Investment Summary

- 15% Increase in Profit of 2017Q3

- Remarkable Effects of Capacity-Control and Price-First Strategies

- It will be helpful to benefit from the economic recovery in Europe to operate jointly with Lufthansa

Valuation & Investment thesis

According to the latest result, we revised our estimate 2017/2018 net profit of AC to be 9.68/9.55 billion RMB; EPS to be 0.67/0.66-yuan RMB. The target price is adjusted to HKD8.67, estimates 11x/11x P/E and 1.45/1.31x P/B in 2017/2018. “Accumulate” rating is given.

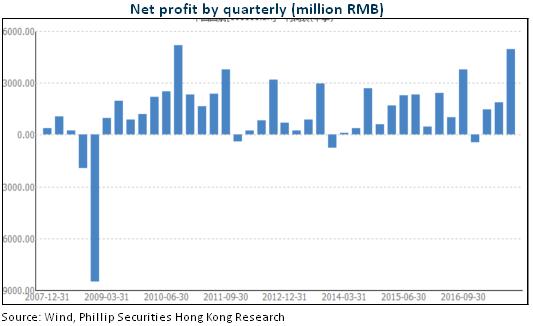

15% Increase in Profit of First Three Quarters of 2017

According to AC's report of the first three quarters (Chinese Accounting Standards), it recorded a revenue of RMB92,996 million for the first nine months of 2017, with yoy growth of more than 8.8%. The net profit attributable to the parent company was increased by 14.6% to RMB8.28 billion, with a basic EPS at RMB0.62. AC's EPS in Q1, Q2 and Q3 was RMB0.10, RMB0.13, RMB0.34, respectively, reduced by 47%, rocketed by 63% and increased by 17% yoy, respectively, from last year's RMB0.19, RMB0.08, RMB0.29, respectively. The faster growth of revenue in comparison with operating cost and the substantial savings in financial costs for the appreciation of RMB were the main causes for result growth.

AC's financial cost of the first three quarters was only RMB66.34 million due to exchange gains, down by 99.6% Y-o-Y, which was the largest drop in the three major airlines. AC's net profit slightly slipped by 3.6% to RMB6.81 billion in 2016, which were lower than our estimate of 23%. Limited by the bottleneck of Capital International Airport, this was mainly due to lower-than-expected revenue growth and higher-than-expected financial expense as well as income tax rates.

Remarkable Effects of Capacity-Control and Price-First Strategies

AC implemented cautious capacity-control and price-first strategies, with both its P L /F and profitability increased, and maintained its leading position in the three major airlines.

In the H1 of the year, AC had a net increase of five aircraft. Accelerating the introduction of capacity in the H2 of the year, there was a net increase of 15 aircraft in Q3. The fleet currently has 643 aircraft, including 253 aircraft owned by itself, 185 aircraft in the form of finance leases and 205 aircraft in the form of operating leases. According to the plan, there will be a net increase of 18 aircraft in Q4. From 2018 to 2019, the company has a plan of a net increase of 33 and 41 aircraft, with Boeing 737 and Airbus A320/321 as main models.

In the first three quarters, the company's capacity and volume increased by 5.5% and 5.1%, respectively. The growth rate was slower than that of CEA and CSA. Its P L /F increased to by 0.3 ppts to 81.2%, wherein the international routes maintained stable, and domestic and regional routes were improved. RPK rose by 1.43% in the H1 of year and rose by 5.2% in Q3. The company continued to promote the construction of hubs around Beijing, Shanghai, Chengdu and Shenzhen, optimized the price gradient of two domestic cabins (first-class cabin and business class cabin) and expanded customers` breadth of two international cabins. As a result, this gave rise to significant increase in the overall revenue level of two cabins and revenue proportion.

It will be helpful to benefit from the economic recovery in Europe to operate jointly with Lufthansa

In the H1 of 2017, AC announced the official joint operation with Lufthansa AG. Both parties will enhance the service level in China-Europe routes and overall competitiveness in the European market by coordinating flight schedules, implementing plans of joint major clients and further optimizing flight plans of frequent passengers. Both parties will adopt unified pricing on the joint venture routes, and then determine the income ratio according to the number of seats and models that they have invested in. This is a more in-depth cooperation mode in comparison with code sharing. After the affiliation, it will be convenient for AC's passengers to make use of aviation hubs in Frankfurt, Munich, Zurich and Vienna for a round-trip ride.

For AC, this will directly complement the airline network between European hub market and domestic second-tier cities, strengthen flight densities between European airline hub and domestic first-tier cities, enhance International airline passengers` experience and stickiness, as well as enabling AC to have a higher fare-increase flexibility in peak seasons. We hold the view that the European aeronautical market is moving away from the terrorist attacks and will benefit from the demand-improving effects brought by European economic recovery.

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast.

War, terrorist attacks, SARS and other emergencies;

Highspeed railway diversion

Financials

Click Here for PDF format...