Investment Highlights

-Integration synergies with main subsidiaries;

-M&A driving future growth through external expansion;

-Enhancing product R&D development capabilities and optimizing distribution network;

-Favorable policy environment facilitating market leader to improve industry concentration.

Business Overview

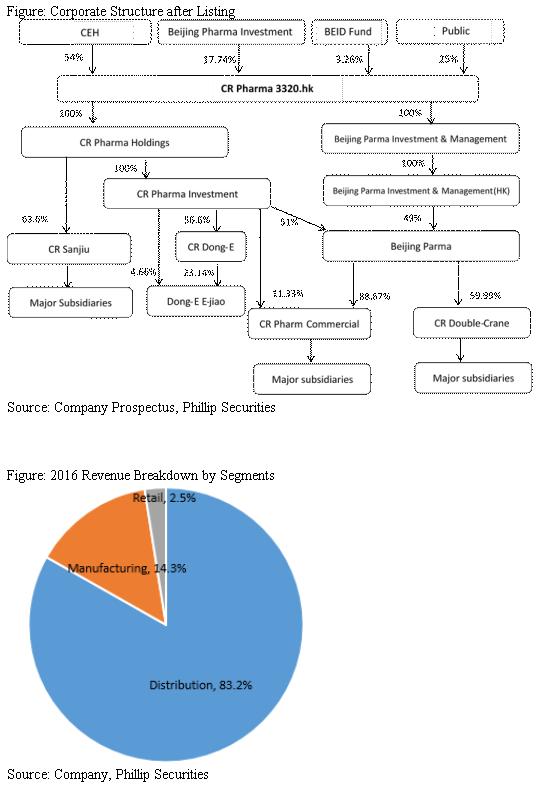

China Resources Pharmaceutical (CR Pharma) is a leading pharmaceutical company in China. It is committed to distribution, manufacturing and retail of pharmaceutical and healthcare products in PRC. The company was established in 2007 and now becomes the second largest pharmaceutical manufacturer and the second largest distributor in China. In Oct 2016, the company was listed on HK main board. From 2013 to 2016, CR Pharma achieved revenue CAGR of 10.25%, and net profit CAGR of 2.25%. Distribution, Manufacturing and Retail businesses respectively accounted for 83.2%, 14.3% and 2.5% in 2016 revenue, with average gross profit margins of 6.61%, 58.33% and 21.21% respectively.

Pharmaceutical Distribution.

CR Pharma is the second largest pharmaceutical distributor in PRC providing comprehensive distribution solutions to pharmaceutical producers and dispensers. By the end of June 2017, it has more than 110 subsidiaries in 27 Chinese provinces and distributes over 100,000 kinds of products, including 40,000 prescription drugs and 15,000 OTC products. It sources products from over 10,000 domestic and international pharmaceutical manufacturers. And it now has 6,400 customers, involving 5,085 Class II&III hospitals and 32,164 primary medical institutions.

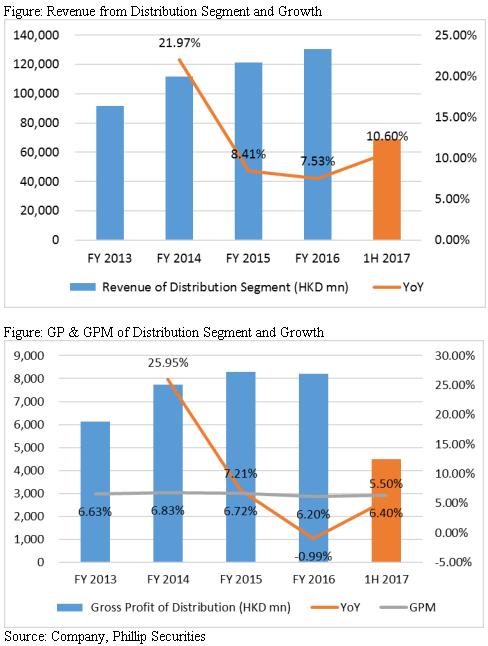

Distribution business recorded FY13-16 CAGR 12.45% with average GPM of 6.61%. Meanwhile, this segment posted income growth 10.6% YoY to HKD70.4bn in 1H17, mainly arising from expansion of breath and depth of network coverage. As a leading distribution firm in the market, CR Pharma is expected to take advantage of the two invoice system and continue to externally expand through M&A. We expect that CR Pharma continues to expand distribution coverage, given it just entered four new provinces (namely Jiangxi, Hainan, Qinghai and Xinjiang) in first half. To enhance competitiveness, the company explores to enhance value-added services to downstream customers. As at end of June, the company provided hospital logistic intelligence (HLI) services to over 200 hospitals, and commenced network hospital logistics intelligence (NHLI) projects.

Pharmaceutical Manufacturing.

CR Pharma is one of the largest manufacturing firm and the largest OTC drug manufacturer in China. It is dedicated in R&D, manufacturing and sale of a wide range of pharmaceutical and healthcare products. It produces around 450 pharmaceutical products (300 of which are included in NDRL), with many famous brand names such as CR Sanjiu, Dong-E-E-Jiao, CR Double-Crane and CR Zizhu. Three main subsidiaries function differently. CR Sanjiu is the platform of OTC product (mainly involving Chinese medicines), and CR Double-Crane is the major producer of chemical drugs while Dong-E-E-Jiao offers traditional healthcare products to high-end customers. CR Parma's product portfolio covers key therapeutic areas involving cardiovascular, cold remedies, anti-infection, track & metabolism, dermatology, pediatrics, etc.

This segment reported FY13-16 CAGR 2.4% with average GPM of 58.33% and posted 3.8% YoY growth to HKD12.69bn in 1H17. We see that 49% of segment income is generated from Chinese medicines, 42% from chemical drugs, while Nutritional & Healthcare portfolio and Biopharm respectively makes up 1% of segment turnover. Gross profit and GP margin of manufacturing business significantly increased in first half (+7.7%/+0.36ppts), attributable to continuous improvement of production techniques and upgrading product mix.

Pharmaceutical Retail.

The company operates and franchise a network of retail pharmacies across 16 provinces in PRC and HK, with a comprehensive and diversified product mix. It owns 745 retail pharmacies with premium brand names, i.e. Yibaoquanxin (醫保全新), Li`an Chian (禮安連鎖), Tung Tak Tong (同德堂), etc. Retail business achieved FY13-16 CAGR 14.6% with average GPM of 21.21%. Meanwhile, this segment reported sales growth 10.2% YoY to HKD2.12bn in 1H17, while gross profit margin decreased by 2.9ppts (1H16 20.1%, 1H17 17.2%). We attribute this to the rapid growth of direct-to-patient (DTP) business, which has a relatively low profit margin. As at end of June, the company operated 81 DTP pharmacies covering 44 cities in the PRC.

Stock Valuation

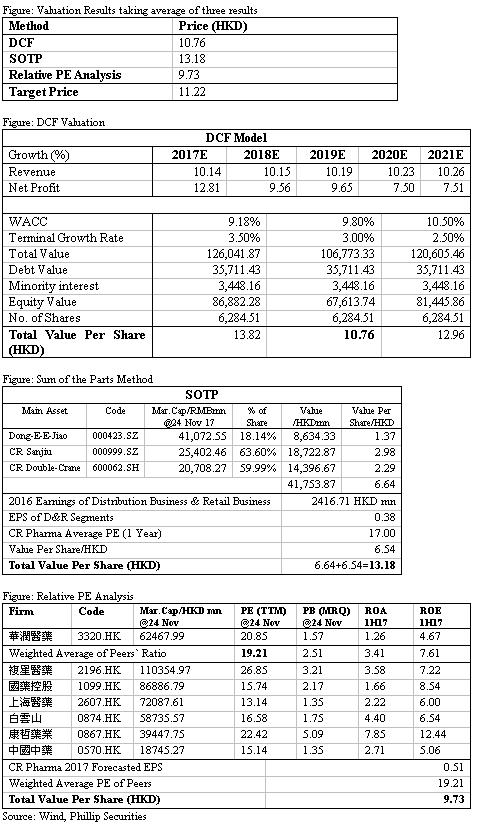

We use three methods to estimate the stock price (including DCF valuation, Sum of the Parts (SOTP) and Relative PE Analysis), and take the average of three results to get our final target price of 11.22HKD per share. Our DCF model predicts growth rate of each business segment to derive the topline growth. The followings are valuation details. (Closing price as at 27 Nov 2017)

Investment Thesis & Risk

Our valuation models derive the target price of 11.22HKD, and we think future growth momentums mainly coming from following aspects.

1) Favorable external environment facilitates industry integration and company expansion. With the further implementation of two-invoice system, we expect more obvious impacts on the pharmaceutical distribution industry. Establishment of hierarchical diagnosis system will also further stimulate the demand for medical service and products. We highlight the importance of superiority in scale and capital, and CR Pharma will form significant advantage in industry consolidation as leading market player.

2) Expanding pharmaceutical manufacturing business and upgrading product portfolio. As to end of June, the company had 225 projects about researches on innovative drugs, generic drugs and product improvements, and 32 projects were pending registration approval CFDA. The company places importance on R&D and technique improvement with rising R&D expenses (which consists 3.1% of total revenue in 1H17). Also it continues to seek collaboration opportunities with international and domestics partners in key medical areas. We expect further progress made by win-win co-operation.

3) Synergies among main subsidiaries and potential price premium. CR Pharma's three major subsidiaries (Double-Crane, E-Jiao and Sanjiu) are all listed companies in PRC. CR Pharma will not only benefit from their good business performances, but also enjoy potential price premium from these listed firms. According to our SOTP valuation, the company stock price should be 13.18HKD given 17x PE, in consideration of subsidiaries` market value.

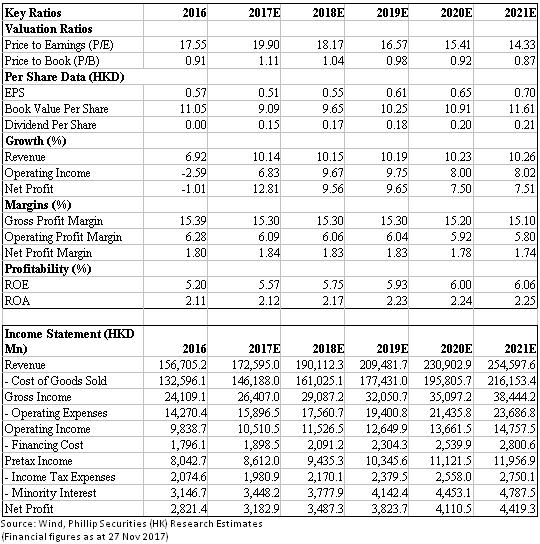

Financials

Click Here for PDF format...