Investment Summary

- Strong sales network with increasing direct academic promotion;

- Professional management and sales team with good control over selling cost;

- Promising pipeline is likely to serve as future growth momentum.

Business Overview

China Medical System (CMS) is a China-based pharmaceutical services company, engaged in the marketing, promotion and sale of prescription drugs of overseas and domestic specialty pharmaceutical companies. CMS was founded in 1995 and listed on HK main board in 2010. In 2002 it started to promote drugs namely Deanixt (for mild to moderate depression and anxiety) and Ursofalk (for dissolution of cholesterol gallstones in the gallbladder) in China, and now has 19 main products sold in PRC market. Its sales achieved FY12-16 CAGR of 28.9% with net profit recording FY12-16 CAGR of 26.6%.

Progressive Product Introduction Strategy.

CMS focuses on obtaining exclusive promotion and selling rights from international and domestic pharmaceutical companies for in-licensed products with high growth potential. The company leverages on its internal and external resources to identify products that have relatively high gross profit margin, clear therapeutic efficacy and significant market potential or unmet needs in PRC. CMS introduces the qualified medicines to China through obtaining product rights, Chinese market rights, or signing exclusive agreement. The company also builds the hierarchical product introduction strategy, which lays solid foundation for sustainable growth in different stages. In short run, CMS introduces products that can be immediately launched in market, while in medium term the company tends to select products which have been launched in overseas markets, but have not gained China Import Drug License (IDL). Meanwhile, the company chooses innovative products at late stage of R&D as long-term pipeline products. We think that acquiring innovative drugs at late R&D phase helps to save research cost and avoids failure risk in early research stage.

This progressive introduction strategy contributed to the quick development in track record period. We see that from 2012 to 2016, the company continued to enrich its product portfolio and realized topline growing at CAGR 28.9%. Although the China medical reforms to some degree cause price pressure on some drugs, the company still remains relatively strong pricing power given the wide usage and proven efficacy of the main products. Also, considering relatively high profit margin of CMS products, we still expect quite room of future profit despite of price cut due to drug tenders.

Professional Sales Management and Extensive Distribution Network.

CMS staff all have educational background in medicine or pharmacology, and most of them possess profound clinical experience. As to the end of 2016, the company has built a sales team with 2,800 salesmen covering 44,000 hospitals and institutions. CMS promotes products through main direct academic promotion network and agency promotion network with covering 44,000 and 7,900 hospitals respectively.

One market concern before is that CMS may be adversely impacted as a drug distributor after the rollout of two invoice system. In fact, CMS will deliver the `first invoice` given it introduces foreign drugs then sells to domestic hospitals. For drugs produced by subsidiaries which CMS controls less than 50% shares, CMS changes its buy-sell model into charging promotion service fee or royalty fee (mainly for drugs including Plendil, XinHuoSu, NuoDiKang and Imdur). As for agency channel, the company continues to enhance promotional service model which is hospital-based and seek to achieve long-term partnership with agencies.

Comprehensive Product Portfolio.

The company now has 19 products in its product mix, 16 of which are promoted by direct academic channel. Majority of its products are included in National Reimbursement Drug List (NDRL) or Provincial Reimbursement Drug List (PDRL). In 1H17, top four products contributed to 70% of total sales.

Plendil (波依定), introduced in 2016, is a new product under the Direct Network with a 20-year exclusive license for the commercialization in China. Plendil is an original product and used to treat hypertension and stable angina pectoris. It is the sustained release formulation of Felodipine, which controls the blood pressure smoothly with clear efficacy and low rates of instances of side effects. Plendil recorded sales of RMB935mn/643mn in 16/1H17, which is estimated to realize 10%/9% YoY growth in 17E/18E. (2017 growth rate is based on adjusted 2016 result, given the product started to contributing to revenue in Mar 2016.)

Deanxit (黛力新) is used in the treatment of mild to moderate depression and anxiety and is on the NRDL. According to IMS data in 2016, Deanxit is the most prescribed antidepressant drug in China. Deanxit recorded sales of RMB 917.9mn/483mn in 16/1H17, representing 1.5%/18% YoY growth. The low growth rate in 2016 was attributable to the withdrawl of tender in Guangdong due to low price. Considering it again entered into Guangdong market in April 2017, we expect sales of Deanxit to gradually recover this year and grow at 20%/10% YoY in 17E/18E.

Ursofalk (優思弗) is for the treatment of cholesterol gallstones in the gallbladder, cholestatic liver disease and biliary reflux gastritis. IMS data shows that in 2016, Ursofalk is the best-selling ursodeoxycholic acid drug in China, and ranked No.1 in terms of sales among digestive products in PRC cholagogue market. The product posted turnover of RMB771.9mn/442.2mn in 16/1H17 with 16.7%/24.6% YoY growth. We expect Ursofalk to maintain 25%/20% growth in 17E/18E through continuing to raise its hospital coverage.

XinHuoSu (新活素) is a National Class One biological agent which is used to treat acute heart failure. It is recommended by the first “Acute Heart Failure Diagnosis and Treatment Guideline” in PRC, and has gradually become the standard medication for treating acute heart failure. XinHuoSu reported sales of RMB537.4mn/304.5mn in16/1H17, and entered into NDRL in July 2017. We estimate that the sales volume may show notable growth with the rollout of new NDRL next year, while the price drops by 40% due to the negotiation. Given its potential sales volume growth and price cut, we estimate Xinhuosu to grow at 38%/15% in 17E/18E.

Promising Pipeline with Potential Future Driver

Tyroserleutide (CMS024) is a National Class One New Drug for the treatment of liver cancer. The research company Kangzhe R&D controlled by the Chairman Lam Kong is processing the research and listed company CMS will have the rights of production, sales and promotion of CMS024. There is no R&D expenses incurred by the listed company, but a royalty fee representing 13% of the sales will be paid to research firm after the successful commercialization of CMS024.

In 2014, the phase III clinical trial of CMS024 was unblinded, and the preliminary statistical analysis suggests that the trial failed to achieve its aim to register for selling the drugs in the China market. After the unblinding, Kangzhe R&D pursued the follow-up study and a statistical significance of survival time between the treatment group and placebo group in this subgroup has been observed. It shows that CMS024 has a tendency of prolonging survival time of liver cancer patients with no tumor thrombosis. CMS024 now is under the phase III extended clinical trial which was still in the patient recruitment stage and progressed smoothly.

Traumakine is for the treatment of acute respiratory distress syndrome (ARDS). ARDS is one of the common acute and critical clinical diseases with no targeted drug treatments currently. Morbidity of ARDS is 59/100,000 yearly in China and the mortality is high (China 50%, Europe and America 35-45%). Traumakine is developed by a Finland firm and the listed company acquired the product assets in China. The company will pay the research institution a royalty fee in respect of a percentage of its net revenue in China after the successful commercialization of the product. Traumakine has finished phase I/II clinical study in UK, and the phase III clinical trial is divided into two separate studies conducted sequentially in time.

We estimate that if the clinical trial and application for production process smoothly, these two drugs are likely to be commercialized in around two to three years. These new drugs with great market potential are expected to become future growth momentum given its innovation and CMS's outstanding promotion power.

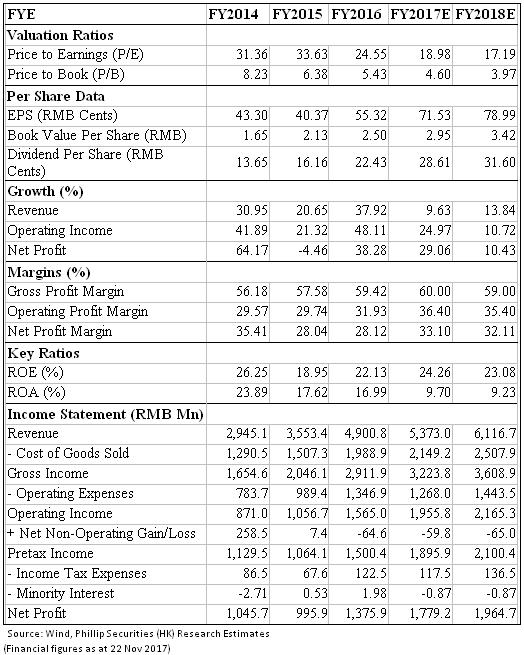

Financial Analysis

Excluding the effect of two invoice system, the company reported revenue/net profit of RMB2.7bn/925mn representing 35%/33.5% YoY growth. From 2012 to 2016, CMS's revenue/net profit grew quickly at CAGR 28.9%/26.6%. CMS generally maintained stable profit margin in recent years, and from 2015 both GPM & NPM continued to improve and reached a record high in 1H17. We predict each product growth to derive turnover in 2017 and 2018 and assume that profit margin will generally maintain steady.

CMS recorded 5-y average selling/administrative expense ratio of 21.9%/5.65%, while in 1H17 attributable to improving management efficiency and economies of scale, these two ratios declined to 19.6%/3.6% excluding the effect of two invoice system. We estimate selling/administrative expenses to be 20%/3.5% in following two years.

Investment Thesis, Valuation & Risk

Our valuation model gives price target of HK$17.93, which is based on PE analysis and estimation of each product growth in 17E/18E without effect of two invoice system. We think future growth momentums arising from: 1) Increasing penetration of current products. For example, XinHuoSu, consisting 11.3% of 1H17 topline, generated 60% income from 100 hospital, while it totally covers 1,000 hospitals. Given CMS's products have notable efficacy and most are included in NDRL/PDRL, we see great potential from existing products to improving their current penetration. 2) Expanding distribution network to cover more hospitals and cities. With the further implementation of hierarchical medical system, the drug market is expected to experience further flourishing with development of county level hospitals and grass-root healthcare institutions. We expect that CMS continues to proactively conduct academic promotion in more lower-tier market to boost its sales. 3) Promising pipeline products are likely to underpin the market confidence to its future growth consequently deriving more favorable valuation. (Closing price as at 22 Nov 2017)

Financials

Click Here for PDF format...