Investment Summary

- Greater coverage of delivery service and extending store network.

- Enriched product mix and exciting staff incentive plan.

- Recovery of catering business with regional development.

Company Background

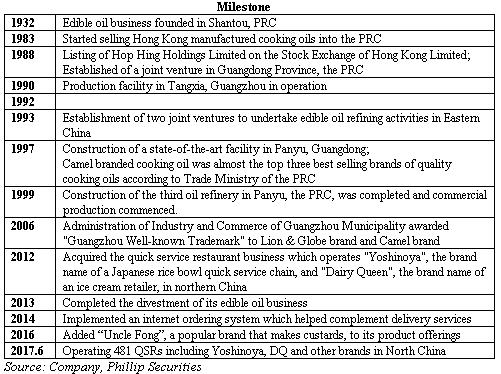

Company ProfileHop Hing Group Holdings Limited (“HHG” or “the Company”) is principally engaged in quick service restaurants (QSR) business in North China. HHG gained rights to operate fast food restaurant chains in franchise regions by issuing convertible bond in 2011. With the acquisition of QSR business, namely the rice bowl brand “Yoshinoya” and ice cream brand “Dairy Queen(DQ)”, HHG successfully transformed itself from solely specializing in edible oil business to QSR-focused business.

Currently the company operates 481 quick service restaurants as up to 30 Jun 2017, covering seven northern Chinese provinces, including Beijing, Tianjin, Hebei, Liaoning, Jilin, Heilongjiang and Inner Mongolia. In future, HHG will continue to expand sales network, diversify brand portfolio and provide various food choices to customers.

Business Analysis

Overview

As up to Jun 30 2017, HHG operates 481 fast food chains with brands including Yoshinoya, DQ, etc. Business in Jing-Jin-Ji area contributes majority of HHG's revenue. In 1H17, 75% of the revenue came from Jing-Jin-Ji area, while other four cities (namely Liaoning, Jilin, Heilongjiang, Inner Mongolia) contributed 25% to the topline. In terms of brands, during the first half Yoshinoya recorded sales of RMB 1,572mn accounting for 85% of total sales while DQ delivered sales of RMB172mn making up 11% of revenue. Meanwhile, six distribution centers in Beijing, Dalian, Shenyang, Harbin, Tianjin and HuHeHaoTe, were primarily established to store, process and repackage food to be distributed to the franchise stores.

Yoshinoya: Leading Japanese fast food chain in Northern China.

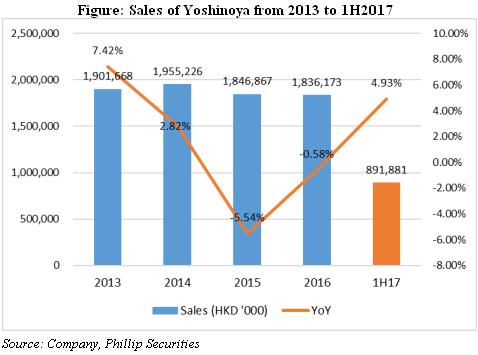

Yoshinoya is a century-old Japanese food chain brand, offering a variety of meals, principally the rice bowl. It is famous for the specialty Gyudon (beef bowls) and also provides a series of taste choices, such as chicken bowls, pork bowls, etc. Yoshinoya targets younger generation who are relatively price-sensitive and the average spending of customer is around RMB30. HHG now operates 317 Yoshinoya shops in PRC. However, dragged by sluggish economy environment, sales of Yoshinoya decreased from 2012 to 2016 showing negative growth.

Three factors contribute to revenue recovery. In 1H17, the brand achieved HD$891mn sales with 4.93% YoY growth, arising from the development of delivery service, expansion of stores network and enriched product portfolio. 1) Enhancement of delivery service: increasing delivery sales now contribute about 30% to sales of Yoshinoya. HHG continues to enhance the self-operated delivery platforms and cooperate with popular online catering platforms to increase brand exposure and enhance customer outreach. In Beijing, HHG's biggest market, the own delivery team of 1000 staff covers over 200 stores and assures stable delivery services and product quality. 2) Store network expansion: the company adopts a 3-tier system, which means opening flagship stores and regular stores progressively particularly in the capital city and opening smaller stores to cater for takeaway orders. Building smaller size of stores helps improve store efficiency, since it can not only increase delivery coverage, but also lower labor cost and rental expense. Aged stores are also renovated to provide customers with a cozy environment. 3) Enriched product portfolio: new products e.g. hot pots, special drinks, French toast for breakfast, are continuously added into product mix to enrich clients` choice and satisfy more younger generations.

Dairy Queen: Improving Store Network and Better Dining Experience.

Dairy Queen provides a range of ice-cream cakes, frozen treats, beverages and fast food. It caters to the customers who have higher consumption power and are looking for better dining experience. HHG focus on opening DQ stores in mega malls with good traffic to adapt to the changing consumption pattern in China. From 2012 to 2016, DQ revenue slightly declined but recovered in 1H17.

HHG kept improving DQ network quality by closing underperformed stores and opening new profitable stores. DQ started to provide delivery services for selected products since the end of 2016. With extensive coverage and increasing brand exposure through third-party's delivery platforms and self-owned social media platforms, we see delivery sales grew rapidly. Meanwhile the company continues to introduce innovative new products to stimulate the taste buds and add new elements to attract young generations. Also in future the company is going to open more DQ flagship stores with comfortable seats to enhance dining experience.

Multi-Brand Strategy and Enhanced Product Mix

The company places importance on introduction of new brands. It introduces a new brand “Uncle Fong” in 2016, which offers authentic Hong Kong snacks to consumers in Northern China. The brand focus on small stores with lower investment costs and faster payback period. Meanwhile, HHG continues to introduce new products according to customer segmentation and improve customers` loyalty. Leveraging on the big data derived from the internet platforms, HHG launched new drinks products which promised high profit margins. With technology applied in business operation, HHG expects to better track the ever-changing market needs and consumption trends to provide more comprehensive products to its customers.

Staff Incentive Scheme Improves Operating Efficiency

The company maintains competitive compensation packages and provides trainings to retain talents. The Virtual Partnership Scheme has been implemented in all stores since 2Q 2015, allowing the heads of stores to operate their establishments as if they were the store owners. The scheme gives managers a sense of ownership and motivates them to operate stores in more efficient ways. The program allows managers to share the fruits of the company success, through rewarding them the certain portion of revenue as long as it outperforms the sales target. Managers` cost-saving efforts have contributed directly to profit growth especially in adverse market conditions, given that the other operation expenses gradually decreased these years.

Investment Thesis, Valuation & Risk

We initiate target price of HK$ X and “Accumulate” investment rating. We see the great potential of the Integration in Jing-Jin-Ji Area policy which is going to boost regional economy in Northern China. As one of the leading catering business in Northern China, HHG is likely to achieve better performance, given expanding network, improving management efficiency and rising regional consumption. We initiate with “Accumulate” rating for the company, and set target prize at HK$0.24 with 11% upside.

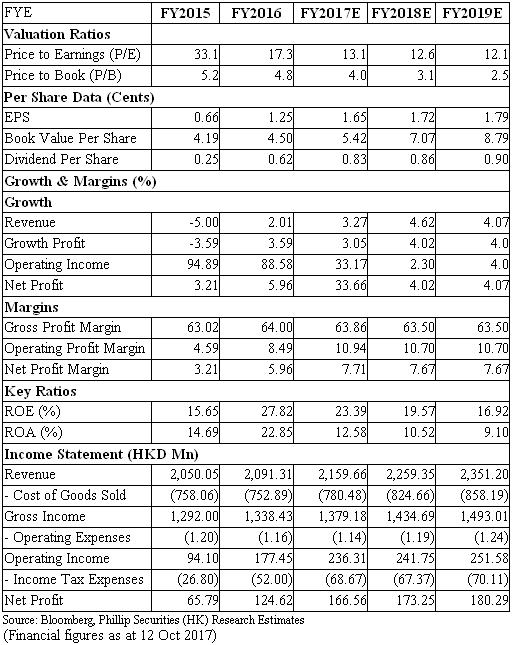

Financials

Click Here for PDF format...