Investment Summary

- Highly focus on the Pearl River Delta region, with 57%, of the GFA of the land bank contributed by the cities in the Guangdong-Hong Kong-Macau Greater Bay

- Urban renewal project will provide a significant amount of GFA of projects

Business Overview

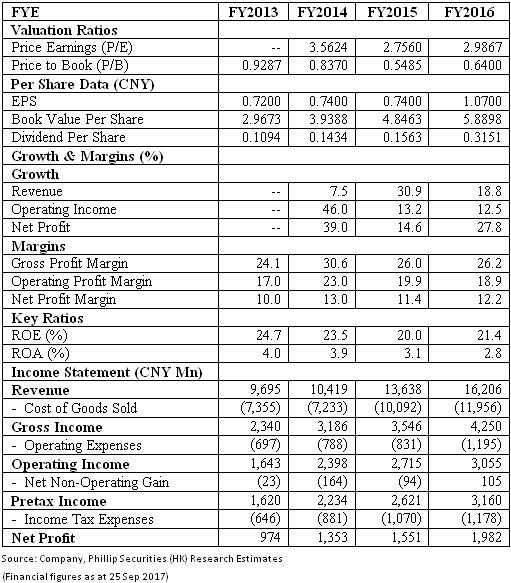

Rapid growth in 1H2017 result: In 1H2017, Times Property achieved sizable growth. Revenue rose 53.1% from CNY5,699Mn in 1H2016 to CNY8,725Mn in 1H2017. Gross profit rose 53.5% from CNY1,499Mn in 1H2016 to CNY2,301Mn in 1H2017. The rise in gross profit is mainly caused by the increase in revenue from the sales of properties and the slight increase in gross profit margin from 26.3% in 1H2016 to 26.4% in 1H2017. Core profit attributable to shareholders increased only 17.6% from CNY540Mn to CNY636Mn. Although net profit increased 51.3% to CNY799Mn, net profit attributable to the owners of the company decreased 9.4% to CNY498Mn. The sales of properties in 1H2017 has been strong, with the company achieving CNY17.03Bn contracted sales in the first six months, a YoY increase of 27.5%. The increase in contracted sales is solely contributed by the increase in sales price per square foot, as evident in the contracted sales area in 1H2017 being 1,165,000 square metres (1H2016: 1,198,000 square metres), a slight decrease of 2.75%. In 1H2017, the Basic and Diluted Earnings per Share were both CNY0.29.

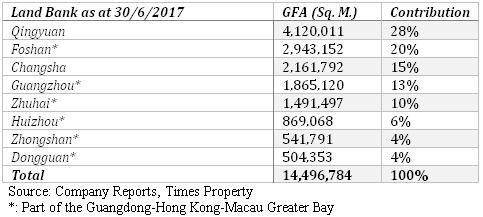

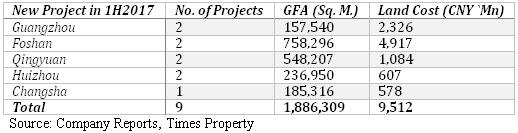

High quality land bank mainly located at the Greater Bay: Times Property primarily focuses on the property development in the Pearl River Delta region. As at 30/6/2017, Times Property has a land bank with a GFA of 14.5 million square metres, which is enough for development for the next 3-5 years. About 57% or 8,214,981 square metres of the GFA are located at Guangzhou, Foshan, Zuhai, Zhongshan, Dongguan and Huizhou. Therefore the national development policy `Guangdong-Hong Kong-Macau Greater Bay` will benefit Times Property significantly. The average land cost of the land bank is just CNY3,242 per square metres. Moreover, the company acquired 9 pieces of land in 1H2017, of which 6 pieces of land are located in Guangzhou, Foshan and Huizhou. These 9 pieces of land will provide an additional 1,886,309 square metres of GFA to the land bank.

Engages heavily in urban renewal projects: Instead of replenishing the land bank via public market, Times Property has a large proportion of projects being obtained through urban renewal way. As at 30/6/2017, Times Property had 48 urban renewal projects, primarily located at Guangzhou and Foshan, of which 17 of the projects, with a planned GFA of about 3.66 million square metres, have been acquired and are currently on application stage. The remaining 31 projects has a planned GFA of 10 million square metres and the company has signed the intent.

The Greater Bay national policy will benefit the company: The national policy of Guangdong-Hong Kong-Macau Greater Bay provides a repricing opportunity for the company. Transportation system and the infrastructure have been built in the area to connect the well-developed, core cities of the Greater Bay such as Hong Kong and Shenzhen to the less-developed Greater Bay cities or non-Greater Bay area such as Huizhou, Changsha and Qingyuan. This will enable the less developed regions to benefit via spill-over of housing demand caused by population growth and economic development, from the well-developed cities such as Hong Kong and Shenzhen. Times Property has a large land bank in the area with a low cost of CNY3,242 per square metres. The economic growth in the foreseeable future in the Greater Bay will allow the company to have a sustainable profit margins and a sizable growth in revenue, hence providing a repricing opportunity for the company.

Liquidity position improved but gearing ratio is still high: As at 30/6/2017, the gearing ratio was 68.6%, increasing from 54.7% in FY2016. The reason for the particularly low ratio in FY2016 is the recognition and the cash receipt stemming from the sales of properties, thereby lowering the gearing ratio. The company has a current ratio of 2.2x in 1H2017 (FY2016: 1.8x) and is mainly contributed by the increase in properties under development. Including restricted cash, the company has a cash reserve amounted to CNY13Bn in 1H2017 and this is enough to cover the current portion of bank loans.

We recommend investors to track Times Property: Times Property is one of the most undervalued China property development stock but has a high dividend yield of around 4.5%. In particular, it highly focuses on the development in the Pearl River Delta region, which the economic development of the region is supported by the national policy. The company has huge land reserve in Guangzhou, Foshan and Huizhou and potentially has more than 13 million square metres of GFA in the form of urban renewal projects. Therefore, we recommend investors to put Times Property in their watch list.

Financials

Click Here for PDF format...