- High-speed boom of heavy truck market drives the high growth of the result in H1

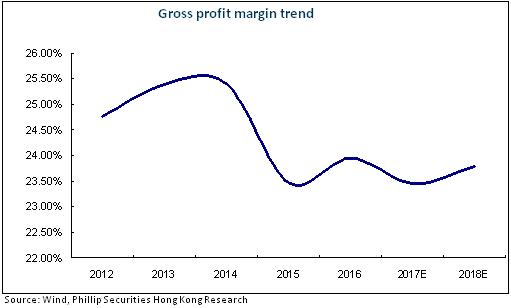

- The gross margin increased by 1.2 ppts

- Steady financial structure, sufficient cash guarantee

- The high-growth momentum of result will continue in H2

Investment Thesis

Valuation

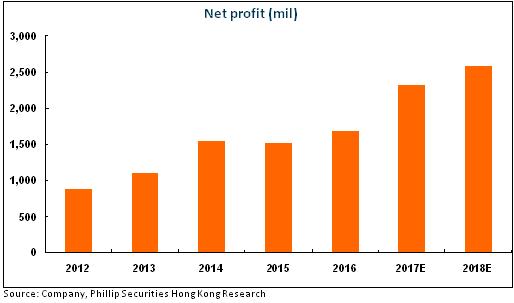

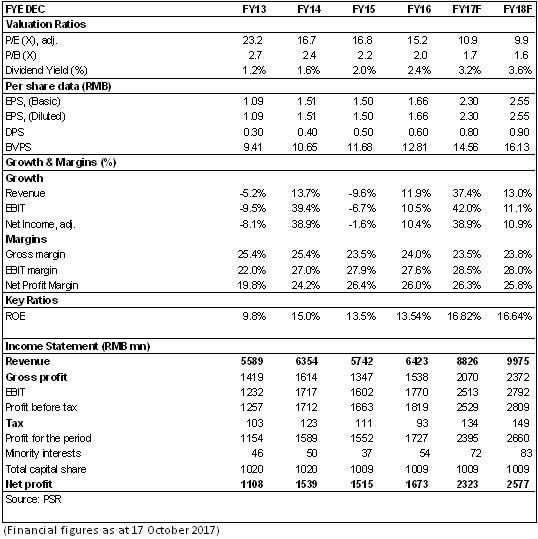

As analyzed above, we expected diluted EPS of the Company to RMB 2.3 and 2.55 for 2017/2018. And we accordingly gave the target price to 30.58, respectively 13.3/12x P/E for 2017/2018. "Buy" rating. (Closing price as at 17 Oct 2017)

High-speed boom of heavy truck market drives the high growth of the result in H1

Weifu High-Technology recorded a total revenue of RMB4,728 million in H1 2017, dramatically up by 40.45% yoy; the net profit attributable to the parent company was RMB1,326 million, up by 40.52% yoy; the net profit attributable to the parent company after deduction of non-recurring profit or loss was RMB1,208 million, up by 45.64% yoy; the net profit in H1was equivalent to 80% of that of last year. Earnings per share were RMB1.31. The figure was RMB0.94 in the same period of last year.

The Company's products like automobile fuel injection, post-processing system and engine air intake system are mainly used in and are highly related to the heavy truck market. Benefiting from the recovery of domestic infrastructure construction market and the strict implementation of the treatment policies against overloaded and out-of-limit heavy trucks, the sales volume of domestic heavy trucks has been on the increase since the middle of last year; its average monthly sales volume exceeds 50%; in H1 2017, a total of 583.7 thousand heavy trucks were sold out at home, up by 71.85% yoy.

The gross margin increased by 1.2 ppts, and the expense was under proper control

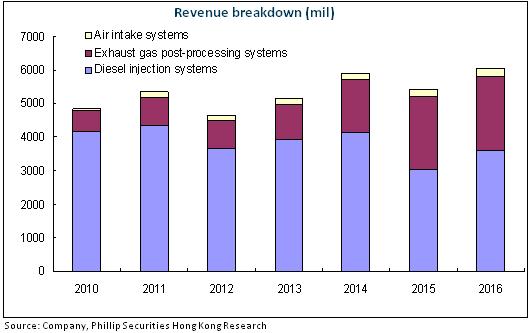

By category, the Company's core product, automobile fuel injection system, recorded a revenue of RMB2,913 million, up by 54% yoy; its automobile post-treatment business recorded a revenue of RMB1,384 million, up by 19.42% yoy; its engine air intake system recorded a revenue of RMB0.18 billion, up by about 38.5% yoy.

The gross margin of the Company was increased by 1.2 ppts to 26.1%. Wherein, the gross margins of automobile fuel injection system and engine air intake system increased by 1.2 and 2.5 ppts, respectively, and that of automobile post-treatment business decreased by 6.2 ppts due to the price rise of bulky materials, e.g., steel. Meanwhile, the Company's expense was under proper control, and the three expense ratios decreased by 2 ppts yoy.

The major affiliated companies Bosch Automotive Diesel Systems Co., Ltd. and United Automotive Electronic Systems Co., Ltd. recorded an income from investment of RMB834 million in H1, up by 40% yoy accounting for 57% of the Company's pre-tax profit.

Steady financial structure, sufficient cash guarantee

The Company's financial state kept steady continually, the asset liability ratio was only about 25%, the quick ratio was 2.6, and the cash flow was continually enhanced. At the end of H1, the on-hand cash + net bills receivable reached RMB3.1 billion, an increase of RMB 0.83 billion yoy, guaranteeing the extended development of the Company and the dividends paid to shareholders. We hope that the industrial buyout fund established by the Company in the middle of last year can yield positive results early.

The high-growth momentum of result will continue in H2

On July 1, 2017, the National V Emission Standard was formally implemented for domestic heavy trucks around the country. On January 1, 2018, it will be implemented for light trucks as well. In addition, the National VI Emission Standard formally entered its preparation stage (predicted to be implemented in 2020); the post-treatment system of commercial vehicle will enter a period of favorable policies. It is expected that both the quality and price of products of the Company will increase.

Financials

Click Here for PDF format...