Investment Summary

In November the company announced to acquire Cardinal China, another giant pharmaceutical distributor in PRC, which will further consolidate its leading position in distribution market and accelerate the development of its DTP business. We see modest growth in 9M17 results with improving profit margin and quickly development of manufacturing segment. Assuming 14x PE, we give target price of HKD25.2 and `BUY` rating with 29.76% upside. (Closing price as at 6 Dec 2017)

Business Overview

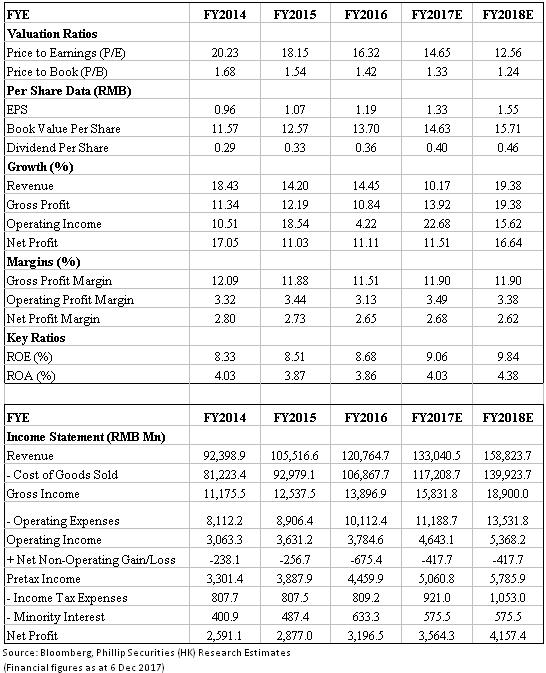

Stable growth in 9M17 results. As up to end of Sep, the company delivered revenue of RMB99bn (+9.41% YoY) and net profit attributable to shareholders of RMB2.69bn (+9.42% YoY), while net profit recorded 14.26% YoY growth excluding effect of declining JV earnings. The profit from JV decreased by 10.67% YoY due to rising expenses for new products and price cut of some drugs. We see improving operation with rising net operating cash inflow of RMB1.85bn (+0.54bn YoY).

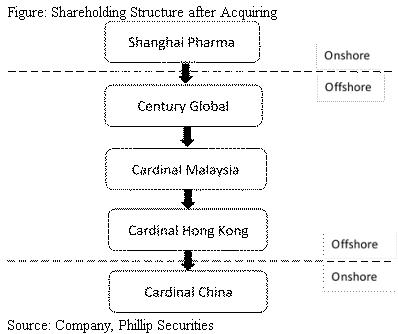

Acquisition of foreign-capital distributor in PRC. On 15 November, the company announced that its subsidiary would acquire 100% of Cardinal China at a price around USD557m. Cardinal China is a foreign-capital pharmaceutical distributor in China, covering 322 cities and offering service to 11,000 medical institutions and other downstream customers. The acquisition will enable the company to vertically strengthen its network in Shanghai, Beijing, Zhejiang and cover more end-user clients. Meanwhile, it will also expand blank regionals such as Tianjin, Chongqing and Guizhou, which helps the company to expand its distribution network to 24 provinces. After completing the acquisition, the company will own the most agent categories of imported pharmaceuticals and become one of the largest agents and distributors of imported pharmaceuticals. We estimate that inclusion of Cardinal business will enlarge the distribution revenue by c.15% in 18E.

Medical reforms facilitate DTP business. DTP (direct to patient) Pharmacies purchase drugs from manufacturers then according to doctors` prescriptions sell drugs to patients and offer delivery services. Medical reforms policies, involving limiting drugs sales revenue percentage for public hospitals and zero mark-up on drug price, encourage hospitals to transfer a part of drug sales business out. Pharmacies nearby hospitals and DTP pharmacies are expected to share the market of prescription outflows from hospitals. Pharmacies nearby the hospitals enjoy geographic advantage as they are close to hospitals and accessible for patients to purchase drugs after seeing the doctors. They often provide a wide range of products, but offer limited value-added services. DTP pharmacies mainly provide new special medicines for diseases of high incidence with high gross profit margin and high customer loyalty. At the same time, DTP pharmacies offer chronic disease management service to meet patients` long-term healthcare needs as well as other professional and related services. We think that under the two-invoice system, the manufacturers are willing to directly access to end users. Selling through DTP pharmacies can help manufacturers to reduce intermediate distributors and collect patients` feedbacks easily, while patients can also enjoy more customized services.

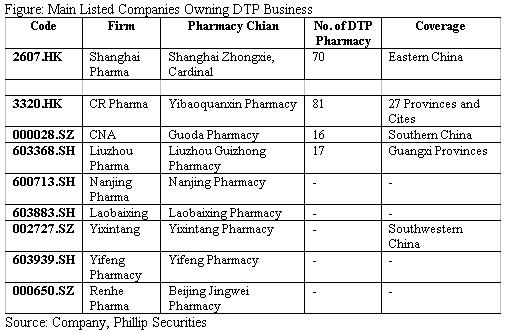

DTP business is expected to develop quickly. Shanghai Pharma has more than 40 DTP pharmacies in eastern and northern China, while Cardinal China owns 30 DTP pharmacies in 22 PRC cities. Shanghai Pharma as market leader owns rich upstream resources and Cardinal China traditionally has advantages in importing foreign new drugs. After the acquisition, the company will have the biggest DTP pharmacy chain in PRC with comprehensive domestic and international medical resources which can better satisfy patients` needs for new special medicines.

Distribution business recorded stable growth. As up to the end of Sep, Shanghai Pharma's distribution business reported revenue of RMB87.9bn (88.7% in total revenue) representing 8.33% YoY growth with net profit reporting 11.38% YoY growth. We attribute this to the influence of two-invoice system, which dragged the revenue growth with limited effect on profit. The gross profit margin and operating profit margin both improved for distribution segment (+0.09ppts/ +0.12ppts). The company's sales network directly covers 24 provinces and cities in China and 27,712 medical institutions (including 1,425 Class III hospitals and 727 CDCs). Meanwhile, Shanghai Pharma continues to expand the hospital supply chain innovation services, with SPD business added 27 contracted hospitals, 162 co-hosted hospital pharmacy and 48 medical institutions co-pharmacy in first half. We see the income from hospitals accounting for 60.62% of pure sales. Its retail business also develops quickly owning 1,855 chained pharmacies in 16 provinces with Shanghai Huashi Pharmacy being one of the retailers with the largest number of pharmacies in East China.

Manufacturing business grew quickly. The manufacturing business posted revenue of RMB11.15bn as up to 9M17 with YoY growth of 18.7%, while net profit recorded YoY growth 15.51%. We attribute this to sales hike of core products and we see both GPM and OPM increased (+1.16ppts/+0.77ppts) for manufacturing segment. The company now produces over 800 kinds of drugs and 20 kinds of dosage forms, mainly focusing on digestion and metabolism, cardiovascular and cerebrovascular, whole body anti infection, mental nerve and anti-tumor. We expect the manufacturing business to maintain quick growth as the company adheres to focus on key products and to strengthen the academic marketing-oriented strategy. Sixty key products reported sales of RMB5.86bn (+12.16% YoY) making up 56.32% of segment turnover (55.64% in 9M17) with a better GPM 70.6% (+1.62ppts). We expect 26 key products to achieve more than 100mn sales in 17E.

Pipeline progresses. In 3Q17, the application of Class I innovative drugs – “SPH3348 active pharmaceutical ingredients and its tablet” was approved for clinical trials. Class I new biological products for treatment purpose –“recombinant anti HER2 humanized monoclonal antibody composition” used for injection purpose obtained clinical approval. We see that Shanghai Pharma attaches importance to R&D and has established cooperative relationships with many research institutions. In first half, R&D expenses accounted for 4.97% of manufacturing segment turnover. We expect further progresses made in future.

Investment Thesis, Valuation & Risk

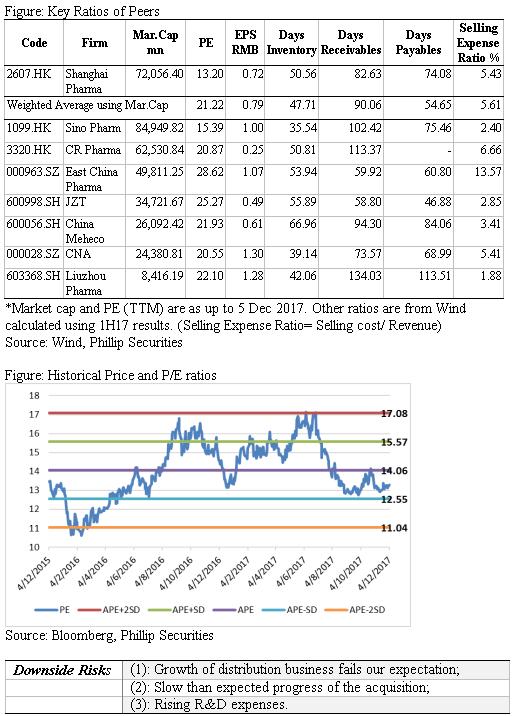

Our valuation model suggests a target price of HK$25.2. The company enjoys lower PE ratio (13.2x) than peers (industry average: 21.22), with better operational indicators and lower selling expense ratio. We predict that the net profit growth in 17E/18E to be 11.5%/16.6% (considering Cardinal effect on 2018 results), and give the target price of HKD25.2 assuming PE 14x.

Financials

Click Here for PDF format...