Investment Summary

- About 43.5% of the land in the land bank, in terms of GFA, is located in Guangzhou, Foshan and Hong Kong, the core cities of Guangdong-Hong Kong-Macau Greater Bay

- Declared first ever interim dividend of CNY0.10 per share

Business Overview

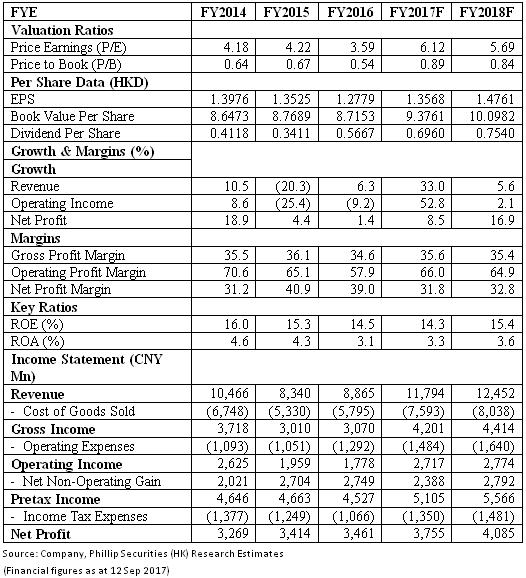

Promising 1H2017 result: In 1H2017, KWG Property achieved sizable growth. Revenue grew at a sharp rate of 44.2% to CNY7,856.6Mn. Partially caused by the drop in revaluation gain and the decrease in profit contributed by joint ventures, net profit rose only 9.5% to CNY1,556.7Mn. Excluding the revaluation gain and other one off items, core profit rose 17.3% to CNY1,440.0Mn. In terms of profit margins, KWG Property successfully maintain its profit margin at a high level, primarily caused by the increase in the selling price. Gross profit margin increased from 35.6% in 1H2016 to 36.0% in 1H2017. Contracted sales was strong during the reporting period and KWG Property achieved an attributable contracted sales of CNY14.62Bn, a YoY growth of 28.0%. The company declared its first ever interim dividend of CNY0.10 per share.

High quality land bank will assure the long term sales growth: KWG Property has projects in 18 cities and the projects are located in cities with good economic development. The land bank has a GFA of about 11.85Mn square metres. In particular, KWG Property has a strong strategic presence in the Guangdong-Hong Kong-Macau Greater Bay. In February 2017 and May 2017, KWG Property formed a joint venture with Logan Property and Longfor Property respectively and successfully broke into the Hong Kong market by obtaining land in Ap Lei Chau and Kai Tak development area. As at 30/6/2017, the company has a GFA of about 5,159,000 square metres of land located in the Greater Bay region, representing 43.5% of the GFA of the land bank.

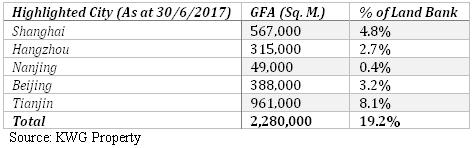

Apart from the Greater Bay, KWG Property also has strong presence in cities with strong economic development, such as Shanghai, Hangzhou, Nanjing, Beijing and Tianjin, which in total represent 19.2% of the GFA of the land bank. We expect KWG Property to benefit from the economic development in the Greater Bay and the cities with advanced economic development. We are particularly confident in the company's projects in the Greater Bay because the region is supported by the national development policy and the company has strong presence in the region.

Expand land bank replenishment sources to neighbouring cities: In 1H2017, KWG Property entered 6 cities for the first time, namely Wuhan, Xuzhou, Jiaxing, Taizhou, Jinan and Hong Kong. Some of these cities are located close to regions and cities with strong economic development and are well-connected to those cities and regions, thus allowing the cities to benefit in terms of economic development. In particular, the Ap Lei Chau project in Hong Kong is expected to be one of the most profitable project. Given the unobstructed view of the ocean, the site will be developed into villas and apartments specifically for middle to high end users.

Net gearing ratio dropped slightly: As at 30/6/2017, including restricted cash, the company had a huge cash reserve of CNY30.6Bn. Due to the huge cash reserve, the net gearing ratio dropped to 64.1%, which is healthy in comparison with the peers in the industry. The company achieved good sales throughout the reporting period and operates in regions with good economic development especially the Greater Bay region, which about 43.5% of the land, in terms of GFA, is located there. Therefore, we expect the amount of debt KWG Property currently bears being manageable.

Investment Thesis, Valuation & Risk

Our valuation model suggests a target price of HK$8.40: KWG Property announced the first ever interim dividend in FY2017. We are confident in the future projects of KWG Property especially it has a substantial portion of its land locating in the Greater Bay region. Moreover, KWG Property focuses primarily on cities with advanced economic development and will thus benefit from it. Therefore, a target price of HK$8.40, corresponding to a P/E and P/B of 6.12x and 0.89x, has been assigned, with a `Neutral` rating assigned. (Closing price as at 12 Sep 2017)

Financials

Click Here for PDF format...