Investment Summary

The strong performance of concentrated TCM granules business confirmed our positive view before. As more medicine dispensing machine are equipped in hospitals, the company further consolidates the market position and prepares for future competition in hospital terminal. With acquisition of upstream and downstream businesses, we see progressively integrated value chain. We expect the bright prospect of concentrated TCM granules and maintain BUY with our target price of HKD5.70. (Closing price as at 19 Oct 2017)

Business Overview

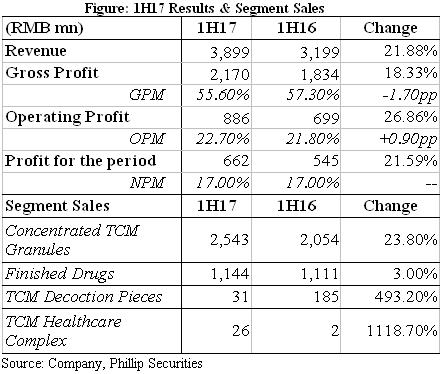

Strong growth in 1H17 results. The company reported turnover/net profit of RMB38.99bn/662mn in 1H17, representing nearly 22%/21.6% YoY growth. We notice that concentrated TCM granules accounting for 65% of topline grew rapidly with 23.8% YoY growth, while finished drugs achieved modest growth (+3% YoY)in first half. Gross profit margin declined by 1.7ppt, which is attributable to the price hike of raw materials and lower profit margins of new businesses (TCM decoction pieces and TCM healthcare complex). We see that the ample inventory stock helped to mitigate the decreasing trend of GPM, although the inventory turnover days for TCM granules significantly rose (+110 days). The finance cost recorded 149.4% YoY growth (RMB85mn) due to RMB4.5bn panda bond issued in November 2016 and June 2017.

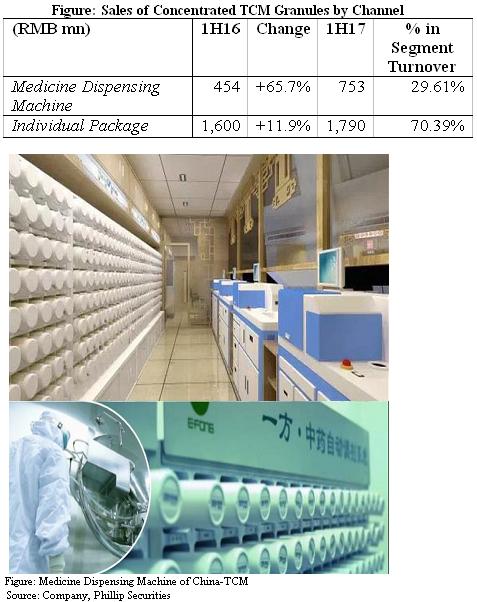

Medicine dispensing machine facilitates market expansion. Concentrated TCM granules are distributed by two main channels, namely individual package and medicine dispensing machine. Although individual package still consisted 70% of concentrated TCM granules turnover, the revenue through medicine dispensing machine dramatically increased by 65.7% YoY in 1H17. We know from our checks that the company provides machines freely to big hospitals. Because the machines are specially designed for the company's TCM granules, it forms a natural entry barrier for other competitors and charges a high switching cost to the hospitals. As up to 30 June, 3072 machines have been installed in 1740 hospitals. We expect future sales growth of TCM granules arising from the progressive installation of medicine dispensing machines.

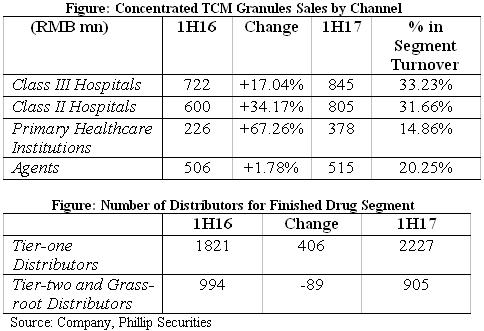

Enhanced channel mix of main segments. One market concern is that the implementation of two-invoice system will adversely impact the agent sales. We notice that the company continued to improve the distribution channels of two main segments. For concentrated TCM granules, the revenue from primary healthcare institutions and class II hospitals dramatically increased in 1H17. And the company compressed the portion of sales to agents to 20.2% (24.6% in 1H16) thus further upgrades the quality of distribution channel. As for finished drugs, we see the number of tier-one distributors rose with less tier-two and grass-root distributors. In long run, we believe that the more flattened distribution structure will help the company to strengthen its control over end customers.

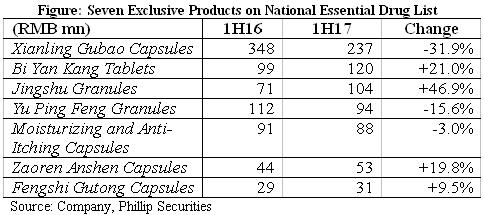

Recovering sales of finished drugs with anticipated new drivers. The finished drug business reported RMB1.14bn sales (+3% YoY) and higher OPM (18.9% in 1H16, 21.6% in 1H17). The sales of one main product, Xianling Gubao Capsules, reported 32% YoY decline due to limiting delivery, as the company was required to replacing the packaging of OTC logo. In future the company is going to nurture the market of some important products through upgrading package and covering more pharm chains. Upgraded package of OTC products may help to build better brand image and strengthen competitiveness. Also the price of newly packaged products will be higher than old ones. We still concern that the side effects from zero mark-up policy and secondary price negotiation are obvious. Although it is hard to achieve high growth in future, modest increase of finished drug business can still be expected.

Attractive integrated value chain with fast growing businesses. We see that an integrated TCM value chain is established and continues to expand. In 2016 the company completed the acquisition of Guizhou Tongjitang and Shanghai Tongjitang, which mainly focus on TCM decoction pieces. This contributes to extension of up-stream business and ensure better control over raw materials for TCM granules production. Although TCM decoction pieces only consisted 5% of topline in 1H17, this segment grows very rapidly. Meanwhile, the company continues to upgrade construction line and build new capacity in provinces such as Zhejiang, Shandong, etc. The company plans to increase its existing capacity of Chinese medicinal herb extraction and concentrated TCM granules, which is expected to realize over RMB20bn production value after accomplishment. In downstream, the company completed the acquisition of 60% registered capital in Guizhou Tongjitang Pharmacy Chain, thus further expands the sales network. With enhanced control over hospital customers and pharm chains, we expect the company to achieve better performance in future.

Investment Thesis, Valuation & Risk

Our valuation model suggests a target price of HK$5.7: Given China-TCM continuing to enhance the control of upstream, expanding capacity and strengthening sales network, we maintain BUY recommendation with our target price HKD5.7 representing 29% upside.

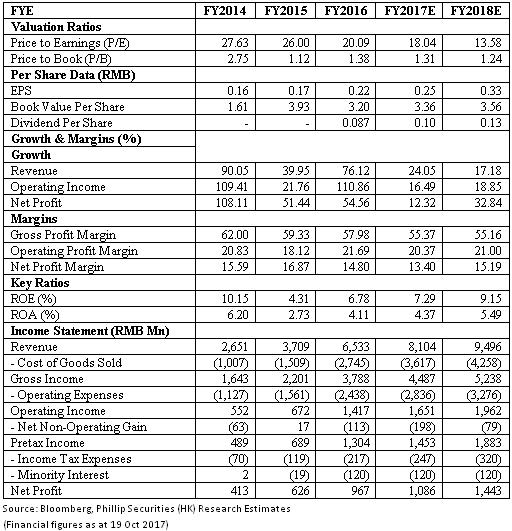

Financials

Click Here for PDF format...