Investment Summary

Financial Data: Over 20% Decline in Profit of the First Three Quarters

New Energy Automobile Business Sails Again after the Twists and Turns

Cloud Rail Services and Mobile Phone Components Business Will be Another Two Important Growth Points for Future Earnings

Investment Thesis

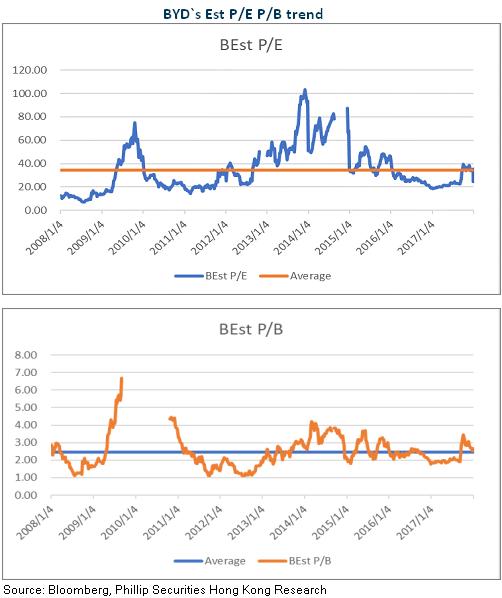

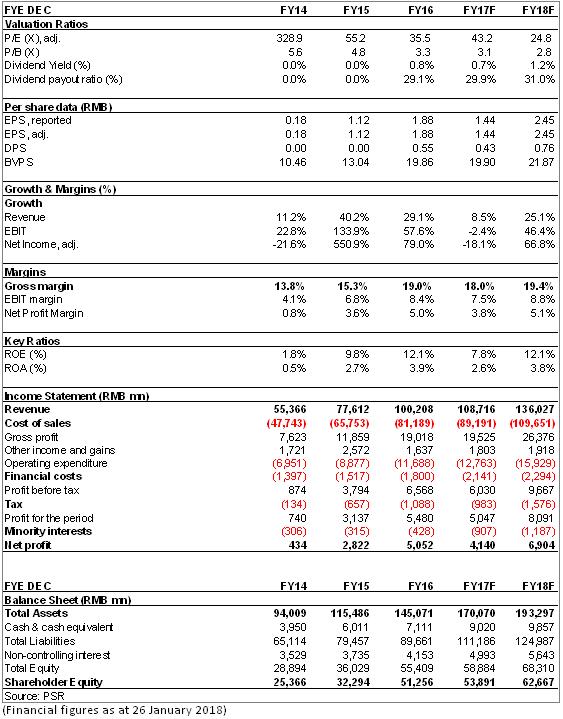

We adjusted the expected EPS of 2017/2018 to RMB1.44 / RMB 2.45 and revise the target price to HKD84.43, which corresponded to 49/28x P/E and 3.5/3.1x P/B ratio for 2017/2018. We give the rating of “Accumulate”. (Closing price as at 26 Jan 2018)

Financial Data: Over 20% Decline in Profit of the First Three Quarters

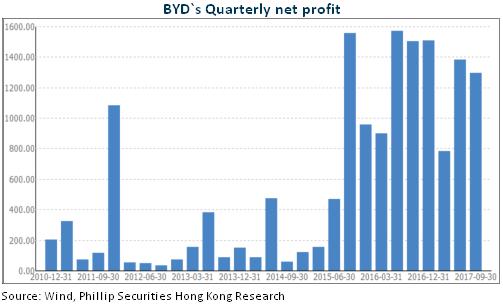

BYD recorded revenue of RMB73.93 billion in the first three quarters of 2017, which was basically flat yoy. The profit attributable to the owner of the parent company was RMB2.79 billion, down 23.8% yoy. EPS was RMB0.96. And the results were basically in line with the Company's previous result forecast of RMB2.74 - 2.93 billion. The Company also expects to record net profit attributable to shareholders of RMB4.04 - 4.29 billion in 2017, down 20.03% - 15.09% yoy. As a leader in the new energy industry, the decline in the first three quarters of BYD mainly comes from the change of industry prosperity caused by industrial policy adjustment.

New Energy Automobile Business Sails Again after the Twists and Turns

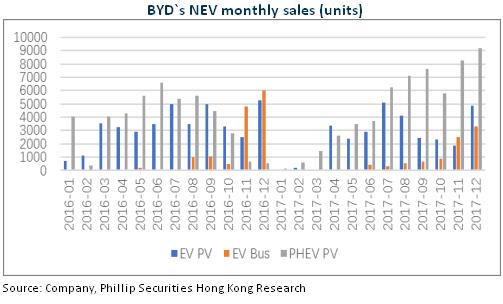

Affected by the slashed new energy subsidies and new subsidies catalog management at the beginning of the year, China's new energy automobile industry experienced twists and turns in the first half of this year. In the first quarter, sales of new energy vehicles fell 4.7% to 56,000 units yoy, a sharp drop in growth. As the new subsidized product catalog has been distributed, and local government subsidy policies have been issued, the new energy automobile industry gradually recovered the momentum of rapid growth in the past in the second quarter. Sales volume doubled in October to 91,000 vehicles yoy. Cumulative sales rose 45% to 490,000 units in the first ten months.

Led by the new plug-in HEV Song DM and EV Song EV300, and the upgraded version of the Qin 100, Tang 100, E5 300 and other models, the Company sales volume of new energy vehicles increased month by month. In the first ten months, 83,000 units of new energy vehicles were sold, reaching sales target two months ahead of the schedule, with a global market share of 13%. In addition, an entry-level E5DM new model will be launched this year, mainly in the unsubsidized cities, to help the Company expand its market share. It is expected to sell 150,000 new energy vehicles throughout the year, including 130,000 new energy passenger vehicles, 15,000 EV buses and 5,000 special vehicles.

In 2018, the Company will launch new models, including the Qin II and the Tang II, and a high-end SUV model Ming and a sedan model Han. The Company has set a target of new energy vehicle sales of 200,000 units next year, and the target global coverage of cities will be expanded from 200 to 400. And 30,000 charging facilities will be built nationwide. We believe that the contribution of the new energy vehicle business in the overall business of the Company will be further enhanced, and the revenue share is expected to exceed 40%.

Cloud Rail Services and Mobile Phone Components Business Will be Another Two Important Growth Points for Future Earnings

BYD's first cloud rail was officially opened to traffic in September, in Yinchuan, Ningxia and won many praise. The construction cost of the cloud rail is only 1/4 - 1/5 of the subway, the construction time is 1/3 of the subway, and the operation cost is 1/2 of the subway. The cloud rail has huge potential market space in the large number of small and medium-sized cities. At present, the Company has signed a cooperation agreement with a number of cities or enterprises, to promote "cloud rail" project. It is expected that results will be slightly increased in the fourth quarter of this year and the promotion of profit contribution will be accelerated next year.

Benefiting from that the metal shell and the metal frame have gradually become the mainstream specification of the mid- and high-end smart phones, profits attributable to the parent company in the first three quarters of 2017 of mobile phone parts business of the Company rose 125% to RMB1.99 billion. In the future, with the capacity release of 3D glass and smart phone metallization trend, the business is still expected to maintain rapid sustainable growth.

Risk

Sales of new energy vehicles is not as good as expected

Cloud Rail business risk

Financials

Click Here for PDF format...