Investment Summary

- Sales in "Golden September" and "Silver October" Had Excellent Results, Hitting a New High in October.

- The SUV sales made up 54% of the total, among which BoYue sold over 30,000 units, leading to further optimization of the sales structure.

- The LYNK&CO order remains large, and its strong product cycle will go on for two years.

Investment Thesis

The platform technology of standardized and modularized production, the late-mover advantages from corporation with Volvo, and the company's strong cost control ability and gradually mature concept of car manufacturing have provided strong momentum towards its new round of development. The recent redemption of the notes lifts restrictions on the increase of the company's existing dividend payout ratio of 15%; the dividend rate is expected to substantially increase in the future.

We are optimistic about its steady growth in medium and long term sales. As for the valuation, considering the better sales momentum and higher dividend yield in the future, we lift target price to HK$ 33 on our revised forecast EPS, equivalent to 26.4/19.4/14.2x estimated P/E ratio of 2017/2018/2019. (Closing price as at 23 Nov 2017)

Sales in "Golden September" and "Silver October" Had Excellent Results, Hitting a New High in October

The sales volume of Geely Auto reached 125,100 units in October 2017, representing a vast increase of 30% yoy. In the first ten months, Geely Auto's total sales volume reached 952,200 units, approximately up 72% yoy, already achieving 87% of its goal of annual sales volume. In view of this gratifying sales volume, we predict the annual sales volume will be much likely to exceed the set target of 1,100,000 units and even expect to achieve a higher result of 1,200,000 units, increasing over 50% yoy. It excels in the China's auto industry as the average growth rate in the sector slowed down to single digit.

The SUV sales made up 54% of the total, among which Bo Yue sold over 30,000 units, leading to further optimization of the sales structure

In terms of models, the sales of Geely's six main models stabilized at over 10,000 units per month. 27,033 units of the sedan model Imperial were sold, up 8% yoy and 14% mom; 13,513 units of the crossover Imperial GL were sold, up 90% yoy and 12% mom.

The sales volume of Bo Yue SUV, the most high-end model of SUV, broke through 30,000 units in October at its first try, up by 80% yoy and 15% mom to 30,318 units. It is a main supporting factor that plants in Baoji and other cities expanded and released capacity. Such a brilliant sales volume of a new model which was launched just one and a half years ago, fully demonstrated Geely's increasingly mature development in manufacturing concept, technology and marketing etc. And the sales volumes of other SUV models are as follows: Vision SUV 11,214 units, Imperial GS 16,063 units, and the small SUV X1 and X3, 3,061 units and 7,007 units, respectively. The proportion of SUV increased from 37% at the end of last year to 54%. The sales structure was further optimized, and therefore the gross margin was expected to reach a new high.

The LYNK&CO order remains large, and its strong product cycle will go on for two years

The first LYNK&CO 01 sedan with a 2.0T+6AT specification, a model of Geely's new brand LYNK, is able to be reserved now. The price range is between RMB170,000 and RMB240,000, and the exact price will be released on November 28. For now, the order of this new model is better than expectation. Another new model with a 1.5T specification will be launched in 2018 to further increase consumer size and capture more demands.

At the same time in Guangzhou International Automotive Exhibition, Geely has launched a brand-new model of Vision S1, a second crossover SUV whose positioning is a bit below Imperial GS. With the launch of Vision S1, Geely's product chain of SUV is further strengthened.

Looking into the future, in the support of the new technology platform iNTEC, the company will remain the same efforts to launch new cars in the next two to three years. Considerable new models will be unveiled in 2018/2019. Upgraded versions of the existing models will be launched successively. Besides, Geely Auto will launch 8 brand-new models in 2018, including LYNK&CO 02 and 03. And in 2019, the company will continue to launch no less than 5-6 brand-new models, enriching its product portfolio.

The platform technology of standardized and modularized production, the late-mover advantages from corporation with Volvo, and the company's strong cost control ability and gradually mature concept of car manufacturing have provided strong momentum towards its new round of development. The recent redemption of the notes lifts restrictions on the increase of the company's existing dividend payout ratio of 15%; the dividend rate is expected to substantially increase in the future.

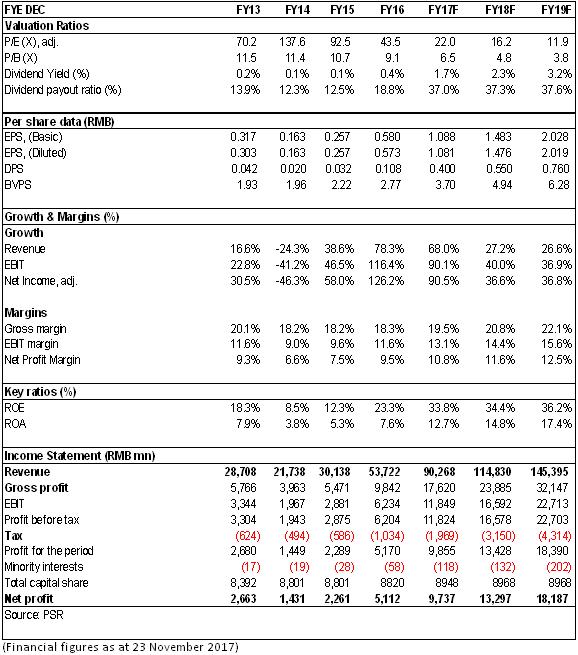

Financials

Click Here for PDF format...