Investment Summary

- 60% Decrease in 2017H Results

- Beijing Mercedes-Benz's doubled profits

- BAIC self-owned brand and Beijing Hyundai all turn gain to loss

Investment Thesis

Judging from the latest sales data, in July, sales volume of Beijing Hyundai and BAIC self-owned brand increased month on month, but we think it is difficult to see a strong rebound in the short term. The strong momentum of Beijing Mercedes-Benz has not diminished, with a sales increase of 48% year on year in July. In terms of new energy vehicles, BAIC self-owned brand, Beijing Hyundai and Beijing Mercedes-Benz have sufficient reserves of new energy models in the low, medium and high fields, aiming to meet the challenges of future new energy market competition.

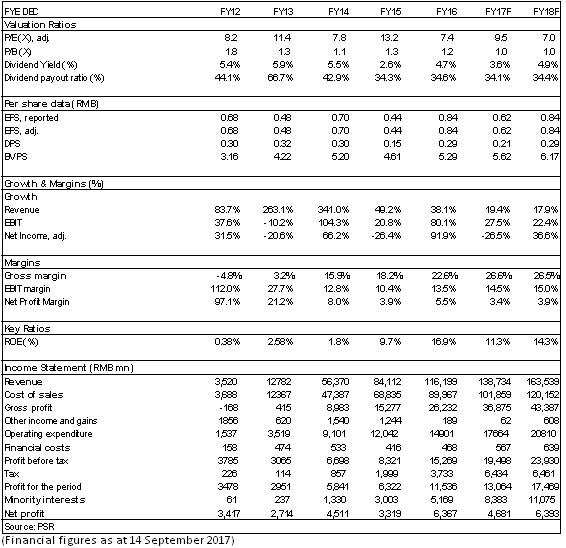

Semiannual report of the company showed that the result was greatly worse than expected, so we reduced the company's earnings forecast. Earnings per share in 2017/2018 will reach to 0.62/0.84 yuan. We will also reduce target price to 7.62 HKD (10.4/7.7x for 2017/2018 P/E) and rating to careful accumulate.

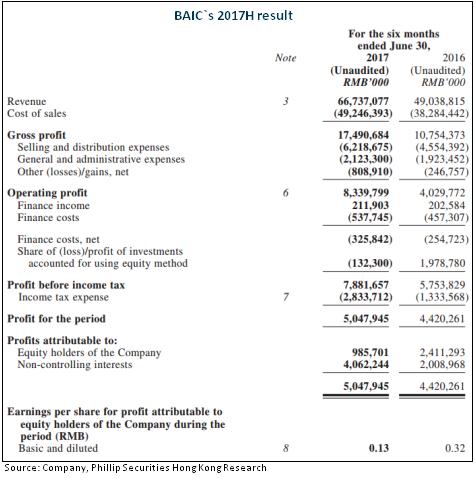

"One joy" failed to make up for "two worries", with the semi-annual result dropping markedly by 60%

Greatly influenced by its Korean cars sales volume, in the first half of 2017, BAIC net profit decreased dramatically by 59% to RMB986 million, compared to the same period last year. Earnings per share decreased from 0.32 yuan in the same period last year to 0.17 yuan in the first half of 2017.

During the period, the company's total revenue increased by 36% to 66.738 billion yuan year on year, owing to the 56% increase of Beijing Mercedes-Benz's revenue, which partially offset the 28% decrease of BAIC self-owned brand's revenue.

Beijing Mercedes-Benz's doubled profits

In the first half, Beijing Mercedes-Benz continued its explosive growth, with sales volume increasing by 47% to 211,000 units. Beijing Mercedes-Benz recorded an increase of revenue by 56% to 58.3 billion yuan year on year while its gross margin increased by 4% from 28% to 32%, with the contributed net profit from 2.05 billion yuan in the same period last year doubling to 4.24 billion yuan. Based on monthly sales exceeding 10,000 units in the Benz E level, C level and GLC level SUV, three flagship models, medium-term GLA level SUV also got a good sales result in market. In addition, the increase proportion of higher-priced SUV models and new models lead to positive correction in single vehicle revenue and profit: Price of single vehicle is 276,000 yuan, an increase of 6.5% year on year; profit of single vehicle is 39,000 yuan, a big increase of 41% year on year.

BAIC self-owned brand and Beijing Hyundai all turn gain to loss

However, the other two brands, BAIC self-owned brand and Beijing Hyundai suffered dismal results. Restricted by its weak product power, periodic shift and product mix, sales volume of BAIC self-owned brand in the first half deceased by 45.5% to 111,000 units. Revenue related to BAIC self-owned brand decreased by 29% to 8.4 billion yuan, with fractional gross margin decreasing from 2.3% to -15%. Finally it turned from a profit of 400 million yuan to a loss of 3.26 billion yuan in the same period last year.

Influenced by the market competition and political events between China and South Korea, Korean car sales volume continued its sustained downturn this year. In the first half, Beijing Hyundai sales volume decreased by 42.4% year on year, about 300,000 units. Investment income (mainly from Beijing Hyundai) first turned loss, a record low from a profit of 1.98 billion yuan to a loss of 120 million yuan in the same period last year.

Investment Thesis

Judging from the latest sales data, in July, sales volume of Beijing Hyundai and BAIC self-owned brand increased month on month, but we think it is difficult to see a strong rebound in the short term. The strong momentum of Beijing Mercedes-Benz has not diminished, with a sales increase of 48% year on year in July. In terms of new energy vehicles, BAIC self-owned brand, Beijing Hyundai and Beijing Mercedes-Benz have sufficient reserves of new energy models in the low, medium and high fields, aiming to meet the challenges of future new energy market competition.

Semiannual report of the company showed that the result was greatly worse than expected, so we reduce target price to 7.62 HKD (10.4/7.7x P/E) and rating to careful accumulate.

Financials

Click Here for PDF format...