Summary of Investment

-Favorable industry policy, good market prospects and strong capacity of business expansion;

-Abundant reserve of projects and continuously growing business;

Investment Rating

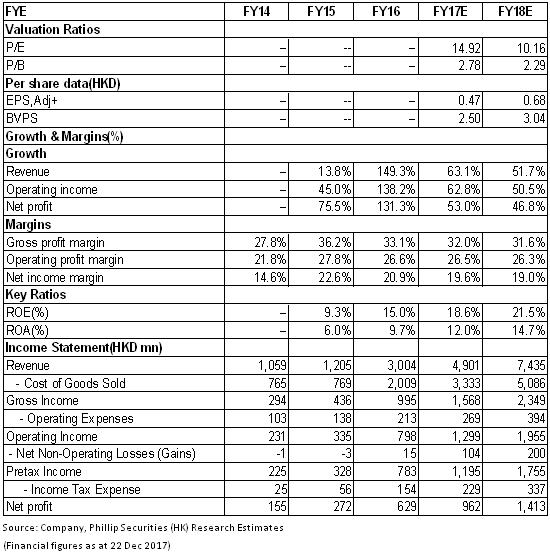

Based on the favorable policy environment, abundant reserve of projects, sustained growth momentum that drives results and high margin of safety in valuations, we expect that the net profits attributable to the parent company for 2017-2018 will reach HKD962 million and HKD1413 million, respectively; EPS will be HKD 0.47/0.68, equivalent to a PE of 14.8/10.2. The target price is expected to be RMB8.84 and the rating is "Buy" for the first coverage. (Closing price as at 22 Dec 2017)

Strong Momentum in Result Growth

Everbright Greentech was listed on the stock market in May 2017 separated from the parent company Everbright International. Its main business includes comprehensive utilization of biomass and hazardous waste disposal. Besides, there are still a small number of photovoltaic and wind power projects.

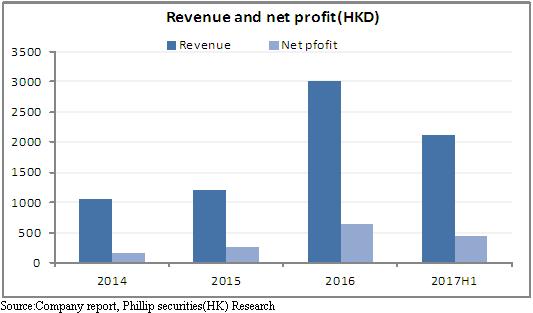

In H1, the company recorded an income of HK$2.047 billion, up 69% YoY. EBITDA was HK$713 million, soared 60% YoY, and the profit attributable to shareholders stood at HK$457 million, up 57% YoY. EPS was equivalent to 28.23 cents, up 39.2% YoY.

Biomass contributed most of its results with fast growth. Biomass recorded the profit of HK$342 million, up 104% YoY, accounting for 74.8%; the profit of hazardous waste disposal was RMB90.7 million, increased 29% YoY; the profit of photovoltaic and wind power projects was RMB585,210,00, basically flat compared to the same period in last year mainly due to the lack of new projects in the period.

The gross margin was 32.26%, down by 3pct YoY. The main reason is that the construction revenue with low gross margin has been increased, and the new biomass project is in breaking-in period, which has dragged down the overall gross margin. The net profit margin was 21.85%, down by 1.86 YoY.

The company is financially sound and rich in cash. As of H1, the company's cash on the book was HK$3.89 billion; unused loan limit was HK$3.903 billion; asset-liability ratio was 35% and mobility ratio was 3.36. The sound financial structure and abundant funds provide fund guarantee for accelerating project implementation.

Biomass Power Generation Business Shows Great Growth Potential

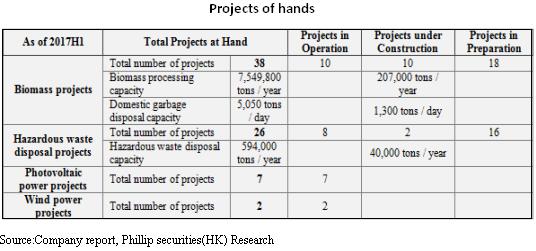

As of H1, the company had 38 biomass projects, with a total installed capacity of 867 MW, an increase of 251 MW compared with the end of 2016. The market share of the company topped the industry. The company developed the unique business mode of the integration of biomass and rural domestic waste, which could effectively reduce the overall development and operating costs and enhance the competitive advantage in business expansion.

According to the 13th Five-Year Plan, by 2020 the cumulative biomass power installed capacity will reach 15,000 MW. By the end of 2016, however, the total installed capacity was only 6,692 MW. It is expected that the CAGR will reach 17% in the next few years. The biomass resources available in China are abundant, but the utilization rate is low. Biomass power generation is still in the initial stage of development. Benefiting from the promotion of favorable policy and the demand for air pollution control, the biomass power generation industry will usher in the golden period of development. The company has an integrated advantage and rich operating experience in the field of biomass. It is expected to speed up the acquisition of the project and expand the market share.

Excellent Qualification of the Hazardous Waste Disposal Capacity

As of H1, the company had 26 hazardous waste disposal projects, with total disposal capacity of 594,000 tons. At present, it can dispose 42 items of the 46 categories of hazardous wastes listed in the National Hazardous Wastes Catalogue, and mainly disposes hazardous wastes in a harmless way. The company has carried out strategic layout for the Eastern China with the largest out of waste disposal, and has a leading position in the hazardous waste disposal capacity in the industry.

At present, China's hazardous waste disposal capacity is not strong, effective capacity is not enough, and market concentration is not high. It is expected that, between 2017 and 2021, the CAGR of hazardous waste industry will reach 11.7%, of which the CAGR of the resource utilization will reach 10.0%, and the CAGR of harmless disposal will reach 15.7%. Benefiting from the strictness of environmental standards and the rapid growth of the disposal demand, the hazardous waste industry will have a good prospect in the future. At present, the company has secured fewer hazardous waste projects. With the continuous expansion of the company's hazardous waste capacity and the acceleration of the project implementation, the result contribution of the company is expected to be further improved.

Actively Planning the Layout of Soil Remediation Industry

In the period, the company established the environmental remediation and management center, and will enter the fields such as soil remediation and the pollution control of volatile organic compounds (VOC). The soil remediation industry is still young in China and the trillion markets will soon be started. The active layout of the soil remediation industry is expected to bring new growth opportunities to the result of the company.

Risk Warnings

Industry policy risk;

The acquisition and implementation progress of projects falls below expectations;

Risk of intensified market competition;

Financials

Click Here for PDF format...