Investment Summary

Anta Sports is a leading sportswear company in PRC market. We expect the company to experience high growth in future, considering: 1) Growing sports industry may benefit from national development plan and consumption upgrade trend; 2) Multi-Brand and Omni-Channel strategy contributes to future growth; 3) Outstanding operation efficiency and excellent management. We predict sales growth rate to be 21%/25% in 17E/18E, assuming PE 22.93x (par to 2y historical average plus 0.5x SD) to derive TP HKD36.6. With 15.3% upside, we initiate `Accumulate` recommendation and suggest buying on price dips. (Closing price at 20 Dec 2017)

Business Overview

According to public data of Chinese listing firms focusing on sportswear, Anta is ranked at the first in terms of sales volume. The company is engaged in developing, producing and distributing of sportswear products in PRC market. Anta achieved revenue/net profit CAGR 17.27%/18% since listed in 2007. Its 2016 revenue amounted to RMB13.35bn, 52% of which came from apparels while 45% from footwear products. In light of its core strategy `Single-Focus, Multi-Brand and Omni-Channel`, the company caters to different types of consumers with multiple brands and continues to expand promotion and distribution channels. We see that the company revenue grew more rapidly than peer companies during recent years and continues to improve operation efficiency.

Multiple brands to cover more consumers

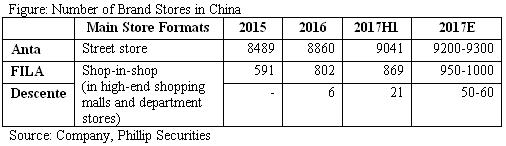

The company insists `Multi-Brand` strategy to broaden customer base with different brands to meet different client demands. The company's brand portfolio reaches consumer segments across groups of different age, covering mass and high-end markets and providing functional and fashionable casual sportswear. As up to the end of June, the company operates 9,041 Anta shops, 869 FILA shops and 21 Descente shops in China.

(1) Anta & Anta Kinds.

Anta brand provides functional sportswear products for running, crossing-training, basketball and soccer. The brand caters specifically for lower- and middle-income groups with average selling price of RMB200-500. Anta brand stores are mainly street stores located in second and third tier cities, but we also see increasing retail network presence in shopping malls and department stores. From 2008, the company started to provide sportswear products for kids aged from 0 to 14 years old, which are priced as low as RMB79. Given low concentration of children clothing market and the introduction of two-child policy, we expect the company to benefit from accelerated growth of children clothing market, leveraging on its strong brand image and wide street-store coverage.

(2) FILA & FILA Kids.

FILA brand provides a series of high-end and stylish sportswear products. This brand was acquired in 2009 from Belle and expanded rapidly from 200 stores to 869 stores until 1H17. FILA stores are mainly located in high-end shopping malls and department stores in first and second tier cities targeting at high-income consumers. The famous Chinese celebrity Gao Yuanyuan was featured in FILA advertising campaigns. FILA Kids was built in 2015 offering high-end apparel and footwear products for children aged 7 to 12. With more new FILA stores launched, we expect the brand to continue growth trajectory, given gradual recovery of macro economy and future consumption upgrade trend.

(3) Descente.

In 2016, the company introduced the brand through forming a joint venture (JV) with Japanese Descente firm. The brand produces professional outdoor products related to skiing, cross-training and running, especially featured in ski suits. Currently Anta operates 21 Descente stores in main first and second cities and builds up a membership system to increase the customer loyalty. Given the 2022 Winter Olympics will be held in Beijing, the Chinese government plans to promote winter sports and promises that the number of people participating in winter sports will increase to 300mn. We highlight that the company actively exploit this segment market which helps to further enrich product lines and widen client coverage.

(4) Other brands.

In 2016 the company acquired an English brand Sprandi which mainly offers leisure footwear products. This year, the company cooperates with Kolon to set up a JV to produce leisure outdoor products, and acquires a Hong Kong children clothing brand KingKow (小笑牛). We expect these new brands to contribute to revenue in future.

We expect, by the end of 2017, the total number of Anta brand stores to reach 9,200 to 9,300 and FILA to reach 950 to 1,000. Meanwhile, given Descente brand will enter into more first and second tier cities, we expect 50 to 60 Descente stores in China by the end of 2017.

Omni-Channel Development

With the retail-oriented strategy, the company continues to enhance retail management and boost online distribution. Its promotion and distribution channels involve street stores, shopping malls, department stores, outlet stores and e-commerce platforms. The company makes store-opening strategy according to characteristics of different client groups: Anta brand focuses on street stores in tier 2 and 3 cities in order to adapt to shopping habits of middle- and low-income customers; FILA and Descente stores are located in big shopping malls and department stores in tier 1 and 2 cities to access high-end buyers; Online platforms and Outlets serve as centers to clear aging inventory. Meanwhile, the company places importance on boosting online sales channel, which distributes in-season products, off-season products and online exclusive products from company brands. We highlight that product launch schedules, priorities and styles of e-commerce platforms are standardized to facilitate synergy between online and offline retailers, which also helps to prevent their negative competition.

Excellent Supply Chain Management

The efficient supply chain management is emphasized across the whole business chain. It takes 13 months from product design to sales. The company combines in-house and outsourced production (including OEM and ODM models) in order to better respond to market conditions and changes in consumer preferences. In 2016, in-house production percentages for apparels and footwear are respectively 42.9% and 16.7%. The company holds trade fairs four times a year and properly arranges production according to trade fair orders. It enhances the replenishment order system to increase proportion of replenishment orders except for the trade fair orders, to further improve products` ability in meeting consumer demands and to optimize inventory levels. The company will first complete c.80% of main product orders and then efficiently arrange rest (c.20%) production progress in response to sales conditions. The company progresses improvement of logistic system. A new logistic center will be into operation in early 2018, which will enable delivery period cut from one month to as short as 48 hours. We believe the logistic center will underpin future fast growth of all channels, from wholesale to retail and from online to offline.

Rapid Sales Growth and Outstanding Efficiency

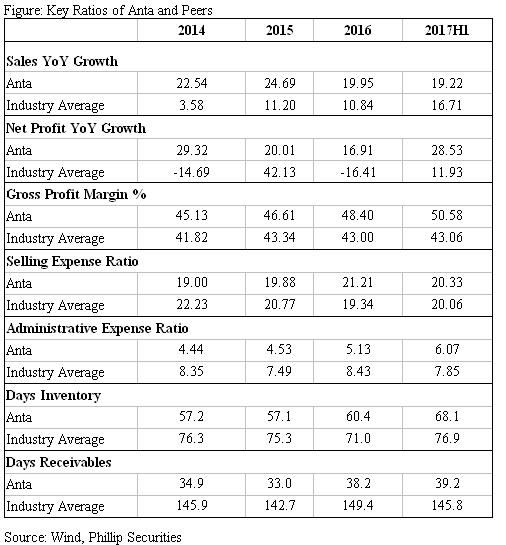

The company achieved revenue/net profit CAGR of 17.27%/18% since listed in 2007. We select four peer companies to clarify Anta's competitiveness, namely Li Ning 2331.HK, Guirenniao 603555.SH, XTEP 1368.HK and 361 Degrees 1361.HK. From the table below, we see that Anta reported higher than average growth in terms of revenue and net profit with expanding profit margin, i.e. in 1H17 Anta recorded GPM 50.58% better than industry average 43.06%. We see increasing trend of selling expenses in past three years but selling cost to revenue ratio declined in 1H17, attributable to decreasing advertising cost ratio (1H16 11.2%, 1H17 9.3%). We highlight good control of administrative fees (6.07% in 1H17 revenue) which is lower than average cost level (7.85% in revenue). According to 2017 interim results, the inventory level is rational with shorter inventory turnover period (Anta 68 days vs average 76.9 days). Stable and shorter than average receivables turnover period indicates Anta's strong ability to collect cash (Anta 39.2 days vs average 145.8 days). Besides, we highlight the company efforts to strengthen R&D capability with rising R&D cost to sales ratio (1H16 4.4%, 1H17 5.8%).�

Growing Sports Industry

With further urbanization progress and improving education level of residents, we see rising residents` health awareness and more people starting to form fitness habits. According to NBS data about China's cultural, educational and sports goods manufacturing industry, the industry posted revenue RMB 1.7 trillion in 2016, with FY06-16 turnover CAGR of 26% and profit CAGR of 33.3% (implying industry profit margin 4.93%). In May 2016, the State Sports General Administration issued the 13th Five-Year Development Plan for Sports Industry. It is said that by 2020, the turnover of national sports industry would total more than RMB 3 trillion and make up 1% of GDP with faster growth speed than GDP. Thus we roughly estimate that there is still quite room for China sports goods industry to develop.

Investment Valuation

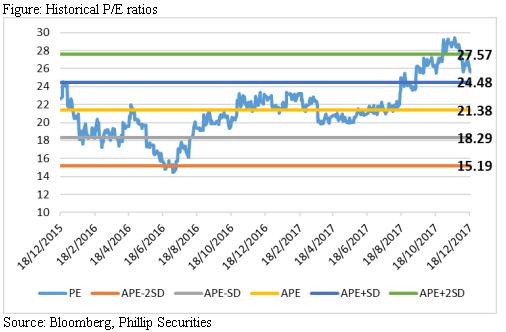

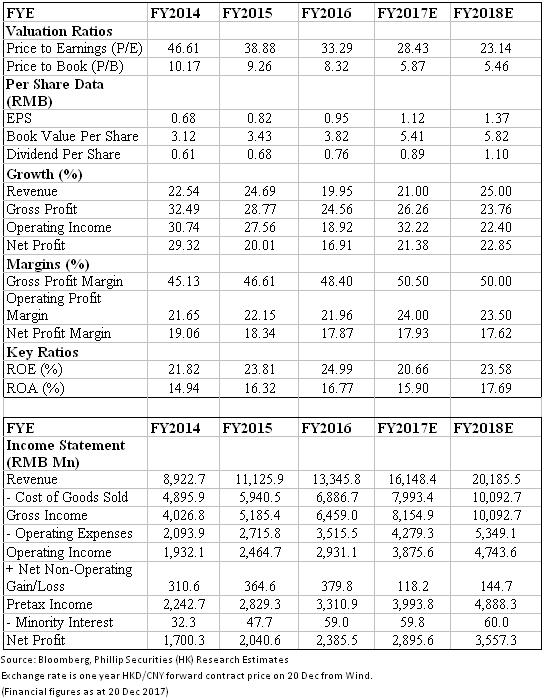

We predict sales growth rates to be 21%/25% in 17E/18E. Assuming PE 22.93x (par to 2y historical average plus 0.5x standard deviation), we give target price of HKD36.6. With 15.3% upside, we initiate `Accumulate` recommendation and suggest buying on price dips.

Risk

New brands sales fail expectation;

Fierce competition in sportswear markets;

New stores are launched slower than expected;

Depressed macro economy.

Financials

Click Here for PDF format...