Sectors:

Air, Automobiles (ZhangJing)

Environmental protection (Wang Yannan)

Healthcare, Consumer (Eurus Zhou)

Automobile & Air (ZhangJing)

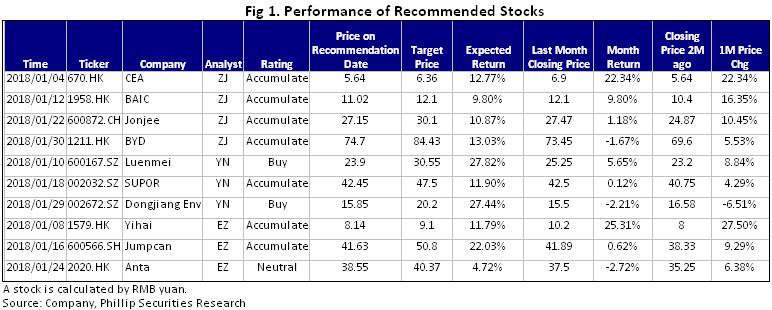

This month I released 4 equity reports including China Eastern Airline CEA (670.HK), BAIC (1958.HK), Jonjee (600872.CH) and BYD (1211.HK).They all got success by their unique Competitive edge. We prefer CEA and BAIC.

CEA ranks the first among the top three airlines in introducing ASK. On June 19, 2017, CEA formally signed a capital increase agreement with four investors, Legend Holdings, GLP, Deppon and Greenland. It reduced its state-owned equity to below 50% for the first time and completed the long-term equity incentive mechanism for its core employees. Although it still takes time to test whether the reform can be successful, we think it is a good exploration and promotion for listed companies in terms of corporate governance and its efficiency. Given that possible improvement on efficiency after the mix reform, and the expected better ticket price in the future, we are optimistic about the Company's future result flexibility.

According to media reports, the parent company BAIC Group has recently announced that it will divest Weiwang, its self-owned sub-brand to BAIC Changhe. The divestment of Weiwang will help BAIC reduce revenue losses of its self-owned brands of at least RMB2 billion in 2018.Earlier, the Company had announced that it planned to issue new A-shares of no more than RMB485 million, equivalent to 6.0% of the enlarged total share capital. The net raised funds will be used to upgrade its production base, expand production capacity, replenish working capital and repay bank debts. As A shares enjoy a higher valuation premium than H shares, we think this move is expected to significantly increase the Company's intrinsic value and enhance its capital strength.

Environmental protection (Wang Yannan )

In this month I released 3equity reports, including Luenmei (600167.SZ), SUPOR( 002032.SZ ), Dongjiang Env (002672.SZ). In the first three quarters of 2017, Luenmei Holding recorded a revenue of RMB1,338 million with an increase of 18.88% year on year, net profit attributable to parent company RMB467 million with an increase of 56.83% year on year, equivalent to EPS of RMB0.61, with an increase of 38.7% year on year. Recently stock price of the Company has been volatile, and the controlling shareholders increased their holdings to strengthen investment value of the Company and stable investment confidence. We expect the net profit of the Company in year 2017-2018 attributable to the parent company will be RMB893 million and RMB1142million, respectively, equivalent to EPSof RMB1.01/share, RMB1.30/share, respectively, and PE of 23.6, 18.4 times, respectively. For the first coverage, target price 30.55 and rating Buy are given.

Healthcare & Consuming (Eurus Zhou)

This month I released 3 equity reports, including Yihai International (1579.HK), Jumcan Pharma (600566.CH), and Anta Sports (2020.HK). We tend to highly recommend Jumpcan (600566.CH) and Anta Sports (2020.HK).

For Jumpcan, we highlight that Pudilan was selected into Jilin and Henan PDRLs in 2018. The company recently announced that its exclusive product PAOL entered into Jilin and Henan PDRLs. We highlight that inclusion into Jilin and Henan PDRLs will enlarge PAOL sales more obviously than inclusion into Qinghai PDRL before, given these two provinces have much bigger population base. One subsidiary Dongke attained the production approval for YYG, an exclusive product for treatment of chronic atrophic gastritis. We expect YYG to further enrich the digestive product line, while it still takes time to cultivate market and generate income. Jumpcan expanded its OTC channel in 2017H2 by building professional promotion team and intensify pharmacy chain network.

As for Anta Sports, the company's new logistics center will go into operation in May 2018. This new center will help to significantly shorten delivery time from factories to distributors and retail terminals. It will improve the replenishment efficiency which facilitates the company to better respond to market conditions and changes in consumer preferences. Anta brand is expected to achieve mid-teens growth in 2017E, given normal inventory turnover and continued same store sales growth in 17Q4. Fila brand enters more shopping malls and department stores in tier-one cities and we expect Fila to deliver over 30% YoY growth in 2017E. The company successfully renews its sponsor contract with the national team in Sep 2017 with a higher cost. There are three important sports events in 2018. We expect the advertising cost will increase for these sports events and higher rental cost due to more stores opened in shopping malls. But considering that more brands` inclusion into financial results will enlarge the topline and main brands are likely to report steady growth, we still expect the OPM to remain stable.

Click Here for PDF format...