Investment Summary

Events: Pudilan was selected into Jilin and Henan PDRLs; NHFPC recommends CCQG for treatment of children flu; Another product YYG attained production approval. Investment suggestion: We highlight the company's comprehensive product mix and pipeline with visible sales growth and improved OTC channel. We predict the topline to grow at 23%/22% in 17E/18E and increase our target price to RMB50.8 (assuming PE 33.5x) with `BUY` recommendation, 22% upside. (Closing price at 12 Jan 2018)

Business Overview

Winter flu may facilitate CCQG sales hike. Since this winter the influenza has been prevalent in many Chinese cities, and the epidemic of children flu is especially serious. On Jan 8th, NHFPC issued a influenza treatment program (2018), in which the Child Chiqiao Qingre Granules (CCQG, Jumpcan's exclusive product) was recommended for the treatment of children influenza. We expect that winter flu may promote CCQC sales.

Pudilan was selected into Jilin and Henan PDRLs. The company recently announced that its exclusive product Pudilan Anti-inflammatory Oral Liquid (PAOL) entered into Jilin and Henan PDRLs. We highlight that inclusion into Jilin and Henan PDRLs will enlarge PAOL sales more obviously than inclusion into Qinghai PDRL before, given these two provinces have much bigger population base. Compared with Pudilan tablets and capsules, Pudilan oral liquid is more convenient for patient to take. And PAOL as an anti- inflammatory medicine will continue to benefit from national policy restrictions to its main competitors (including antibiotics and traditional Chinese medicine injection). We expect PAOL sales to grow at ~20% YoY in 2017E.

YYG gained production approval. Digestive segment includes one core product Rabeprazole Sodium Enteric capsules (RSE), which recorded sales of RMB1.1bn (+12% YoY) in 2016 with relatively large market cap. In 2017 Nov one subsidiary Dongke attained the production approval for Yangyingqingwei Granules (YYG). YYG is an exclusive product for treatment of chronic atrophic gastritis with no competitors producing and selling the same product now. Dongke acquired the rights of YYG in 2016 June at a price of RMB17mn. We expect YYG to further enrich the digestive product line, while it still takes time to cultivate market and generate income.

Comprehensive product mix and pipeline with visible sales growth. We highlight that the company has comprehensive drug portfolio and sustainable pipeline for different growth stages. Pudilan sales by hospital channel is expected to maintain stable growth while OTC sales is likely to surge; CCQG won bid in many regions last year which will facilitate sales volume hike; Iron Proteinsuccinylate Oral Solution (IPOS) is likely to reach over RMB 100mn sales with attaining tender in eight new provinces and cities. Also we estimate sales of Fuyanshu Capsules, Ganhai Weikang capsules and Huanglong Kechuan capsules will also climb in 2017E. Meanwhile, the company launches Pudilan toothpaste series for both adults and children to enrich the health care product line. The sustainable product lines are expected to underpin future development.

Improved OTC channel. Jumpcan expanded its OTC channel in 2017H2 by building professional promotion team and intensify pharmacy chain network. It has an OTC sales team with over 1000 people which mainly promotes core products including PAOL, RSE, CCQG, etc. We expect OTC sales to experience rapid growth in 2017E.

Investment Thesis & Valuation

We increase target price to RMB50.8. We select 19 A-share firms focusing on Chinese patent medicine with market cap more than RMB10bn to get the PE average (37.56x) and median (30.44x). We see Jumpcan now is traded at around PE 28.9x, which is much lower than industry average. Back to 2016 Jumpcan recorded net profit YoY growth 34%, which is much higher than industry average growth level (10.3%). During past three quarters in 2017, Jumpcan achieved topline/bottom line growth of 21.75%/38%, therefore we see highly visible sales growth in 2017E. We predict the revenue growth to be 23%/22% in 17E/18E. Assuming PE 33.5x (middle between industry average and median), we give target price RMB50.8 and `BUY` recommendation.

Risk

Slow than expected expansion of distribution network;

Substantial shareholders selling shares;

Policy risks;

R&D failure.

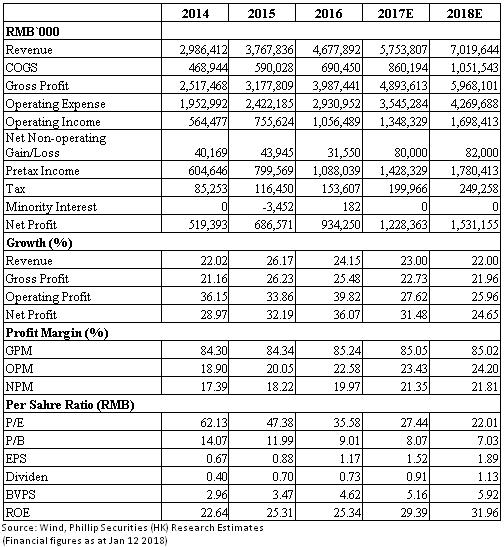

Financials

Click Here for PDF format...