Summary of Investment

-- Geo-replication of the Grandblue model again;

-- Extend business to the watershed management sector, and build new points of growth.

Investment Advices

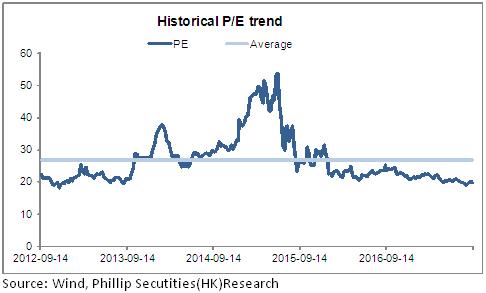

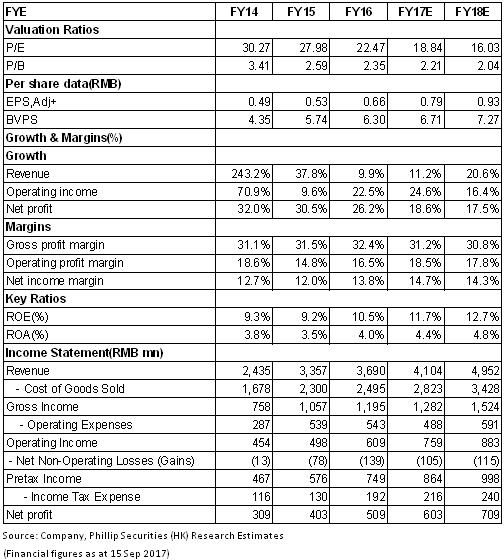

Business of water supply, sewage treatment and gas service has embraced steady operation and growth, contributing stable cash flow to the Company, as well as supporting the Company's expansion of solid waste treatment, with its focus mainly placed on market expansion schedule of solid waste treatment and hazardous waste treatment. Based on the above analysis, we predict the Company's net profits of 2017 and 2018 will reach RMB603 billion and RMB709 million, respectively; earnings per share (EPS) will be RMB 0.79 and RMB 0.93, respectively, equivalent to 18.4/15.6 times price-earning ratio (PER) of 2017/2018; the target price is adjusted to RMB17.4, with a “Accumulate“ rating. (Closing price as at 15 Sep 2017)

Steady Growth of the Four Major Types of Business

According to the 2017 interim result report, Grandblue Environment recorded revenues of RMB1.96 billion, with an annual increase of 13.8%, having accomplished 49% of the annual growth target; net profit attributable to the parent company was RMB314 million, with an annual increase of 20%; net profit attributable to parent company excluding non-recurring items was RMB287 million, with an annual increase of 15.4%, equivalent to primary earnings per share at RMB0.41, which was RMB0.34 over the same time period of last year. Among other things, solid waste, gas service, water supply and sewage treatment contributed 34.6%, 34.1%, 20.7%, and 4.59%, respectively to revenues, and revenue growth rate was 6.44%, 15.3%, 6.99%, and 15.38%, respectively. Generally speaking, the four types of major business have steadily developed and the overall result growth is satisfactory.

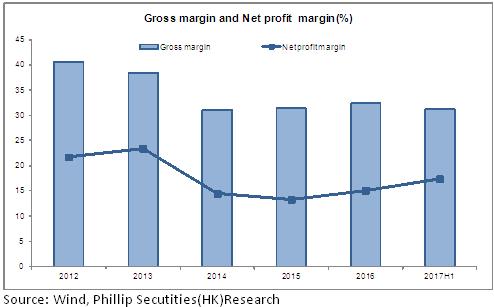

With regard to profitability, the overall gross profit margin was 31.12%, dropping by 2.9% Y-o-Y, mainly due to decrease of gross profit from gas service, water supply and solid waste treatment; net profit margin was 17.34%, up by 0.73% Y-o-Y; the period cost rate saw an obvious decrease to 11.77% from 14.49% over the same time period of last year, mainly benefiting from the sharp decline of financial expense by 20.3% post the issuing of corporate bonds.

Solid Waste Treatment Industrial Park is Geo-Replicated Again

The Company extended its business to the solid waste treatment sector in 2005, and established the first domestic solid waste treatment industrial park in Nanhai District. The Company acquired C&G China in 2014, achieving the nationwide layout for solid waste treatment. In September 2016, the Company bought 34% equity of Shunde Holdings and participated in the construction and operation of the solid waste treatment industrial park project in Shunde District (holding 70% equity of the operational company). The project consists of household waste (3,000 tons per day), sewage sludge treatment (700 tons per day) and kitchen waste project. This is the first geo-replicated solid waste treatment industrial park project of the Company.

In March 2017, the Company won the bid for the project: Solid Waste Integrated Treatment Center of Kaiping City in Guangdong Province, Stage 1, Phase 1, PPP Industrial Park. The project consists of the first household waste incineration power plant (Phase 1: 600 tons per day; Phase 2: 300 tons per day), percolate treatment center (200 cubic meters per day), landfill site (750,000 cubic meters) and relevant supporting projects. The Grandblue Mode is geo-replicated again, which suggests the Company's advantages in solid waste treatment have been recognized in the market, so as to further strengthen its impact and competitiveness in the field of constructing solid waste treatment industrial park in Guangdong Province and even in the whole country.

Intra-period Huangshi Phase 2 (400 tons per day) has been put into operation; Dalian Project (1,000 tons per day) is expected to be put into operation in the second half of 2017. So far, the volume of waste incineration power plant, sewage sludge treatment and kitchen waste treatment the Company is able to process is 26,750 tons per day, 1,350 tons per day and 1,350 tons per day, respectively; the capacity for hazardous waste treatment is 318,000 tons per year, among which proposed projects and projects to be built can process 10,050 tons per day. The projects to be built will contribute to results in 2018 and in later years. It's expected to record a result growth of 15% to 25% in the next three years.

Increase Capital to Blue Bay Company and March towards Watershed Management Sector

Business of water supply, sewage treatment and gas service of the Company are mainly centralized in Nanhai District of Foshan City, possessing a relative monopoly over Nanhai District. Water supply in Nanhai District has entered the mature period of the industrial development. There is still certain development space for sewage treatment and gas service with the development of city and boosting for environmental protection. Revenue of water supply as a result of increase of water consumption volume has reported a growth by 6.99% Y-o-Y (RMB406 million); revenue of sewage treatment due to contribution made by operation and management of the sewage collection pipe network has reported a growth by 15.4% Y-o-Y (RMB90 million); revenue of gas service facilitated by displacement of fuel gas and expansion of new customers in the aluminum profile industry has reported a growth by 15.3% Y-o-Y (RMB669 million), but its contribution to net profit has seen a sharp decline by 26.88% Y-o-Y; furthermore, the fuel gas project in Jiangxi Grandblue has a good start, the base filling station is under test run, some industrial users have been expanded, and the smooth implementation of fuel gas project outside the province helps to support the Company's sustained expansion in different areas.

In August 2017, the Company took the wholly-owned subsidiary, Grandblue Sewage Treatment Investment Company, as the main agency, increased RMB388 million to Blue Bay Company and acquired 90% equity of that company, in charge of watershed management project for the Lishui River in Nanhai District. The project investment scale is around RMB2.15 billion. The Company will march towards the watershed management sector by means of increasing capital, extending equity and investing in watershed management project of the Lishui River, which will facilitate the integration, optimization and coordination of the water service industry chain and create new points of profit growth for the Company.

Risk Warnings

Market competition is intensified;

Gross margin goes downward;

Expansion and bringing into operation of solid waste treatment is below expectation.

Financials

Click Here for PDF format...