Summary of Investment

- Marching into the southwest market to expand its nationwide layout;

- Gaining a substantial increase in productivity in 2018;

- Cooperating with Conch Venture, constituting a strong partnership in respect of hazardous waste treatment;

Investment Advice

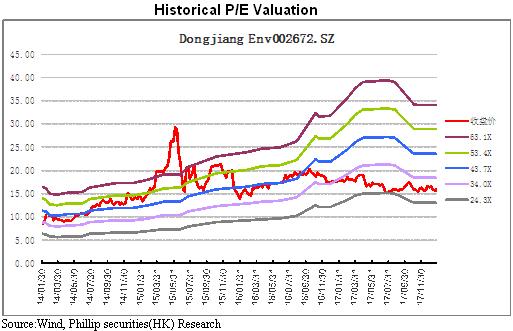

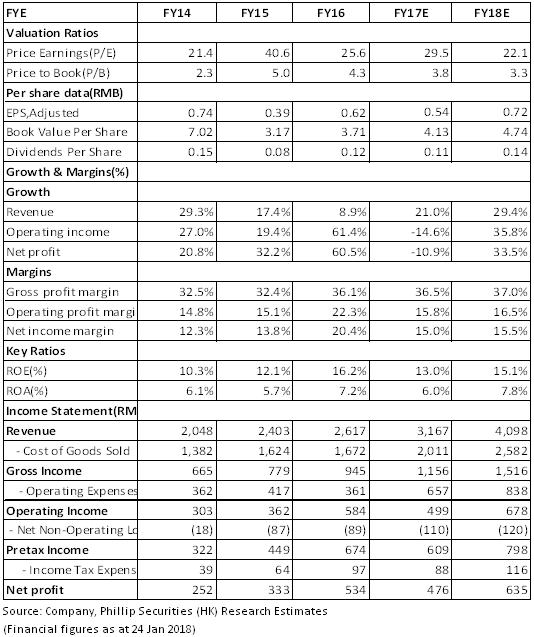

It is forecast that net profit of the Company in 2017 and 2018 will reach RMB 476 million and RMB 635million, respectively; earnings per share (EPS) will be RMB 0.54 and RMB 0.72, respectively; the P/E ratio will be 29.5 and 22.1 , respectively; the target price will be RMB20.2, with a Buy rating. (Closing price as at 24 Jan 2018)

The Nationwide Leading Hazardous Waste Treatment Enterprise is Accelerating Its Expansion

DongJiang Environment is mainly committed to three core fields, i.e., resource recovery, waste harmless treatment and environmental service, and owns 28 hazardous waste treatment and disposal bases around the country. The Company occupies the core industrial hazardous waste market share in China, and forms an industrial layout covering Pearl River Delta mainly including Guangdong, Yangtze River Delta mainly including Jiangsu Province and Zhejiang Province, North China mainly including Hebei Province, Shandong Province and Hubei Province, as well as Jiangxi Province, and Fujian Province, etc. As of the end of 2017, the Company's implemented hazardous waste productivity was about 1.8 million tons/year, of which about 0.9 million tons was attributable to harmless productivity, accounting for 50%. It is expected that, in five years, the Company's hazardous waste treatment productivity will reach 5 million tons/year, of which 1 million tons/year will be attributable to solid waste co-treatment in cement kilns co-disposing productivity, and the average compound annual growth rate will reach 22.7%.

Marching into the Southwest Market to Expand Its Nationwide Layout. The Company signed an investment agreement with Fucheng District, Mianyang City, Sichuan Province, planning to construct a large comprehensive industrial hazardous waste treatment base, which will have an annual solid waste treatment productivity of 0.35 million tons, including 0.25 million tons/year of harmless waste and 0.1 million tons/year of resource recovery, with a total investment of RMB1.5 billion. Currently, the demand-supply gap of hazardous waste treatment in Mianyang City is large, and after the project is completed, the contradiction between the high local industrial waste treatment demand and the deficient treatment capacity will be effectively solved. At the same time, such influence will be radiated to cities around Mianyang City like Chengdu City, Deyang City, etc., advantageous for the Company's regional from-point-to-area market layout, enhancing its market share and comprehensive competitiveness in the southwest region and laying a solid foundation for its future occupying the market.

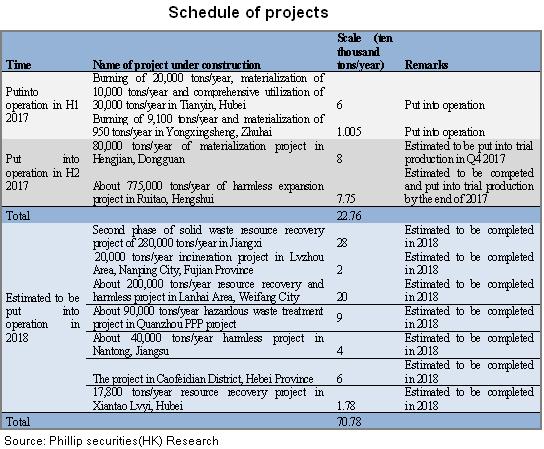

Gaining a Substantial Increase in Productivity in 2018

In 2018, the Company will implement multiple hazardous waste projects in a concentrated way, including 0.28 million tons of resource recovery of Phase II of the project at Dongjiang River, Jiangxi Province, 0.2 million of harmless + resource recovery in Lanhai Area, Weifang City, about 40 thousand tons of harmless waste of the Nantong Project, about 60 thousand tons of harmless + resource recovery of the project at Caofeidian District, Hebei Province, about 20 thousand tons of harmless waste in Lvzhou Area, Nanping City, about 90 thousand tons of harmless + resource recovery of the Quanzhou Project, 17.8 thousand tons of resource recovery in Xiantao City, Hubei Province and so on; the predicted newly increased productivity will be about 0.7 million tons, resulting in an actual productivity of up to 2.5 million tons/year. We hold that the release of newly increased productivity and the increase of productivity utilization rate will facilitate the realization of a high result growth in the future two years.

Cooperating with Conch Venture, Constituting a Strong Partnership in Respect of Hazardous Waste Treatment

DongJiang Environment and Conch Venture reached a cooperative intention with regard to the solid waste co-treatment in cement kilns a few days ago. Taking Guangdong Province as the pilot site and executing equity cooperation, both parties would mutually advance the distribution of cement kiln solid waste co-treatment points in Guangdong Province and the development of cement kiln solid waste co-treatment projects across the country.

The cement kiln waste co-treatment technology has been developed maturely at abroad, and up to now has gradually entered its rapid development stage. Conch Venture is devoted to three fields, namely hazardous waste co-treatment in cement kilns, municipal waste co-treatment in cement kilns and waste incineration power generation. Up to now, its cement kilns completed and put into operation have a solid waste co-treatment capacity of 375 thousand tons/year, and those under construction have a solid waste co-treatment capacity of 1.67 million tons/year. Its hazardous waste co-treatment technology and business mode of the cement kilns take leading positions in the industry. We hold that through the productivity cooperation with Conch Venture, the Company can complement each other's advantages in treatment technologies and market layout, well supplement and expand the Company's existing hazardous waste treatment mode and regional layout, energetically improve the Company's hazardous waste treatment scale and efficiency, consolidate the industrial position and lead the industrial development.

According to the Three-year Action Plan on Control over Solid Waste Pollution (from 2018 to 2020) (Exposure Draft) issued by Guangdong Province on November 9, it was put forward that a batch of in-cement-kiln industrial solid waste co-treatment projects will be established at an accelerated speed with many efforts, so that the amount of industrial solid waste co-disposed in cement kilns would reach more than 5 million tons/year in 2020. Due to issuance of the policy, the degree of prosperity of in-cement-kiln co-treatment market has increased, bringing policy advantage to the cooperation between the two parties, possibly driving the implementation of the cooperative project between the two parties to achieve the Company's nationwide from-point-to-area expansion.

Risk Warnings

Intensified market competition;

Project implementation below expectation;

Project expansion below expectation;

Financials

Click Here for PDF format...