Investment Summary

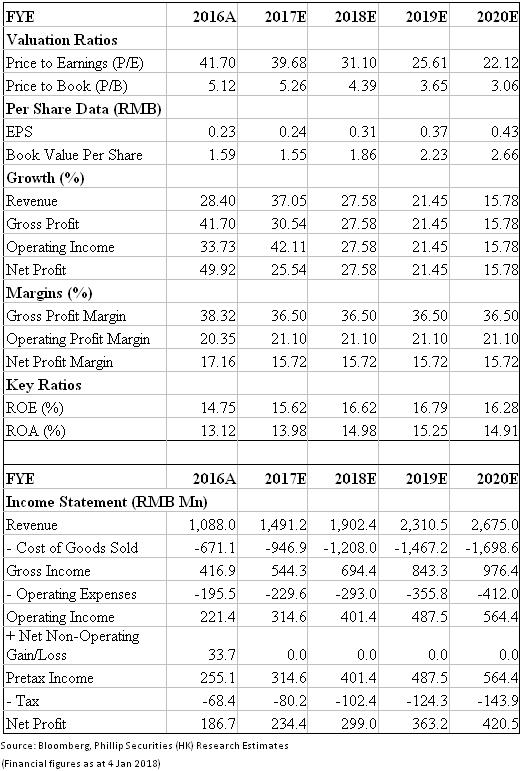

Yihai is a leading and fast-growing compound condiment manufacturer in PRC. The company achieved high growth since 2013, given revenue/net profit recorded FY13-16 CAGR of 51%/104% respectively. We believe that the company will benefit from the trend of consumption upgrade and increasing resident consumption demand. We also highlight that the company enjoys significant brand advantage and has strong channel advantage with a national wide distribution network. We use DCF model to get stock price and review it with relative valuation, which shows our target price located in a rational range. We give `Accumulate` recommendation with target price of HKD9.10 implying 11.8% upside, and suggest buying during price dips. (Closing price at 4 Jan 2018)

Business Overview

Company Background. The company started from producing hot pot flavoring for Haidilao restaurants and was listed on HK exchange in 2016. Haidilao (HDL) was established in 1994 and now has become a national hot pot chain with 192 restaurants in China as up to 17H1. According to Frost & Sullivan, HDL is the largest Chinese hot pot restaurant chain and the No.1 Chinese cuisine restaurant company in China, as measured by 2015 sales. The listed company is the sole supplier of hot pot soup flavoring products to HDL. The company hss the exclusive right to use the Haidilao brand to sell condiment products on a royalty-free basis for a perpetual term commencing from 2007.

Product Portfolio. The company manufactures mid- to high-end compound condiment products, including hot pot soup flavoring products, hot pot dipping sauce products and Chinese-style compound condiment products. The main product is hot pot soup flavoring making up 85% in 17H1 revenue with gross profit margin around 33%. According to Frost & Sullivan, the company is the largest mid- to high-end hot pot soup flavoring condiment manufacturer as measured by 2015 sales, which accounts for over 30% market share.

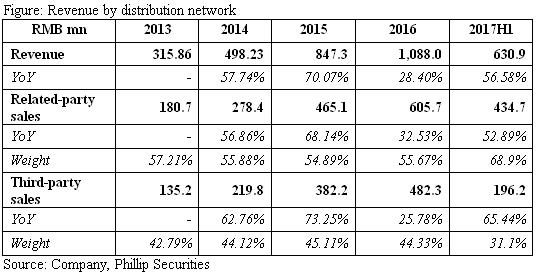

Distribution Channels. The company produces and sells compound condiment products to related-party customers (mainly HDL) and third-party customers. We see both channels develop quickly, with income from HDL recording FY13-16 CAGR 49.7% and 52.8% for third-party sales. Currently, related-party sales contributes most to company revenue (55% in 2016 topline, 69% in 2017H1 topline). The products for HDL are exclusively customized for HDL restaurants and mainly involve hot pot flavoring. Third-party clients consist of distributors, online shoppers and catering service providers. Distributors as the most significant channel contribute over 90% to third-party sales. Now the company has 782 distributors, covering 360 Chinese cities and 14 foreign countries and areas.

Growth Momentum

Rising Industry. (1) Hot port condiment. According to Frost & Sullivan, in 2015 the market size of hot port condiment (including both hot pot soup flavoring products and dipping sauce products) totaled to RMB15.4bn with FY10-15 CAGR 15.9%. And it is estimated to expand to RMB31.0bn in 2020 implying FY15-20 CAGR of 15%. (2) Chinese-style compound condiment. Sales of Chinese-style compound condiment products is also predicted to enjoy high growth in future with FY15-20 CAGR of 16.9%, from RMB12.3bn in 2015 to RMB26.8bn in 2020E. (3) Consumption upgrade trend brings opportunities to mid- to high-end market players. With the rising per capita income and the upgrading of consumption structure, the family and individual consumption of mid- to high-end products will further increase. And consumers tend to place more importance on food safety and product quality rather than price. It is estimated that sales of mid- to high-end hot pot soup flavoring products accounted for 23% market share (mass market 77%). This market share is predicted to climb to 29.6% in 2020E implying CAGR 22%, higher than expected growth of the whole hot pot soup flavoring market.

Brand Advantage. We believe that barriers to enter condiment industry are not high, which often leads to product homogeneity. We think the core competitiveness should not be product differentiation, but rather the brand. Outstanding brand often represents trustable food safety, superior quality and pleasing customer experience. HDL hot pot chains, with the first market share in mid- to high-end market, enjoy wide popularity and good brand image. The brand is often associated with good service and quality products. Selling under Haidilao brand, Yihai thus enjoys greater brand advantage than peers.

Quick Expansion of HDL. Frost & Sullivan projects that the hot pot catering market will grow at 10.2% CAGR during 2015 to 2020E. The increasing trend in hot pot catering service market is likely to drive the growth of hot pot condiment market. In past years, we see HDL chains expanded quickly, although all of its restaurants are self-operated rather than franchised. As up to end of 2017 June, HDL operates 192 hot pot restaurants in China, 23 of which are newly opened during first half. In future, we expect HDL to remain relatively rapid expansion and continue to raise same store sales growth, through improving table turnover and consumption per capita.

Strengthening Third-party Channels. (1) Distributors: In 16H1 the company replaced big provincial level wholesalers with more city-based distributors. We expect that Yihai continues to widen sales terminal network and enhance sales efficiency. With new capacity starting to contribute revenue and intensifying promotion, we expect this channel to maintain stable growth. (2) E-commerce. The company makes efforts to develop online channel, through enhancing marketing and promotion activities and broadening online new product portfolios. As of June 2017, Yihai builds five flagship stores on popular e-commerce platforms like Tmall and Suning. E-commerce channel sales grew at 215.7% YoY in 17H1. Considering its low base, we project E-commerce sales to continue high growth in future. (3) Third-party catering companies. The number of such customers reached 69 as at 30 June 2017 and sales revenue amounted to RMB 11.7mn. Although currently only a small portion of hot pot restaurants are using packaged hot pot soup flavoring products, while the majority of them choose to make hot pot condiments themselves. However, with business expansion, more catering service providers start to adopt packaged compound condiments in order to realize standardization and accompanying quality consistency. We expect the company to seize chance of this segment market to provide more diversified and customized products to clients.

Valuation

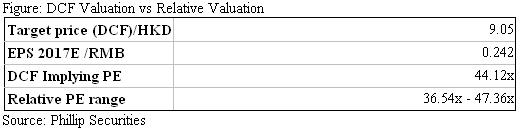

We adopt DCF method to calculate stock price and review our result referring to peers` PE valuation. (1) We predict the sales and EPS by estimating the growth of different channels and assume relatively stable profit margins. (2) Given Beta 1.33, WACC 7.59%, our DCF model gives stock price of HKD9.05, representing PE 44.12x. (3) We build a sample by selecting 11 listed firms focused on condiment products in PRC. We get market-cap weighted average PE 40.06x and median PE 36.54x. To further excluding market-cap influence, we pick 3 firms with most similar market cap, which implies even higher average PE 45.77x and median PE 47.36x. Relative valuation indicates a rational PE range of 36.54x to 47.36. (4) Our target PE from DCF is located in this range. Besides, we highlight that Yihai's revenue and net profit grow more rapidly than peers. Therefore, we think that DCF derived price 9.05 is generally reasonable. (Exchange rate refers to HKDCNY 1y forward price on Jan 3rd 2018.)

Investment Recommendation

The condiment industry is expected to benefit from rising consumer demand and consumption upgrade. We highlight that leading enterprises with brand and channel advantages are more likely to achieve significant development. Yihai features outstanding brand advantage and expanding channels. Although the stock price increased dramatically since Dec 2017, given current lower than average PE and strong growth expectation, we still consider the stock attractive. We give `Accumulate` recommendation, target price HKD9.10 with 11.8% upside, and suggest buying during price dips.

Risk

Sales may be adversely affected if Haidilao brand is harmed; Price hike of raw material and rising expenses; Revenue growth fail expectations.

Financials

Click Here for PDF format...