Investment Summary

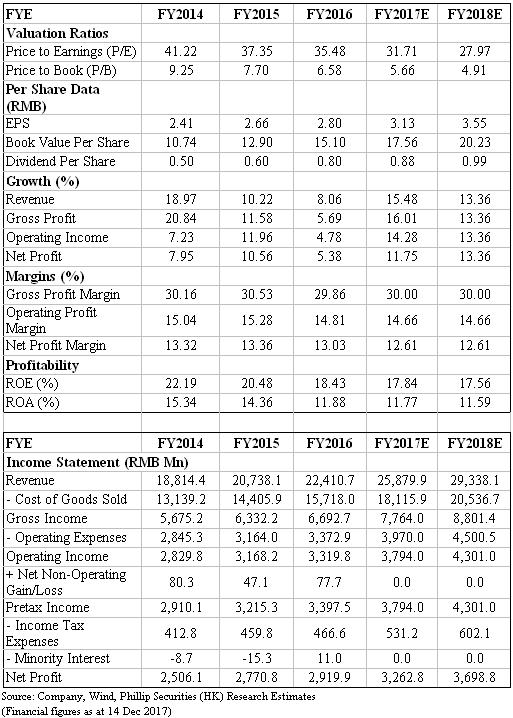

Yunnan Baiyao is a pharmaceutical firm engaged in R&D, producing and distribution. Baiyao, developed in 1902, is a famous anti-infective and hematostatic traditional Chinese medicine (TCM). The Baiyao formula is a state-level secret with a strong customer base and high brand awareness. Recent years, the company based on Baiyao series develops other medicines, cosmetic products and nourishing healthcare products, as well as exploits distribution business. The company recorded FY07-16 revenue/net profit CAGR of 20%/27%, and we expect it to maintain relatively high growth with EPS RMB3.13/3.55 in 17E/18E. Assuming PE 33x (roughly par to 2y historical average plus 1.5x standard deviation), we initiate TP of RMB117.7 with 18.5% upside, `Accumulate` recommendation. (Closing price at 14 Dec 2017)

Business Overview

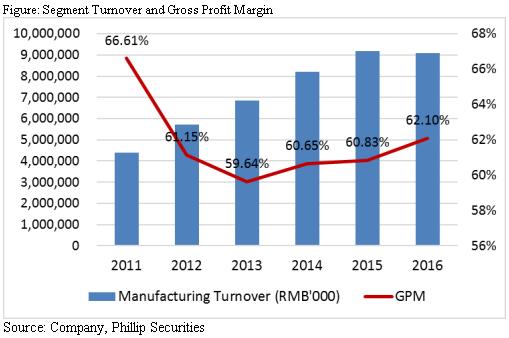

Bright Outlook of Manufacturing Sector

With Baiyao series as cornerstone, the company keeps exploring great healthcare industry involving Western and Chinese medicines and raw materials, personal healthcare products, TCM, etc. The company now owns 40 production lines producing over 19 formulas and 390 products. The manufacturing sector delivered FY11-16 revenue CAGR of 15.68% with 61.8% average gross profit margin (GPM). In 1H17, manufacturing sector recorded sales RMB4.97bn (42% of topline) with 9.5% YoY growth and 66% GPM (+4.79ppts, 1H16: 61.23%).

(1) Medicine segment. Medicine segment reported RMB4.98bn sales (22% in topline) in 2016. Three main products, namely Yunnan Baiyao band-aid, aerosol preparation and ointment, were ranked NO.1 in terms of sales volume among peers in PRC market. Sales of another main product Qinxuekang oral solution also grew fast in 2016. In future, the company will strengthen promotion of key products, select and nurture around 10 special products of great market potential as future growth momentums. We estimate this sector to remain 3% YoY growth in 17E/18E.

(2) Healthcare product segment. This segment reported 2016 sales RMB3.76bn (17% in topline) with FY11-16 CAGR over 25%, involving products like toothpaste, shampoo, and sanitary towels. The Yunnan Baiyao Toothpaste makes up 16.5% national toothpaste market, ranking at NO.1 among native brands. To further expand client base, the company launched new toothpaste products for kids and pregnant women in 2016. For shampoo products, we see continuous sales growth of Yangyuanqing series and new series like Taomishui, Essential Oil launched in 2016. This year leveraging on the influence of hot IP like `三生三世,十裡桃花`, the company launches related products to attract more young customers. Meanwhile, we see sanitary towel sales continues to climb. In addition to existing Rizi series, the company starts to exploit middle and high end market with new brands such as Feiyang and Xinanshu. Besides traditional channels like supermarkets, Yunnan Baiyao's healthcare products are also distributed through online flagship shops on mainstream platforms. The company sets up Internet promotion center in Hangzhou city in order to accelerate business development under E-commerce environment. We predict this segment to quickly grow at 15% YoY in 17E/18E, given the strong brand image of Yunnan Baiyao and intensifying distribution network under the consumption upgrade trend.

(3) TCM resource segment. TCM segment reported RMB944mn sales (4.2% in topline) in 2016 with FY13-16 CAGR of 39.7%. The natural geographical environment and climate bring Yunnan the unique advantage of biological resources with most plants species among Chinese provinces. Given its advantages in TCM industry, the company has built planting bases of Chinese medical materials through strategic cooperation or JV. Meanwhile, it explores offline channel in Yunnan through providing consumers with precisely customized TCM products and healthcare services. We project this segment to grow at 30% YoY in 17E/18E given the relatively small base.

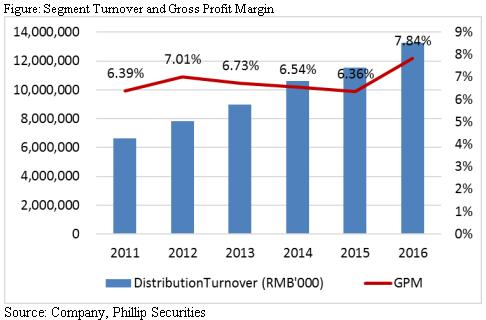

Distribution Sector Rapidly Growing

We see distribution sector grew at CAGR 14.8% during FY11-16 with average GPM of 6.81%. In 1H17, distribution business recorded RMB6.92bn revenue (58% in topline) with 17.5% YoY growth and 7.07% GPM (+1.06ppts, 1H16: 6.01%). Yunnan Baiyao is a regional distribution leader with three main subsidiaries as distribution platform (namely Yunnan Pharmaceutical Company, Yunnan Baiyao Pharmacy and one E-commerce company). For the traditional offline channel, the company has covered all main medical institutions in PRC and all hospitals above county level within Yunnan Province. At the same time, the company continues to enhance e-commerce business through cooperation with Tmall, Taobao, JD, Wechat, etc. In future, the company will provide more customized service to hospitals of county and above levels and boost businesses of retail pharmacy chains, hospital pharmacy trusteeship and online shops. We expect the distribution sector to grow at 15% in 17E/18E.

Composite Ownership Reform Underpins Growth at New Stage

Currently, Yunnan Baiyao Holdings Limited (YBH) controls 41.52% of the listing company shares. YBH was wholly-owned by the State-owned Asset Supervision and Administration Commission (SASAC) of Yunnan Provincial Government. After composite ownership reforms, YBH is now owned by SASAC, New Huadu and Jiangsu Yuyue (45%, 45%, 10%). The stake reorganization not only introduces abundant cash (c.RMB30bn) into YBH, but also helps to build up market-oriented governance structure, under which all the directors, supervisors and management team are appointed according to marketization principal, with no one enjoying politically administrative titles. In terms of the strategic investor, Jiangsu Yuyue, controlling listed firms i.e. Yuyue Medical (002223.SZ), Wandong Medical (600055.SH), is a leading private enterprise in fields of medical image and household healthcare. After Jiangsu Yuyue participated in Wandong Medical's reform in 2014, Wandong in 2016 realized net profit of RMB71.54mn, which was nearly three times to 2014 NP. In future, we expect that market-oriented decision making system and synergies with its strategic investors can serve as new growth momentums.

Improved Compensation to Management Team

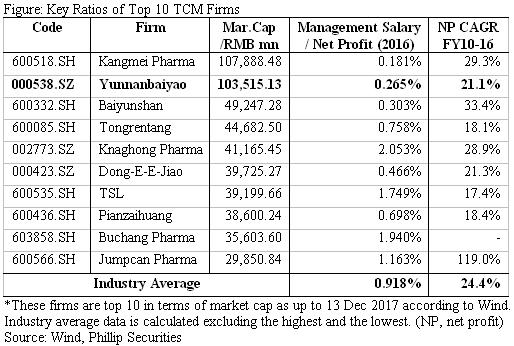

We see the compensation to management kept below average level in past. The management salary in 2016 totaled RMB7.74mn making up only 0.265% of net profit attributable to shareholders, while the industry average was around 0.92%. In November 2017, the board of directors approved two reform schemes about compensation to management and independent directors (which specified that annual allowance for per independent director should amount to RMB 216,000 after tax). We estimate that the current compensation is around industry average, and we expect that the incentive plan can encourage the management to work more proactively for better operation results.

Policy Tailwinds

According to PRC National Bureau of Statistics, the TCM market turnover recorded 20.59% CAGR during 2006 to 2016. In 2016 Aug, the State Administration of TCM made the Thirteenth Five-Year Plan for TCM Development, in which it expected the manufacturing industry turnover to be RMB1252.3bn in 2020, implying 15% CAGR. Therefore, we see still quite room for the development of TCM business. Meanwhile, the further rollout of two-invoice system is expected to increase concentration of distribution industry. We predict that Yunnan Baiyao as a regional leader should benefit from the policy and further enhance network through accretive M&A or other cooperation.

Investment Thesis, Valuation & Risk

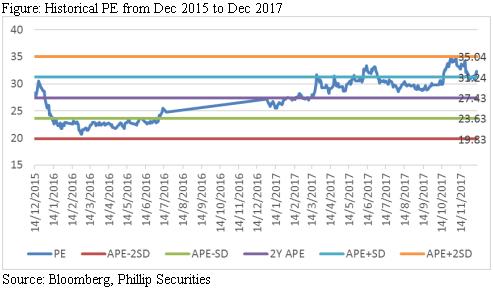

We initiate target price of RMB117.7. We project the sales growth of mentioned four segments to be 3%/15%/30%/15% in both 17E and 18E, thus derive 17E/18E EPS of RMB3.13/3.55, assuming relatively stable profit margins. Given PE 33x (roughly par to 2y historical average plus 1.5x standard deviation), we give TP RMB117.7 with 18.5% upside, `Accumulate` recommendation.

Risk:

Rising price of raw materials;

Sales growth fails expectation;

Policy risks.

Financials

Click Here for PDF format...