Investment Summary

We highlight that 1) Descente is expected to benefit from developing winter sports market; 2) New logistics center is going into operation soon; 3) Main brands are on right track; 4) E-commerce grows quickly. Given PE 26x (par to industry average), we increase our target price to HKD40.37, `Neutral` recommendation. (Closing price at 22 Jan 2018)

Business Overview

New logistics center going into operation soon. We know from our checks that company's new logistics center will go into operation in May 2018. This new center will help to significantly shorten delivery time from factories to distributors and retail terminals (from one month to as quick as 2 days). It will improve the replenishment efficiency which facilitates the company to better respond to market conditions and changes in consumer preferences.

Main brands are on right track. Anta brand is expected to achieve mid-teens growth in 2017E, given normal inventory turnover and continued same store sales growth in 17Q4. Fila brand enters more shopping malls and department stores in tier-one cities and we expect Fila to deliver over 30% YoY growth in 2017E. Because of early winter and cold weather, warm clothing sells well in northern market. We expect generally good performance in 17Q4.

Descente is expected to benefit from intensifying winter sports market. Descente is introduced in 2016 offering winter sportswear and now majority of Descente products are imported. The company makes efforts to localize the products in order to better cater to Chinese customers. Meanwhile the company is planning to develop summer products that will enrich the brand product mix and mitigate seasonal effect. The brand is expected to open 50 new stores in 2018E. We expect 2022 Beijing Winter Olympics will help to make winter sports more popular in northern area. According to Suggestions to Speeding up the Development of Winter Sports (2016-2011) issued by Beijing municipal government, the population participating in winter sports will amount to 8 million in 2022E. The government is going to establish more skiing fields and promote winter sports to residents and schools. We highlight that increasing popularity of winter sports will boost sales of relating apparels and footwear. Anta is dedicated to enhance promotion campaign for winter sports and make Descente a popular winter sports brand.

Kolon fills blank of outdoor market. The company set a JV with Korean Kolon in Sep 2017 to commercialize Kolon IP in China market. Kolon owns more than 200 stores in PRC targeting mid/high-end clients. The brand provides not only professional outdoor products but also fashionable outdoor leisure products with popular star Song Zhongji as its spokesperson. Kolon enriches the company product lines. We expect that Kolon will leverage on Anta's strong distribution channel and efficient operation to win more share of outdoor products market.

Comprehensive kidswear portfolio. We see improving children product lines which cater to children aged 0-14 and cover low-, mid-, and high-end market at the same time. Anta Kids targets low/mid-end market with sports style products. While Fila Kids offers leisure clothing and targets to mid/high-end market. We expect Fila Kids to grow rapidly together with the expansion of Fila stores. Besides, the company acquired a Hong Kong kidswear brand KingKow in 2017, which further supplements children product lines. KingKow operates over 80 stores in HK, TW, and PRC. We expect the positive earnings contribution to come later given the company is adjusting the stores network right now.

E-commerce grows quickly. As far as we know, 70% of online products are exclusive products, 20% are synchronized with current offline products, while 10% are aged stocks. E-commerce channel consists of flagship stores in main stream platforms and Anta official website. We know from internet source that Anta posted the third highest sales volume on 2017 Singles` day in Tmall, ranked No.1 among native brands. We also notice Anta has launched ANTAUNI on its official website, which accepts customized orders of basketball shoes and running shoes priced at RMB200-600 per pair. Compared with Nike and Adidas customized shoes which usually cost over RMB1000 one pair, Anta products may be more attractive for customers who value performance-price. We expect the E-commerce sales to record notable growth in future.

Rising expenses. Anta Sports values event marketing. The company successfully renews its sponsor contract with the national team in Sep 2017 with a higher cost. There are three important sports events in 2018: Pingchang Winter Olympics in Feb, Russia World Cup during Jun to Jul, and Asia Games during Aug to Sep. We expect the advertising cost will increase for these sports events. Meanwhile, as more stores will be opened in shopping malls and department stores, we expect higher rental cost. But considering that more brands` inclusion into financial results will enlarge the topline and main brands are likely to report steady growth, we still expect the OPM to remain stable.

Investment Thesis & Valuation

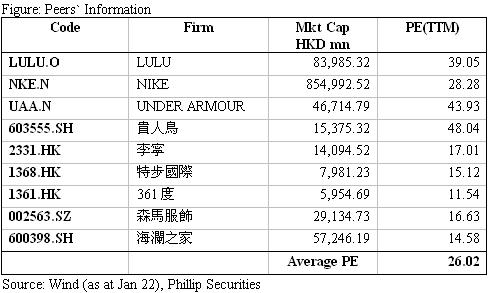

We select peers in apparel and footwear industry then get industry average PE 26x. We fine-tuned our numbers to factor into the rising advertising cost. Assuming PE 26x, we get our target price of HKD40.37. With 4.7% upside, we give `Neutral` recommendation.

Risks

Slow than expected sales growth;

Rising distribution cost due to intensive marketing;

Fierce competition in sportswear industry;

New brands performance fail expectation.

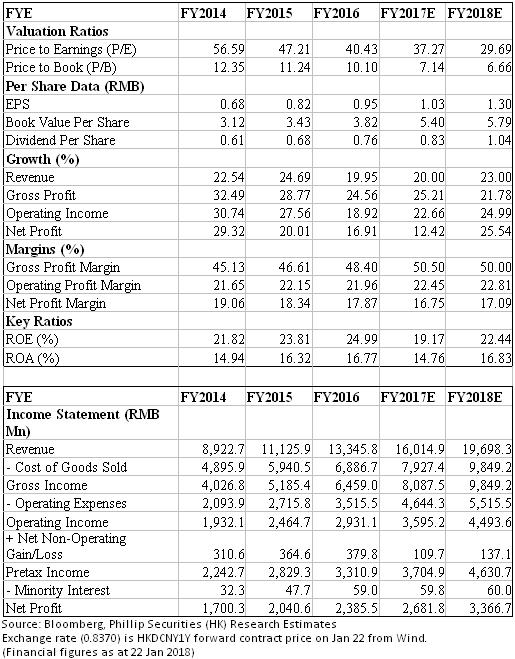

Financials

Click Here for PDF format...