Summary of Investment

- The industry of industrial smoke treatment remains booming;

- With a firm commitment to the layout of non-electrical sector, there is expected to be an outperforming growth;

Investment Rating

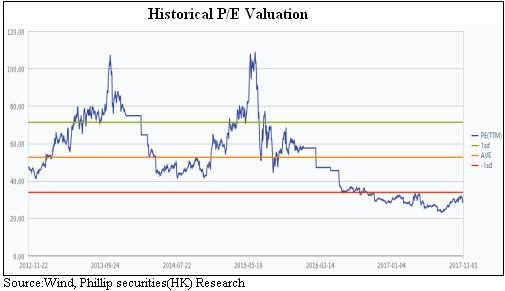

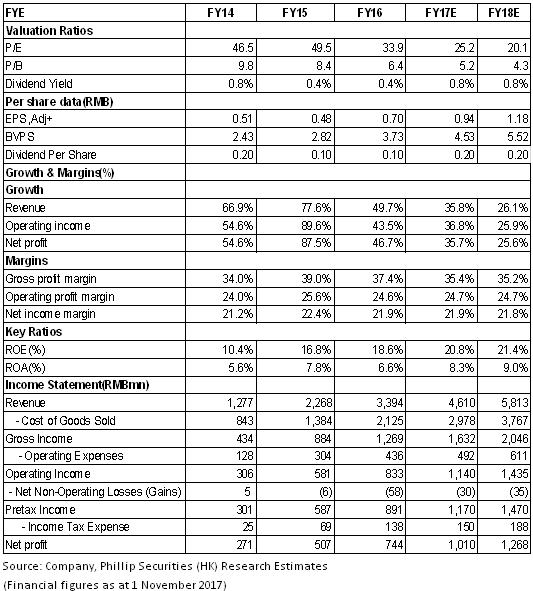

We believe that with an enormous boom in the industry of industrial smoke treatment, the leading companies will benefit continuously from it and we see a bright future in the company's early layout and active merger and acquisition in non-electrical sector which is expected to provide new growth impetus. We expect the 2017 to 2018 net profit attributable to the company to be 1010/1268mn, respectively, and EPS to be 0.94 and1.18, respectively, equivalent to PE of 25.2and 20.1, respectively. The target price is 30.00 RMB and the Buy rating is given. (Closing price as at 1 NOV 2017)

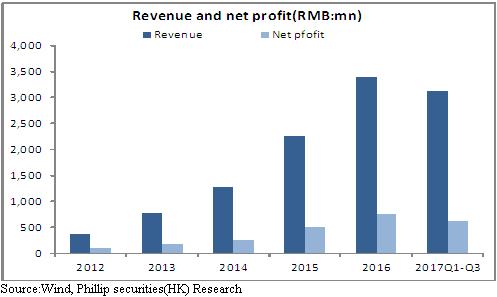

Results in the First Three Quarters Meet Expectation. According to 2017 Q3 result report, SPC Environment recorded a revenue of RMB3.134 billion, up by 57.65% yoy, a net profit attributable to parent company of RMB618 million, up by 23.99% yoy and 24.27% yoy after deduction of non-recurring profit and loss and the corresponding EPS of RMB0.575 (+23.11%). The results meet our expectation. Q1, Q2 and Q3 reported revenues of RMB672 million, RMB877 million and RMB1.584 billion, respectively and net profits after deduction of non-recurring profit and loss of RMB91 million, RMB316 million and RMB295 million, respectively. The trend of contribution quarter after quarter is positive. The company anticipates the yearly net profit margin to be between RMB856 million and RMB1.07 billion, up by 15%-45% yoy, mainly due to the new result growth from new operational businesses and the EPC program in progress.

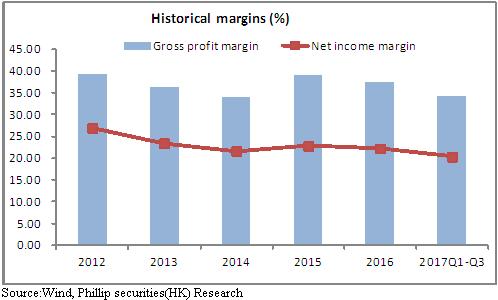

The Decrease in Gross Margin and Large Increase in Financial Expense Retarded the Net Profit Margin. In terms of financial profitability, the company recorded a gross margin of 34.2%, down by 4.2% compared with 38.4% in the same period of last year, mainly due to the increase in raw material cost; and a period cost rate of 12.3%, up by 3%, including ratio of expense to sales of 2.42% (+0.02%), ratio of expense to administration of 5.26% (-0.19%) and ratio of expense to finance of 4.62% (+3.23%) which hugely increased to RMB145 million by 4.25 times, mainly due to interest expense led by the increase of debt financing in H1. Retarded by the decrease in gross margin and increase in period cost rate, net profit margin went down by 5.6% to 20.33% yoy.

In terms of finance, the company recorded a net amount of operating cash flow of RMB37.93 million, down by 24.2% yoy and receivables of RMB2.823 billion, up by 25.7% from the end of year 2016, mainly due to the rapid growth in EPC business; and an asset-liability ratio of 61.49%, down by 2.8 ppts from the end of year 2016 and monetary capital of RMB303 million, down by 76% from the end of year 2016, mainly due to green debt financing in use of project construction.

The Industry of Industrial Smoke Treatment Remains Booming. Tighter environmental supervision and environmental emission standards push the industrial circle to reconstruct under new standards and meet new emission standards. Meanwhile, with the in-depth practice of the idea of "Building a Beautiful New China" after the 19th National Congress of the Communist Party of China, the industrial smoke treatment industry is going to remain highly booming and the enterprises of this industry will embrace new growth. SPC Environment is a leading company in the field of thermal power smoke treatment. With the decrease of the demand of ultra-low emission, the company actively expands the new business of smoke dehydration and zero emission of desulfurization waste water of coal-fired power plants so as to ensure sustainable development of thermal power business. Meanwhile, the company is also actively devoted to the layout of non-electrical sector. The company acquired environmental desulfurization worth RMB1.7 billion from Aluminum Corporation of China Limited to lay out the smoke treatment of nonferrous industry in 2016; and the company also bought 100% of the stock rights of Bohuitong to lay out the smoke treatment of petrochemical industry in H1. Non-electrical sector involves fields like cement, petrifaction, metallurgy and non-ferrous metal. There is a great potential in the market of smoke treatment. Thanks to its strengths in technical reserve and R&D ability, the company is hopefully to earn greater share of the non-electrical market and contribute new growth impetus.

Risk Warnings

Macro policy risks;

The implementation of projects below expectation;

The expansion to non-electrical industry below expectation;

Financials

Click Here for PDF format...

Summary of Investment

- The industry of industrial smoke treatment remains booming;

- With a firm commitment to the layout of non-electrical sector, there is expected to be an outperforming growth;

Investment Rating

We believe that with an enormous boom in the industry of industrial smoke treatment, the leading companies will benefit continuously from it and we see a bright future in the company's early layout and active merger and acquisition in non-electrical sector which is expected to provide new growth impetus. We expect the 2017 to 2018 net profit attributable to the company to be 1010/1268mn, respectively, and EPS to be 0.94 and1.18, respectively, equivalent to PE of 25.2and 20.1, respectively. The target price is 30.00 RMB and the Buy rating is given. (Closing price as at 1 NOV 2017)

Results in the First Three Quarters Meet Expectation. According to 2017 Q3 result report, SPC Environment recorded a revenue of RMB3.134 billion, up by 57.65% yoy, a net profit attributable to parent company of RMB618 million, up by 23.99% yoy and 24.27% yoy after deduction of non-recurring profit and loss and the corresponding EPS of RMB0.575 (+23.11%). The results meet our expectation. Q1, Q2 and Q3 reported revenues of RMB672 million, RMB877 million and RMB1.584 billion, respectively and net profits after deduction of non-recurring profit and loss of RMB91 million, RMB316 million and RMB295 million, respectively. The trend of contribution quarter after quarter is positive. The company anticipates the yearly net profit margin to be between RMB856 million and RMB1.07 billion, up by 15%-45% yoy, mainly due to the new result growth from new operational businesses and the EPC program in progress.

The Decrease in Gross Margin and Large Increase in Financial Expense Retarded the Net Profit Margin. In terms of financial profitability, the company recorded a gross margin of 34.2%, down by 4.2% compared with 38.4% in the same period of last year, mainly due to the increase in raw material cost; and a period cost rate of 12.3%, up by 3%, including ratio of expense to sales of 2.42% (+0.02%), ratio of expense to administration of 5.26% (-0.19%) and ratio of expense to finance of 4.62% (+3.23%) which hugely increased to RMB145 million by 4.25 times, mainly due to interest expense led by the increase of debt financing in H1. Retarded by the decrease in gross margin and increase in period cost rate, net profit margin went down by 5.6% to 20.33% yoy.

In terms of finance, the company recorded a net amount of operating cash flow of RMB37.93 million, down by 24.2% yoy and receivables of RMB2.823 billion, up by 25.7% from the end of year 2016, mainly due to the rapid growth in EPC business; and an asset-liability ratio of 61.49%, down by 2.8 ppts from the end of year 2016 and monetary capital of RMB303 million, down by 76% from the end of year 2016, mainly due to green debt financing in use of project construction.

The Industry of Industrial Smoke Treatment Remains Booming. Tighter environmental supervision and environmental emission standards push the industrial circle to reconstruct under new standards and meet new emission standards. Meanwhile, with the in-depth practice of the idea of "Building a Beautiful New China" after the 19th National Congress of the Communist Party of China, the industrial smoke treatment industry is going to remain highly booming and the enterprises of this industry will embrace new growth. SPC Environment is a leading company in the field of thermal power smoke treatment. With the decrease of the demand of ultra-low emission, the company actively expands the new business of smoke dehydration and zero emission of desulfurization waste water of coal-fired power plants so as to ensure sustainable development of thermal power business. Meanwhile, the company is also actively devoted to the layout of non-electrical sector. The company acquired environmental desulfurization worth RMB1.7 billion from Aluminum Corporation of China Limited to lay out the smoke treatment of nonferrous industry in 2016; and the company also bought 100% of the stock rights of Bohuitong to lay out the smoke treatment of petrochemical industry in H1. Non-electrical sector involves fields like cement, petrifaction, metallurgy and non-ferrous metal. There is a great potential in the market of smoke treatment. Thanks to its strengths in technical reserve and R&D ability, the company is hopefully to earn greater share of the non-electrical market and contribute new growth impetus.

Risk Warnings

Macro policy risks;

The implementation of projects below expectation;

The expansion to non-electrical industry below expectation;

Financials

Click Here for PDF format...