Summary of Investment

-Efforts will be made in the fourth quarter, and thus high result growth of the year can be expected;

-The risk of acquisition falling short of expectations has basically been released;

-The management has held more shares, showing their confidence;

Investment Rating

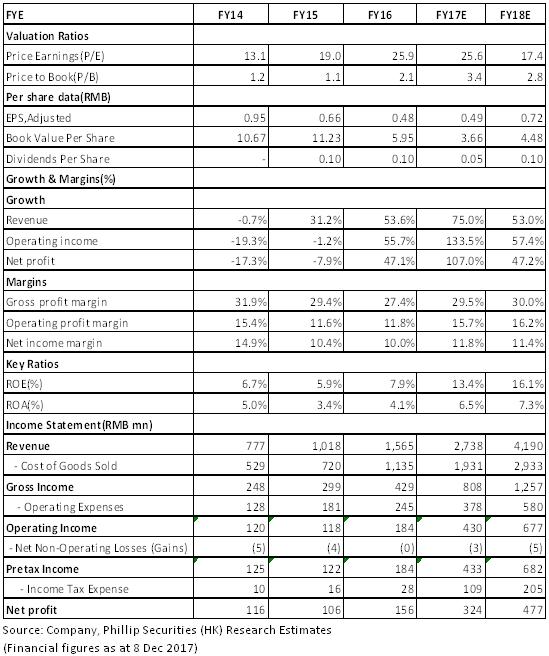

In general, we are optimistic to the prospect of soil remediation market. Beijing GeoEnviron Engineering & Technology has strong overall strength in the soil remediation field, and at the same time, has accelerated its layouts in the dangerous wastes disposal and garbage burning fields, bringing sufficient momentum for continuous result growth. A few days ago, after the Company resumed trading by terminating its purchasing Shenzhen Shentou Environmental Technology Co, Ltd., the risk of falling short of expectations has been released to a large extent, and the controlling shareholders, supervisors and senior executives successively held more shares to show to the market their confidence in the long-term development of the company. We expect the company's 2017-2018 net profit attributable to the parent company to reach RMB324million/RMB477million, respectively; the corresponding EPS to be RMB0.49/0.72 respectively; the corresponding PE to be 25.6/17.4 times, respectively; the given target price to be RMB18.00, rated Buy. (Closing price as at 8 Dec 2017)

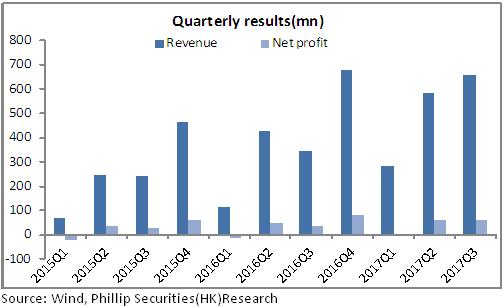

High Result Growth in the First Three Quarters

In the first three quarters of 2017, the revenue of Beijing GeoEnviron Engineering & Technology reached RMB1.52 billion, up by 71.19% yoy, and the net profit of returns attributable to the parent company was RMB129 million, up by 71.89% yoy and up by 73.96% excluding non-recurring items, equivalent to an EPS of RMB0.195, up by 68% yoy. The rapid revenue and profit growths mainly originate from the increase of the quantities of construction projects and the 30% yoy increase of the profits in the consolidated financial statement and from investment and acquisition.

Fee management and returns on investment have driven the net profit to increase

The overall fee control by the Company is in a good state, but the financial expense has greatly increased. In the first three quarters, the period cost rate decreased by 1.34 ppts yoy. Specifically, the sales expense rate was 2.84%, down by 0.92% yoy, the administration expense rate was 9.84%, down by 2.13% yoy, and the financial expense rate was 3.95%, up by 1.71% yoy, mainly due to the increased interest expense led by the increase of bank loans.

Fee management and returns on investment have driven the net profit to increase greatly. The gross margin and net profit were 27.84% and 10.67%, respectively, up by 0.94% and 2.32% yoy, respectively. By virtue of the Company's enhancing the collection of accounts receivable, the net operating cash flow of the first three quarters were -RMB72.85 million, up to some extent yoy.

In June 2017, the Company issued a plan that it would non-publiclyissue RMB1.2 billion of green bonds and RMB0.84 billion of convertible bonds. Up to now, the convertible bonds have been accepted by the China Securities Regulatory Commission (CSRC), and the expected multi-channel financing will effectively boost the capital strength and accelerate the Company's project acquisition and implementation.

The number of environmental restoration orders decrease compared with the last year

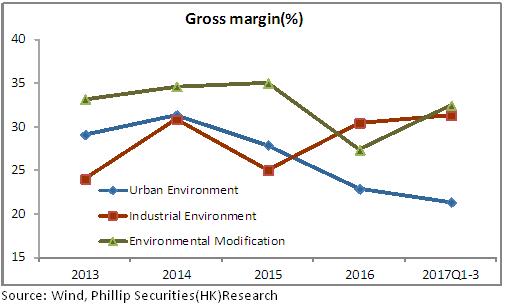

Up to now, the amount of orders is RMB2,293 million, including RMB586 million of environmental modification, RMB1161 million of industry environment and RMB546million of urban environment. At present, the amount of order in hand is RMB9,329 million, of which RMB1,756 million have been executed and RMB7,576 million have not. There are adequate orders to be executed.

Compared with 2016, the Company's orders increased at an obviously lower speed this year. The environmental modification and urban environment orders greatly reduced, except the industry environment orders greatly increased. This is mainly caused by these two facts: The industrial policy has been implemented at a speed lower than expected, and the industrial orders have been released at a lower speed.

The soil remediation market is about to surge

The soil remediation industry is still in the starting stage in China, and relevant law and standard systems haven`t been completed yet. In May 2016, with the issuance of the Action Plan for Soil Pollution Prevention and Control (hereinafter referred to as "the Ten-Chapter Plan"), the soil pollution control market was started. In June 2017, Public opinions were sought for the Soil Pollution Prevention Law (draft), which is expected to be issued in 2018. Moreover, relevant technical rules and management methods will also be released in succession. With the deep implementation of "the Ten-Chapter Plan" and the gradual completion and release of relevant regulation systems, the room in the soil remediation market will be gradually released.

According to market estimations, the room of cultivated lands, industrial lands and mineral areas in the soil remediation market will reach RMB1 trillion in ten years, indicating a significant market prospect. We hold that in the long run, advanced soil remediation techniques and strong capital strength will become the cores of corporate competitiveness in the industry. Beijing GeoEnviron Engineering & Technology ranks front with regard to the soil remediation technology, project experience and capital strength, and with the gradual release of soil remediation market, the Company will benefit from the prominent pre-emptive advantage.

Risk Warnings

Risk of the advancement of industrial policies falling short of expectations;

Risk of market competition intensification;

Risk of the acquisition of orders falling short of expectations;

Risk of insufficient capital;

Financials

Click Here for PDF format...