investment

-The fourth batch of environmental protection supervision and examination has been started, and some very strict polices forced the demand for smoke-gas treatment to be rapidly released

-Long-term development room has been opened, by virtue of advanced treatment technology and accelerated arrangements of non-electric power sectors at home and abroad.

Increase of Operating Cost and Financial Expense Retarded the Profit Increase Rate

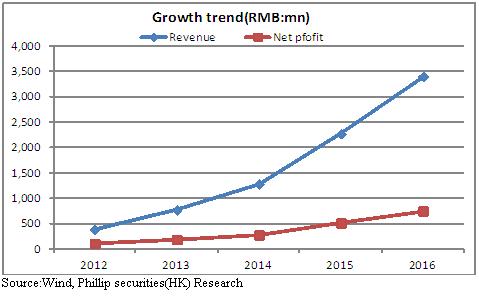

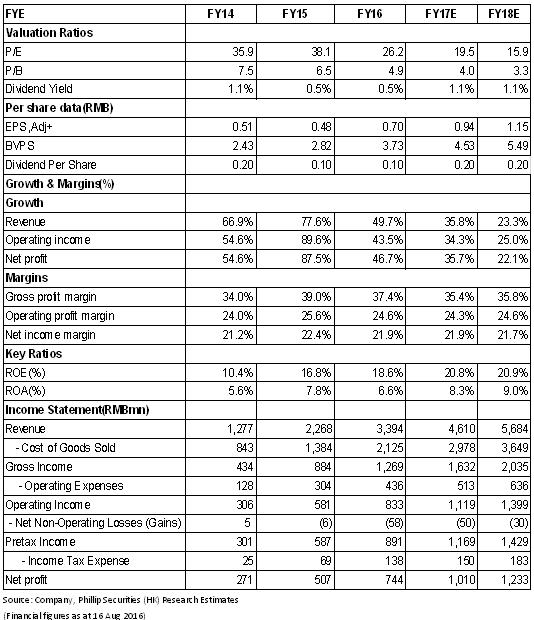

The prediction for the first half year of 2017 published by the Company indicates that the operating revenue increased by 42.63% year on year to RMB1.549 billion, but the net profit attributable to the parent company increased by 17.44% year on year to RMB0.315 billion. The profit increase was less than the revenue increase, because firstly, the cost had increased due to increase of construction business volume, and secondly, the newly added bank loan and green bonds had resulted in that the financial expense increased by 6.46 times year on year. According to the guidance in the Stock Option Incentive Plan of 2014, the net profit increase rates from 2015 to 2017 were no less than 85%, 170% and 270%, respectively (based on the net profit of 2014 RMB0.271 billion); the result growth objectives of 2015 and 2016 were achieved, and it is expected that the net profit of 2017 can exceed RMB1 billion, a year-on-year increase of 34.4%.

The Employee Stock Ownership Plan of Phase III Was Started

Recently, the Company issued the Employee Stock Ownership Plan of Phase III, in which the total number of participating staff didn`t exceed 1,000, accounting for 44% of the total number of the staff in the Company. It is proposed to finance a sum of fund up to RMB0.1 billion, with a lock-in period of 24 months. Besides, different from the previous two phases, the phase-III employee stock ownership plan doesn`t involve directors, supervisors and senior managers. The Company implemented two phases of employee stock ownership plans in 2014 and 2016, respectively. The purchase price of the employee stock ownership plan in 2014 was RMB14.2/share, and relevant shares had been totally sold in February 2017; that of the employee stock ownership plan in 2016 was RMB17.44/share, with a lock-in period of 12 months, and relevant shares had been sold in July 2016. Binding staff's interest with corporate interest can contribute to establishing a long effective incentive mechanism, stimulate staff's enthusiasm and release the Company's confidence in its long-term development.

Atmosphere Treatment Has Got Stricter, and Rigorous Environmental Protection Supervision and Examination Have Been Implemented

The fourth batch of central environmental protection supervision and examinations has been fully launched, and the atmosphere treatment in Beijing, Tianjin and Hebei listed as emphases in environmental protection supervision and examinations. According to relevant policies, the enterprises not able to complete upgrading, reconstruction and up-to-standard emission before the end of September will be thoroughly closed down, and it is expected that the strict policies concerning environmental protection supervision and examinations in the second half of the year will accelerate the progress of upgrading and reconstruction by industrial enterprises. The Company takes a leading position in the industrial smoke-gas treatment field, based on thermal power, rapidly expanding to non-electric power sectors, and expected rapid development, by benefiting from strict environmental protection policies and the growth of the demand for extra-low emission of non-electric power sectors. In addition, aiming at overseas markets, the Company has started its internationalization. It plans to establish a wholly-owned subsidiary in India with its owned capital RMB3 million to provide products and services to the customer resources in India and the surrounding markets. This is expected to accelerate the Company's overseas expansion progress, and promote its overall competitiveness.

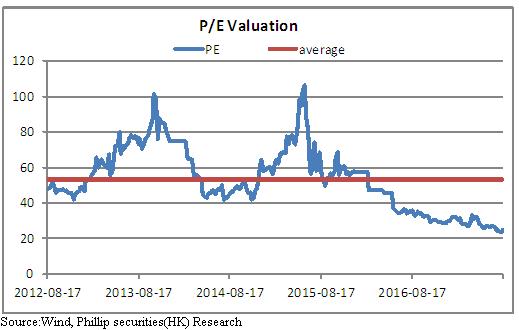

Valuation Rating

Based on the estimate, from 2017 to 2018, the Company's net profit attributable to the parent company will reach RMB1.01/1.23 billion, respectively, equivalent to an EPS of 0.94/1.15, respectively, and a PE of 19.5/15.9, respectively. We give a target price of RMB24.0 and the Buy rating. (Closing price as at 16 Aug 2017)

Risk Warnings

The non-electric power sectors are below expectations;

Environmental protection supervision and examination effect is below expectations;

Fierce competitions in market result in a risk of gross profit decrease;

Financials

Click Here for PDF format...