Investment summary

- Nearly 10% Increase in Net Profit in the First Three Quarters

- Business Data Leading in Three Airline Giants

- The Low Season of the Fourth Quarter under Great Expectations

Investment thesis

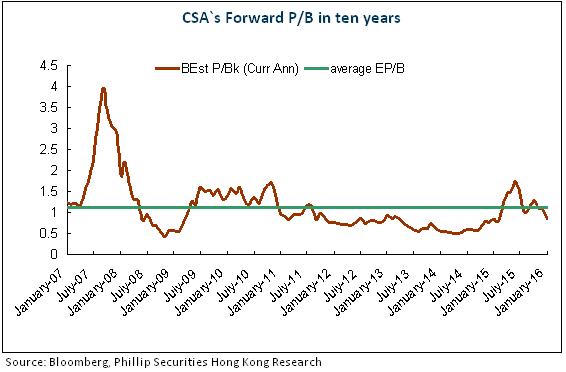

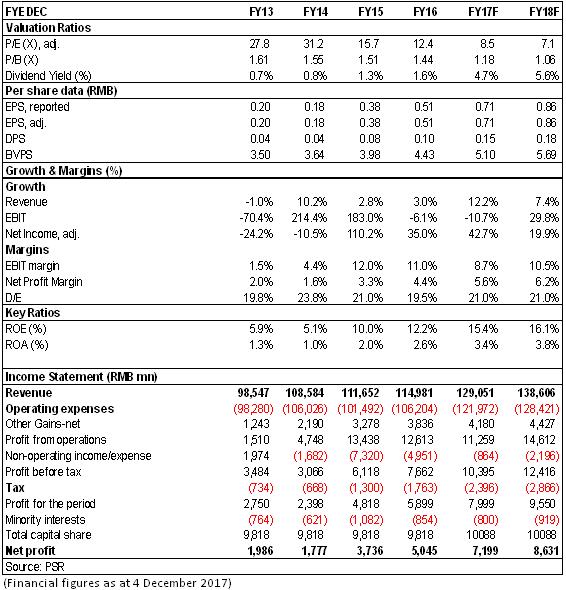

On the premise of the improvement of the supply and demand pattern, we expressed cautious optimism for the promotion of the industry next year. In August, CSA raised H-shares and introduced U.S. airline strategy investors, which was expected to help to develop the company's Euro-American flight. At the same time, the company's project of raising RMB13.3 billion is moving forward, which will further increase assets when finished. In accordance with the latest data, we adjust the estimate of the Company's EPS to RMB0.71/0.86 in 2017 and 2018. The target price is HK$8.45, equivalent to 10/8.3x and 1.4/1.25x estimated P/E ratio and P/B ratio, respectively, in 2017 and 2018. The "accumulate" rating is given.

Nearly 10% Increase in Net Profit in the First Three Quarters

China Southern Airlines (CSA) reported a total revenue of RMB96.12 billion in the first three quarters, up by 11% yoy, and its net profit attributable to the parent company amounted to RMB7.05 billion, soared by 9.5% yoy, with the smallest growth among the three airline giants in China. The main reason was that the cardinal number during the same period of the previous year was high and the EPS was RMB0.71 while last year's EPS was RMB0.66 in the same period.

Three Factors Drive the High Growth of the Result

We thought that there were three major reasons for the steady growth of CSA's result.

1. The main business grew steadily. The macro-economy developed slowly but continued to recover. The demand of business travelers and tourism residents was rising steadily.

2. Fuel costs remained stable and the international crude oil prices fluctuated in the range of USD40-55 per barrel, providing a stable and low-cost advantage for airline companies.

3. The depreciation trend in these three years has changed and the stabilization of the RMB rate has greatly improved the exchange gain of airline companies since 2017.

Oil &RMB Rate Load Shifting

Another characteristic of airlines` result this year is that the result's difference between low season and peak season was smaller. CSA's EPS in Q1, Q2 and Q3 was RMB0.16, RMB0.12, RMB0.42, respectively, reduced by 42%, rocketed by 177% and 29% yoy, respectively, from last year's RMB0.27, RMB0.04, and RMB0.34, respectively. The very low oil price during 2016Q1 is the leading force of the decline of the result in 2017Q1. The rapid growth of RMB rate in 2017Q2 and Q3 greatly improved the exchange gain of airlines this year, with RMB902 million financial costs, down by 76.42% yoy for CSA in 9M2017.

Costs Well-controlled

The company's costs were controlled well and the cost ratio continued to reduce. The sales cost in the first three quarter was RMB4.918 billion, up by 6.15% yoy, accounting for 5.12% in the revenue decreased by 0.23 ppts yoy; the administration expenses were RMB2.328 billion, up by 5.77% yoy, accounting for 2.42% in the revenue decreased by 0.12 ppts yoy. As at the end of September 2017, the scale of the fleets of the company, compared with last year's, had a net increase of 39 to 741 aircraft, including 265 self-owned aircraft, 210 finance lease aircraft and 266 operation lease aircraft; according to the capacity introduction plan, there is going to be a net increase of 16 aircraft in Q4.

Operating Data Leading in Three Airline Giants

In the first three quarters in 2017, CSA's passenger traffic and capacity(RPK/ASK) were up by 11.5% yoy and 9.2% yoy, respectively, whose growth rates were up by 4.0 ppts and 1.2 ppts, compared to the same period of the previous year. The P L /F were up by 1.7% to 82.2% yoy, which was the highest among the three airline giants. In October 2017, CSA's RPK/ASK was up by 10.5% and 9.9% yoy, respectively, and P L /F was 82.00%, slightly up by 0.43 ppts.

The Low Season of the Fourth Quarter under Great Expectations

In order to control the frequent flight delays, the CAAC announced a more strict time scheme and controls industry capacity delivery from the perspective of flight supply. The situation of low supply and high demand in front-line airports was more prominent, which helped the airline companies to raise the ticket price. Seen from the latest booking situation, business travelers` demand was obvious. The ticket price level of domestic flight was improved compared with the same period last year and the cardinal number of international flight during the same period of the previous year was low due to irresistible factors. We expected that airline companies can have better results in the low season of the fourth quarter.

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast.

War, terrorist attacks, SARS and other emergencies;

Irrational inter-industrial price war;

Financials

Click Here for PDF format...