- 2017H1 net profit down by 30% in due to the industry policies interfered

- The gross margin rose by 0.1 ppts, and the market share expanded against trend

- The NEV industry has gradually warmed up, with a high probability of explosive growth in 2017Q4

Investment Thesis

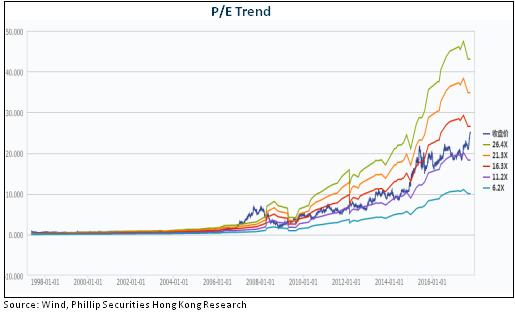

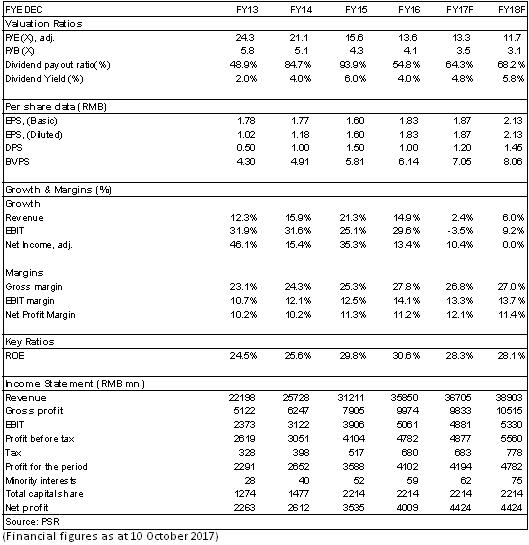

We forecast that the company's EPS in 2017/2018 will be RMB1.87 and RMB2.13. Considering the leading position and its continued technological advancement in new energy vehicles to drive down costs and broaden its market, our target price is set unchanged at RMB29. It is equivalent to a prospective 2017/2018 PE of 15.5x and 13.6x respectively. We give “Accumulate” rating. (Closing price as at 10 Oct 2017)

Quick-frozen industry interfered by policies and decrease in net profit of the company by 30% in H1

Yutong Bus recorded a total revenue of RMB9.31 billion in H1 2017, down by 30% YoY; the net profit attributable to the parent company stood at RMB810 million, down by 34.8% YoY. Basic EPS was RMB0.36, compared with RMB0.56 in the same period last year. EPS in Q1 and Q2 were RMB0.14 and RMB0.22, respectively.

Influenced by multiple adjustments of subsidies for new energy passenger vehicles, including investigations on subsidy defrauding, state subsidy fall-off and local subsidy lagging behind, China's new energy passenger vehicles industry has been quick-frozen in the first half of the year. Sales of new energy passenger vehicles have basically stagnated. The main growth engine of Yutong Bus has been sharply stalled in recent years, with semi-annual cumulative sales down by 28% YoY to 2.18 million units. According to the Ministry of Industry and Information Technology, the number of new energy passenger vehicles produced by Yutong Bus in H1 was down by nearly 60% YoY.

The gross margin rose by 0.1 ppts, and the market share expanded against trend

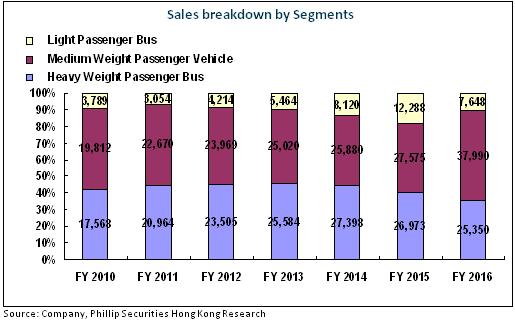

The sales volumes of large, medium and light passenger vehicles of Yutong Bus fell by 7.5%, 40% and 15% YoY to 8,751, 9,947, and 3,136 units, respectively. Due to the increase in the proportion of large passenger vehicles, the gross margin of the Company was 24.9% in the first half of the year, up by 0.1 ppts YoY, while the gross margins in 1Q and 2Q were 24% and 25.6%, respectively. The Company's export sector has performed well, with the volume of exported passenger vehicles up by 17% YoY to 4,356 units.

The adjustment of state subsidies for new energy passenger vehicles has raised the industry threshold, and accelerated the industry clearing. The market concentration of the industry leaders such as Yutong Bus has been significantly improved. The Company's share of vehicle models in the range of 10 meters above, 8 to 10 meters and 6 to 8 meters reached 18.5%, 40% and 12%, respectively. The market share is up by 1.7, 9.3 and 9.5 ppts, respectively, from Year 2016.

The period cost rate rose by 2.1 ppts, mainly due to the rigidity of administration expenses and the delayed grant of state subsidies. During the reporting period, the Company spent RMB505 million on R&D, up by 11% YoY, mainly for such cutting-edge technology as development and optimization of high-end models, new energy buses, lightweight technology and intelligent driving and fuel cells.

The new energy passenger vehicle industry has gradually warmed up, with a high probability of explosive growth in the fourth quarter

With the end of the policy vacuum, the new energy passenger vehicle industry has gradually warmed up. The sales volume of Yutong Bus started to soar from June. In the new edition of the subsidy catalogue, Yutong Bus has obtained subsidy eligibility for 91 new energy passenger vehicles and 3 new energy special vehicles. The bidding for new energy vehicles for all the public transport companies is being fully restarted. We anticipate Yutong Bus will usher in a period of explosive growth of new energy vehicle orders in the fourth quarter.

Financials

Click Here for PDF format...