Summary of Investment

-Rapid growth in the scale of new sewage treatment;

-Multiple new PPP projects in the second half of the year, increasing reserves of projects;

-A valuation much lower than fellow companies, an adequate margin of safety;

Investment Advice

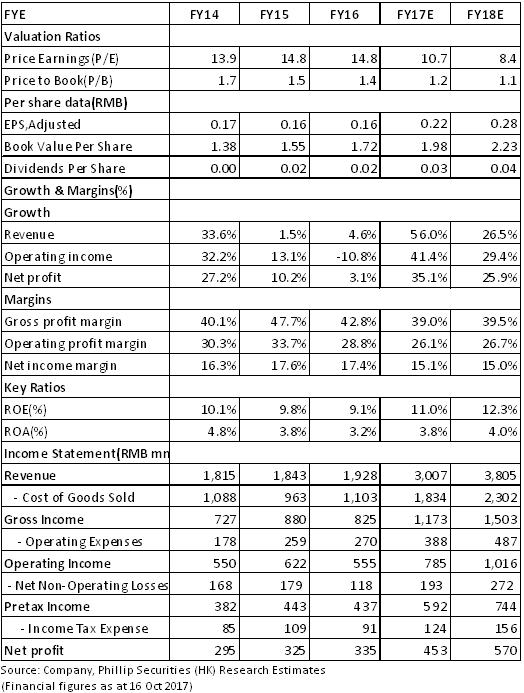

The share price of the company has been fully adjusted in the first half of the year. With the rapid growth of construction income in the second half of the year, it is expected to achieve the 30% growth in result for the whole year. The share price has the possibility of growth. We predict the net profit attributable to parent company from 2017 to 2018 to be RMB 453/570million. The rating of "buy" is given. The target price is HKD2.87. (Closing price as at 16 Oct 2017)

Solid growth of result in the first half of the year: In the first half of 2017, Kangda International Environmental Company Limited has reported a revenue of RMB10.68 billion, a year-on year increase of 18.33%, including the construction income of RMB550 million (+26.9%) (RMB409 million construction income of development of water affairs in urban area, RMB108 million construction income water environment treatment, RMB34 million construction income of rural sewage treatment), the operating income of RMB298 million (+13.3%), the financial income of RMB220 million (+7%). Besides, the net profit attributable to shareholders of parent company amounted to RMB177 million, representing a year-on-year increase of 56.6%, and the basic EPS stood at RMB0.0854 (+56.4%). Profit growth substantially exceeded revenue growth, mainly due to the acquisition of the 15% of the assets of Zhongyuan Asset with a profit of RMB0.37 billion.

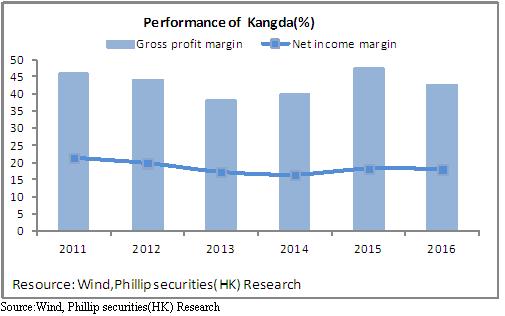

The intensive market competition has a negative impact on the gross profit margin: With regard to profitability, the gross profit margin decreased by 2% to 40% over last year, which mainly resulted from the decrease of gross profit margin of construction income with a high proportion in total income and the decrease of the proportion of financial income. During the year, the period cost rate was on the high side compared to fellow companies, rising by 1% to 27.82% over last year. The net profit margin was 17.16%, a year-on-year increase of 3.6%.

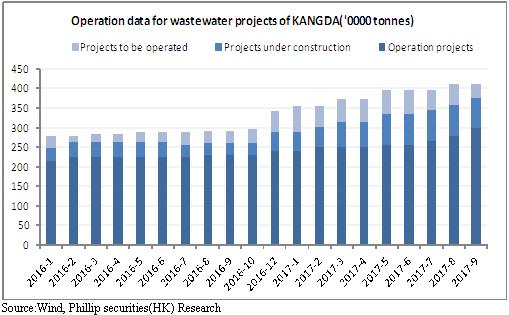

The scale of sewage treatment has increased dramatically: With regard to the treatment of urban sewage treatment, the company endeavored to expand its processing scale through market exploitation and merger and acquisition. In the year, the company has successively acquired about 1.09% share rights of Prodaksen (Asia) Water Service CO., Ltd. and 100% share rights of Hatlen Investment (Aus.) Pty Ltd., 100% share rights of Shandong Fengmin Water Service CO., Ltd. and 70% share rights of Wenzhou Chuangyuan Water Service CO., Ltd. As of September 30, the company has contracted for sewage projects with the daily processing scale of 4.109 million tons per day, a year-on-year increase of 40.8%, operation projects with the daily processing scale of2.984 million tons, a year-on-year increase of 29.2%, projects under construction with the daily processing scale of775 thousand tons, a year-on-year increase of 167.2%, and projects to be operated with the daily processing scale of 350 thousand tons (+9.4%). The rapid growth of the expected new processing scale will provide a guarantee for the continued growth of the income of urban water operations and construction.

The company expedited the progress of project acquisition, the reserve of projects will increase: In 2017, especially in the second half of the year, the company has contracted for multiple PPP projects including the PPP project of the construction of integrated pipe corridor in Weihai Nanhai Area, Shandong, the construction of sewage treatment bound with PPP projects in Jiaoling County, Meizhou City, Guangdong, the first phase of PPP project of Fuhe river construction in Fuzhou City, Jiangxi, and the first and second phase of sanitary sewage treatment PPP project in Maan Town, Huizhou, Guangdong. The total investment is nearly RMB5 billion. With the intensive construction of new PPP projects in the second half of the year, the construction income in the second half of the year is expected to exceed that of the first half of the year, and the annual construction income is expected to achieve considerable growth.

Risk Warnings

The number of new contracts is less than expected;

PPP construction is slower than expected;

Financials

Click Here for PDF format...