Summary of Investment

-- Sunshine Group buys shares at a premium price and holds more shares to embody confidence;

-- Air governance industry booms to catalyze the demands of governance;

-- New progress is made in the non-electrical sector.

Investment Advices

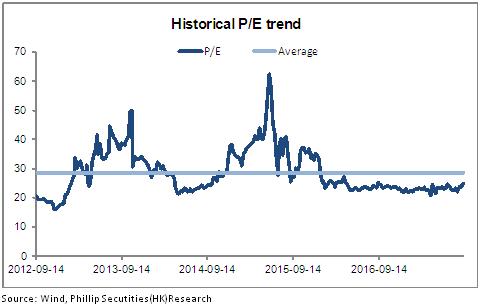

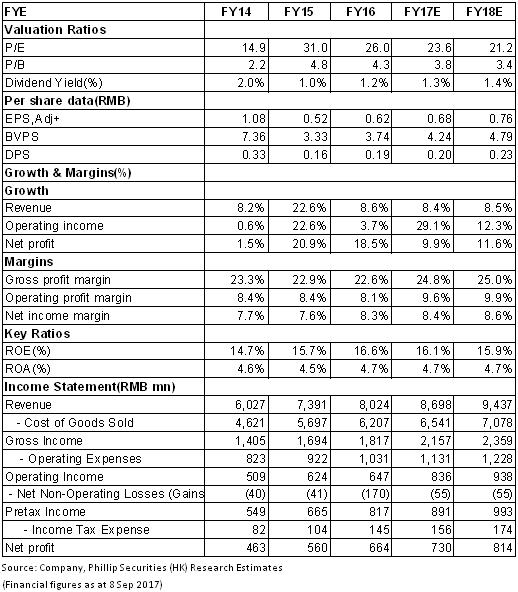

With the implementation of air governance plan and stricter environmental supervision, the air governance industry booms significantly, which continues to benefit our company as a leading enterprise. Based on the above-mentioned information, we forecast that the net profits in 2017 and 2018 are RMB730 million and RMB 814 million, respectively; the EPS, RMB0.68 and RMB0.76, respectively; equivalent to the P/E ratio23.6/21.2 in 2017 and 2018, we give a target price of RMB18.4 and the rating of "Accumulate".

Steady Growth of Interim Result

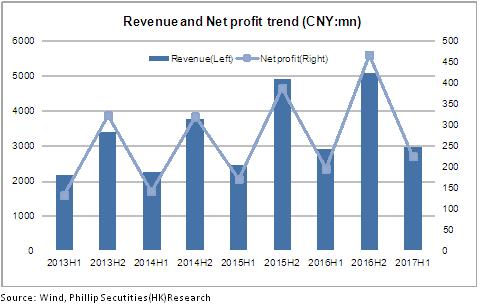

According to the result report in the first half of 2017, the revenue of Longking increased slightly by 1% yoy to RMB2,958 million, net profit attributable to the parent company increased by 14.66%yoy to RMB226 million, and net profit attributable to the parent company after the deduction of extraordinary items increased by 17.89% yoy to RMB205 million, equivalent to the EPS of RMB0.21, compared with RMB0.18in the same period of last year. In general, the result in the first half of the year grew steadily, and the second half will witness more growth of the company.

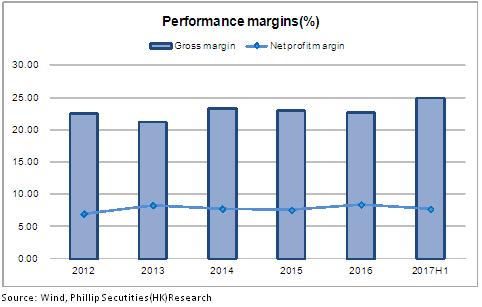

In respect of cost, the increase was 8.94%, slightly higher than the increase of revenue. The gross profit margin decreased slightly by 0.27%, which was mainly affected by the decline of that of real estate and overseas EPC project. During the period, the expense was RMB1.031 billion; the expense ratio was 12.85%, slightly up by 0.38 percentage point over last year. The net profit reached 8.37%, mainly affected by the one-off non-operating revenue of RMB137 million.

In terms of profitability, the gross margin increased by 1.5 ppts yoy from 23.4% in the same period of last year to 24.89%, and net profit margin increased by 1 ppts yoy from 6.72% in the same period of last year to 7.7%, which suggested that the profitability improved a little bit. The period cost rate rose by 0.7 ppts yoy to15.15%, among which the rate of administration expenses was 12.27%(+0.9%), mainly due to increased expenses for research and development(+26.2%); the rate of sales expenses was 2.52%(-0.09%) and the rate of financial costs was 0.36% (-0.1%). The operating net cash flow dropped dramatically from RMB-220million in the same period of last year to RMB-355million in that the costs for goods and services soared, which needs to be improved in the future.

Continuous Growth of Orders and New Breakthroughs in the Non-Electrical Sector

In the first half of the year, the amount of overall newly increased contracts reached RMB5.2 billion(tax included), equivalent to 51% of all the newly increased contracts in 2016. As at the end of the interim period, the amount of orders in hand was RMB17.8 billion, which guaranteed the subsequent growth of result. The electric bag team of the company actively expanded the "integrated device of desulphurization and dust removal" and "exhaust gas green island" projects centered on the electric bag, and made progress in the new business of green island with round tube belt conveyor as the main mechanism. This is expected to be a new point of growth. More contracts are concluded in dry desulfurization project which includes not only the traditional sectors, such as thermal power and steel, but also the emerging ones, such as coking, carbon, catalytic cracking, industrial exhaust gas governing and so on. Besides, significant breakthroughs have also been made in the business development of non-electrical sector including nonferrous metal, building materials, metallurgy and arcola. Moreover, it’s worth mentioning that the company is expanding its business overseas and has made breakthroughs in the Belt and Road Initiative and the projects in Southeast Asia.

Sunshine Group Holds More Shares to Show Confidence

When changes in share options are completed during the period, Eastright Investment & Development is still the largest shareholder. Sunshine Group holds indirectly 17.17% stock rights(183.5 million shares) of Longking by holding directly 51% stock rights of Eastright Investment&Development. The actual controller is changed from Zhou Suhua to Wu Jie who works in Sunshine Group. The final purchase price is RMB3.67 billion, equivalent to the price per share of RMB20, an increase of 23.3% compared with the current price. In addition, Sunshine Group plans to hold more shares valuing RMB0.5-1 billion in the next 12 months. So far, it has already increased 2.83% (30.284 million shares) through two trust schemes with total amount of RMB460 million. The shareholding ratio goes up by 20%, and will keep rising in the next 12 months.

Besides, the company launched 10periods of employee stock ownership plan, among which the 4th one has already finished up to now with an average purchase price of RMB14.68. Senior executives and key staff are involved in this plan. Associating the interest of employees with that of the company facilitates the long-term and sound development of the company.

Risk Warnings

The bids of new units and large units in power industry reduce.

The ultra-low emission transformation of power is coming to an end.

The market is becoming increasingly competitive.

The power sector has a financial strain, and it’s more difficult to collect payments.

Financials

Click Here for PDF format...