Investment Summary

- Fast growth of core finance lease business;

- Bright outlook of hospital operation business;

- Unique SOE background with outstanding medical resources.

Business Overview

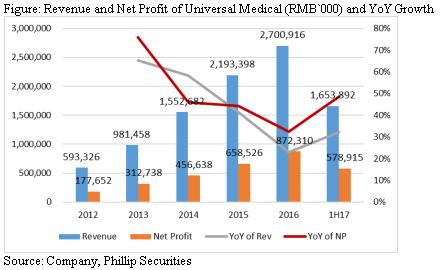

Universal Medical is a leading integrated healthcare solution provider in Mainland China. The company reported revenue of RMB2,700mn/1,653mn in 16/1H17 (+23%/32% YoY), and net profit of RMB872mn/578mn (+32.5%/48.6%). Its service mix comprises three parts: (1) medical equipment financing which constitutes the principal component (72% in 1H17); (2) healthcare industry, equipment and financing advisory services (21%); (3) clinical department upgrade services (5%). Leveraging on the central SOE background, strong medical resources platform and efficient management team, the company develops very quickly with 2012-2016 revenue/net profit CAGR of 46%/48.9%.

Favorable External Environment for Healthcare Industry Development. With population aging and increasing disposable income per capita, the Chinese government places more importance on the development of healthcare industry. The State Council in 2015 issued the Notice of the State Council on the National Healthcare Services System Planning Guidance (2015-2020). The Notice indicates that the number of public hospital beds will be increased from 4.55 per 1,000 persons to 6.00 per 1,000 persons overall and from 1.26 per 1,000 persons to 1.80 per 1,000 persons for county-level public hospitals between 2013 and 2020. Thus we see huge demand comes from hospital expansion and introduction of technology & medical equipment as well as fund support in following years.

Central SOE Background. Controlling 37.7% of Universal Medical's shares, China General Technology Group (`Genertec`) is a Central-administered State-owned Key Enterprise (SOE). Founded in 1998, it is the largest service provider introducing advanced equipment and technology, and also the largest importer and exporter of medical & health products. Genertec has created a full-chain business mode in healthcare industry, which has established cooperation relations with more than 100 countries and regions with 59 overseas branches.

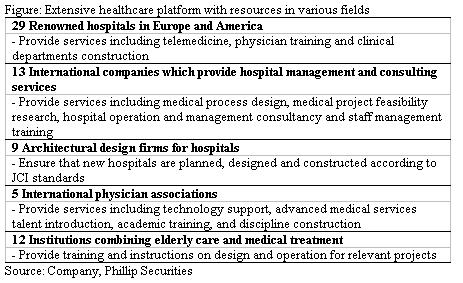

Strong Medical Resources in Various Fields. Capitalizing on Genertec's global business network, Universal Medical continues to progress its integration of international resources, which lays a solid foundation for its professional and technical advantage. The company has almost 300 in-house medical experts and established cooperative relations with over 200 renowned domestic experts. It sets up long-term cooperation with world-famous medical institutions with resources covering numerous fields.

Promising Outlook of Hospital Operation Business: International Land Port Hospital (ILPH)

(1) Partner: the First Affiliated Hospitalof Xi`an Jiaotong University. Together with the partner, the company is going to build a branch of the First Affiliated Hospital. FAH is a leading comprehensive Grade III Class A hospital in Northwest China, with 2.25 million outpatient visits in 2015 and 2,541 beds. It is the leader in terms of medical technology and service quality in Northwest China, having 14 state-level key clinical subjects, 5 province level key clinical subjects and 7 province-level dominant subjects. Its outstanding physicians and doctors are widely recognized within the industry. The revenue of FAH reached around RMB3.5bn/4bn in 2015/2016. It is estimated that the supply chain business of FAH is worth RMB2bn (nearly half of the turnover).

(2) International Land Port Hospital. ILPH is located in Xi`an International Trade & Logistics Park, with the area of 0.25 km2 and 1000 beds planed. Universal Medical will invest no more than RMB2bn and the initial investment is about 1.5 billion, with the rest to be invested within 3-6 years after the hospital comes into operation. At beginning Universal medical will actually invest no more than 0.4 billion as capital input with the rest to be achieved by project financing.

(3) Ongoing Progress. Universal Medical established the project firm Xi`an Ronghui for construction and operation of IPLH. Xi`an Ronghui (80%) together with FAH's project company (20%) has built Xi`an Wanheng as a medical supplies procurement management platform, and through Xi`an Wanheng the company finished the acquisition of a GSP firm. In this July Xi`an Wanheng has renovated the GSP firm, as the company is going to take over the supply chain of FAH soon. Now the existing warehouse of 5,000 sq.m and refrigerator trucks are prepared for the business undertaking, and the market expects that the supply chain business will start to generate income from 2H17.

(4) Future income from two main rights. The cooperation with FAH brings the company two rights, including construction and operation right of ILPH and business cooperation right (taking over the supply chains of FAH and ILPH). On one hand, after the completion of the IPLH construction, Universal Medical will charge construction and operation fee indicating 80% of ILPH EBITDA every year. The construction and operation right bears a term of 25 years, and the ratio 80% will declined to 50% when the return of investment reaches 100%. On the other hand, the project company of Universal Medical will receive 80% stake of dividends paid by Xi`an Wanheng with its supply chain business.

Fast Growing Core Business: Finance Lease

(1) Rapid growth since 2012

Finance lease making up 72.34% of topline in 1H17 is the core business of the company which focuses on medical industry. The figure bellow shows that the finance lease developed dramatically with FY12-FY16 CAGR of 56.99%. Healthcare industry is the main source of segment revenue with contributing 77% to finance lease income in 2016, while the education business is a complement to the core hospital business, which helps the company to maintain good relationship with the local government.

(2) Solid Costumer Base Contributes to Good Asset Quality

According to Frost & Sullivan, revenue of regional and county level hospitals is expected to grow at a CAGR of 18.5% between 2014 and 2018. The company targets these regional and county level hospitals as key customer base since they have high growth potential. In 2017, Universal Medical provides service to more than 1,400 Class 2 above hospital customers covering 30 provinces in China, 80% of which earn more than RMB100mn per year.

Not-for-profit public hospitals usually have strong cash flows and are not that sensitive to interest rate. They value whether the supplier can provide tailored service to help them improve efficiency and introduce advanced equipment of excellent quality. Strong international resources and rich industry experience make Universal Medical enjoy high customer loyalty. Many hospitals are the company's repeat customers.

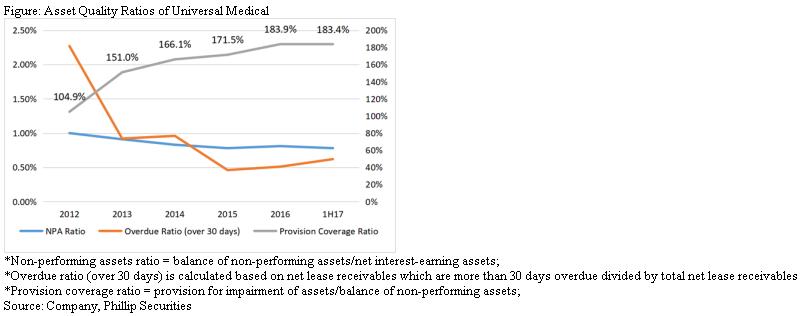

Professional staffs are sent to potential customers to conduct due diligence investigation to estimate whether the customers are capable to carry on lease obligations. After selection, qualified customers with strong cash flow and stable financial condition form a solid base for good asset quality, given the company has never wrote off any accounts receivables until now. The following chart also shows that NPA ratio and Overdue ratio are quite low while Provision coverage ratio is increasing stably indicating highly safety.

(3) Impressive Operation Efficiency and Profitability

The company's finance leases are usually between three to five years in duration and are generally priced at an interest rate floating at a predetermined spread above a base interest rate. The base interest rate is usually referenced to the benchmark interest rates set by People's Bank of China (PBOC) and the predetermined spread will be decided by specific customer based on its risk profile.

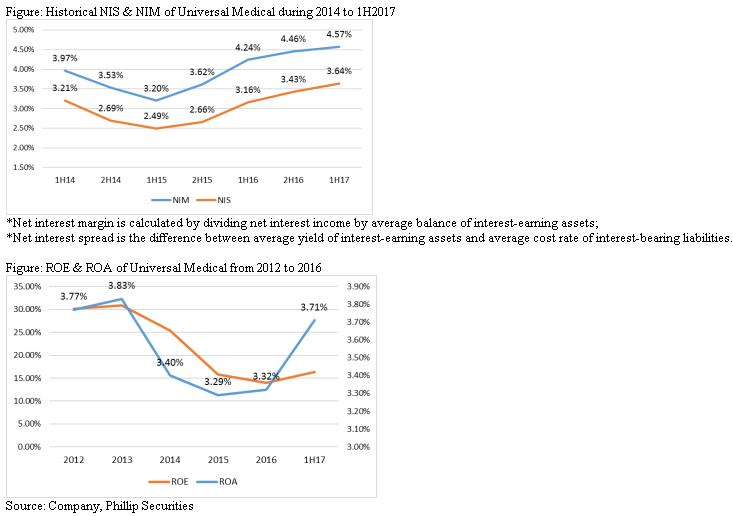

The following chart sets forth Universal Medical's net interest margin (NIM) and net interest spread (NIS) since 2014. Before 2015, the company focused on offshore RMB borrowings as main financing source. As the domestic interest rate was cut down and offshore deposit and lending interest rates hiked due to tight liquidity, the NIS & NIM bottomed out in 1H15. Therefore the management adjusted liability structure through expanding credit line granted by the major domestic lending banks and prepaid some offshore RMB debt. Continued diversification of its borrowing portfolio effectively controlled financing costs and exchange rate risks. In 1H17, both NIS & NIM reached a record high level. We see that the management is of good efficiency and very professionally experienced.

Development of Advisory Business and Clinic Upgrade Service. By providing integrated services to hospital clients, the company is prone to cross-sell different services and solutions across large base of hospital customers. Besides finance lease, the company also provides advisory services and clinical department upgrade services.

(1) Industry, Equipment and Financing Advisory Services

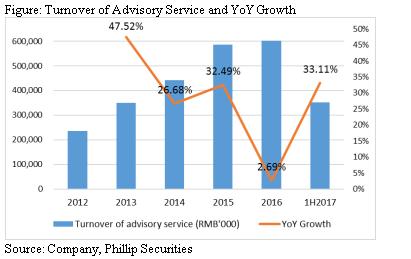

Universal Medical offers comprehensive advisory services which are customized based on the specific requirements of customers, with a focus on industry, equipment and financing. The industry advisory service helps to analyze the competitive landscapes of hospital clients. It uses statistical data to seek diseases that are underserved but prevalent in the region, in order to find the most profitable and efficient growth strategy for hospitals. Universal Medical also helps its customers to choose most suitable and cost-effective equipment. Meanwhile, it gives suggestions about financing options, cash management and operation of purchased or leased assets. This advisory service has achieved quick development with 2012-2016 CAGR of 26.7%. In 1H17, this segment realized 33% YoY growth accounting for 21.9% of company revenue.

�

(1) Clinical Department Upgrade Services

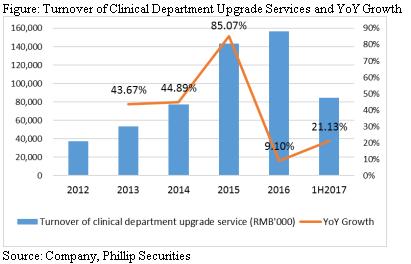

Leveraging on the wide client coverage and enriched industry resources, Universal Medical has developed and now offer CVA (cerebral vascular accident) project solutions and finance lease. The company integrates internal and external resources to assemble project team to provide medical training and support for doctors and professionals, as well as awareness promotion and marketing support. This business posted 2012-2016 CAGR of 43.18% and recorded 21% YoY growth in 1H17. Given it only making up 5% of the topline, we believe that there is still quite room to grow through continued promotion by technology.

Investment Summary

We think future growth drivers coming from: (1) Favorable external environment. National policies encourage to build hierarchical diagnosis and treatment system and boost hospital development in Tier II & III cities. This will further stimulate the need of hospital construction and expansion as well as demand for medical equipment. (2) Promising hospital operation business. Not-for-profit hospitals have strong cash follow and also incentive to outsource the supply chain under two-invoice system. Besides ILPH, the company is also planning for another new project in Handan city. Its expanding hospital client base underpins the development of hospital operation business and other related services. (3) SOE shareholder and comprehensive international medical resource form unique momentum.

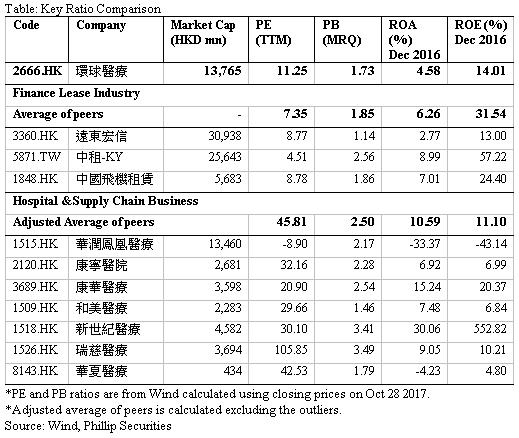

Meanwhile, PE and PB ratios of Universal Medical are much lower than peers` average levels which focus on hospital operation and supply chain business. And the company enjoys better profitability given relatively high ROE among hospital-focused firms. With its hospital operation business to take off, we expect that Universal Medical to achieve notable development in future.

Financials

Click Here for PDF format...