Investment Summary:

-Soar of 18% in the Earnings of the First 3 Quarters

-The exchange earnings and investment income contribute to the growth of profit

-The introduction of ASK is faster than its peers

-The pioneer implementing SOE mixed reform in civil aviation

Soar of 66% in Q1 Earnings

China Eastern Airlines (CEA) recently released the Q1 report in the 2016 fiscal year. During the period, the total revenues increased by 5% over last year to RMB23.53 billion. The attributable net profit soared by 66.4% over last year to RMB2.6 billion, and EPS stood at RMB0.2. Downturn in oil prices, favorable RMB exchange rate and steady growth in demand contributed to the remarkable Q1 result.

Investment Thesis

We expect the company's 2017/2018 net profit to be RMB6.5/6.7 billion, equivalent to EPS of RMB0.45/0.47.

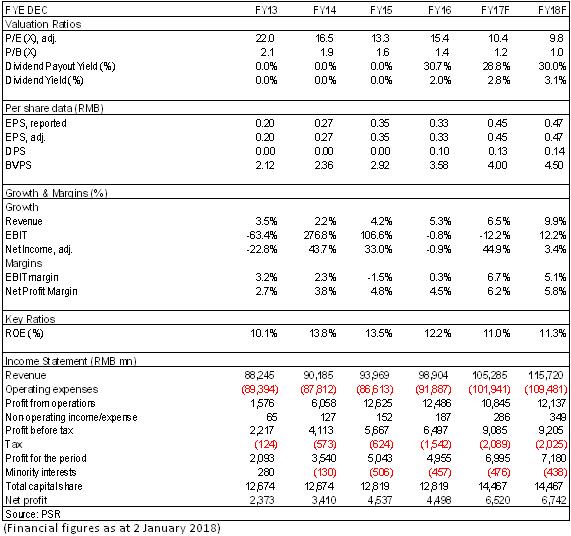

Given that possible improvement on efficiency after the mix reform, and the expected better ticket price in the future, we are optimistic about the Company's future result flexibility. Therefore, we keep the target price unchanged at HK$6.36, equivalent to 11.7X/11.1X estimated P/E in 2017/2018. Also, the "Accumulate" rating is given. (Closing price as at 2 Jan 2018)

Soar of 18% in the Earnings of the First 3 Quarters

According to China Eastern` report of the first three quarters (Chinese Accounting Standards) in 2017, it recorded a revenue of RMB77.5 billion for the first three quarters, with slight yoy growth of 2.8%. The net profit attributable to the parent company was increased by 18% to RMB7.92 billion, ranking the first among the top three airlines. With the basic EPS of RMB0.55, China Eastern` EPS in Q1, Q2 and Q3 was RMB0.19, RMB0.11, RMB0.25, respectively, reduced by 5%, rocketed by 175% and increased by 4% yoy, respectively, from last year's RMB0.2, RMB0.04, RMB0.24, respectively.

The exchange earnings and investment income contribute to the growth of profit

Benefiting from the appreciation of RMB exchange rate, the exchange earnings were RMB1.3 billion. But last year, the exchange loss was RMB1.77 billion due to the depreciation of RMB, and therefore the financial cost in the first three quarters was decreased by 72% to RMB1.1 billion. In addition, RMB1.754 billion also contributed to the rapid growth of the final result as a result of the disposal of China Eastern's logistics equity.

The introduction of ASK is faster than its peers

CEA ranks the first among the top three airlines in introducing ASK. In the first ten months of this year, ASK increased by 9.5% yoy, whose growth is faster than that of RPK's yoy growth 9%. The slightly massive supply causes the P L /F to fall by 0.4 ppts to 81.3%. Due to the penalty imposed on Shanghai Base, the summer weather, the high base of the same period and other factors, the problem of mismatch between supply and demand became more prominent on the international routes, with the P L /F of international routes declining by 2.3 ppts.

The fleet currently has a net increase of 611 from 30 at the end of 2016, including 248 aircraft owned by itself, 224 aircraft in the form of finance lease, and 139 aircraft in the form of operating leases. According to the plan, there will be a net increase of 25 aircraft at the end of this year, and 52 aircraft by 2018. The continuous and rapid expansion of ASK makes the company's P L /F under pressure, but the company has accelerated the renewal of old aircraft, making the average age of the fleet keep only 5.5 years, superior to its peers.

The pioneer implementing SOE mixed reform in civil aviation

In September 2016, China Eastern Airlines Group became one of the six central SOE's to promote the pilot reform. In this round of reform, it is in the leading position in the mixed reform among central enterprises. Early in 2015, CEA carried out deep cooperation with the United States on China-U.S. routes through the introduction of the 3.55% equity investment of RMB2.75 billion of Delta Air Lines. In April 2016, Ctrip's private placement of RMB3 billion in CEA has left a room for imagination for follow-up cooperation between the two parties. On June 19, 2017, CEA formally signed a capital increase agreement with four investors, Legend Holdings, GLP, Deppon and Greenland. It reduced its state-owned equity to below 50% for the first time and completed the long-term equity incentive mechanism for its core employees. Although it still takes time to test whether the reform can be successful, we think it is a good exploration and promotion for listed companies in terms of corporate governance and its efficiency.

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast.

War, terrorist attacks, SARS and other emergencies;

Highspeed railway diversion

Financials

Click Here for PDF format...